Sulphur 423 Mar-Apr 2026

23 March 2026

Market Outlook

Market Outlook

SULPHUR

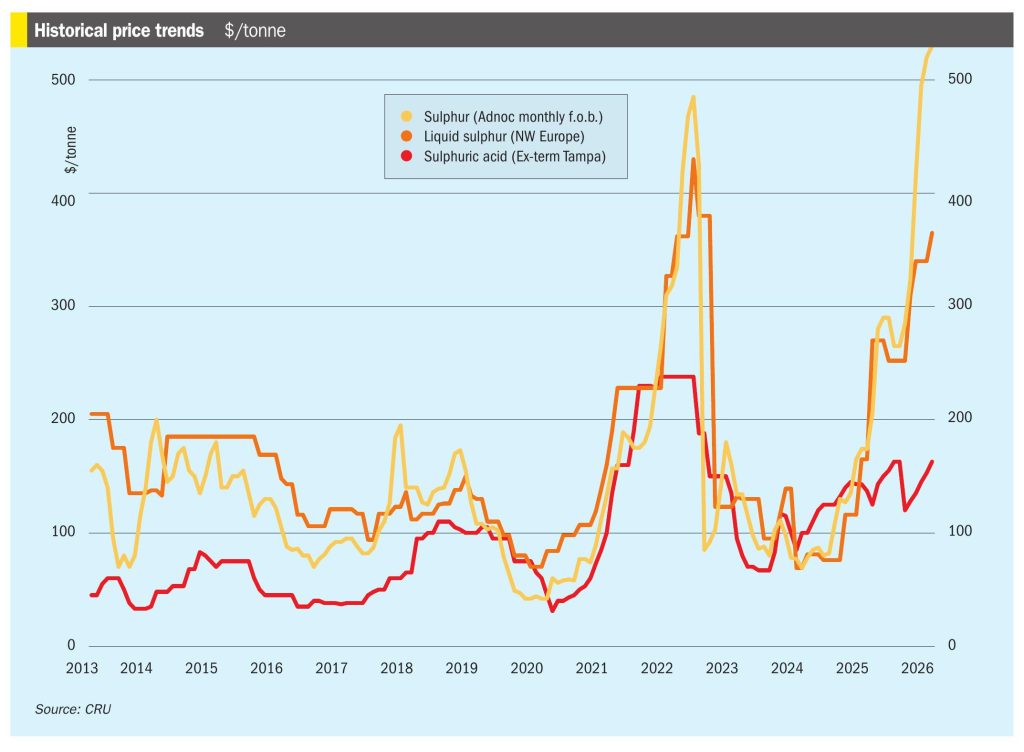

• Market sentiment has shifted decisively from bearish to bullish as the conflict in the Middle East has triggers a significant price rally.

• The sulphur market’s direction is now dependant on the duration of the conflict in the Middle East. The current holding pattern is unsustainable, and the market is poised for a price increase as 48% of seaborne supply remains largely unavailable.

• A prolonged halt to operations would mean the loss of volumes that cannot be recovered from other origins, tightening the global balance and inevitably leading to demand destruction and upward pressure on the market. While production continues, the halt in shipping will also start to cause inventory build-up, with some producers facing imminent storage issues if exports remain blocked. The immediate lack of cargo availability is supporting prices.

• However, this support is fragile. If the flow of vessels through the Strait of Hormuz recovers in the short term, the release of this pent-up supply would likely cause prices to fall.

• Market sentiment is split between fears of demand destruction and concerns over supply security. One side argues that if phosphate producers cannot secure ammonia, sulphur demand will collapse. Conversely, other buyers are focused on the sulphur shortage itself, showing a willingness to pay a premium to secure product.

SULPHURIC ACID

• Looking ahead, the market remains clouded by significant uncertainty. In the near term, price direction will depend on the duration of the shipping disruption. With sulphur from the Middle East being significantly affected, there is growing market talk that China may potentially restrict its acid exports after April, opting to use the acid domestically as an alternative to buying expensive sulphur. While this currently remains just a rumour, such a policy shift would add significant upside risk to the seaborne market.

• Near-term prices will be influenced by the logistical reshuffling from the Maaden disruption, but the greater upside risk is the potential for China to extend its current export policy, which would fundamentally tighten the global market; the conflict in the Middle East has prompted speculation that China may extend its current sulphuric acid export policy beyond its expected April end date, in a bid to retain acid domestically as an alternative to expensive sulphur imports.

• For now, the market will remain thin and price discovery uneven. Importers on maintenance will keep demand muted, traders will hold back parcels unless pricing becomes compelling, and the impact of regional tensions will determine whether the next visible transactions reset the assessment higher or merely reflect isolated distressed volumes.