Sulphur 425 Jul-Aug 2026

14 July 2026

Price Trends

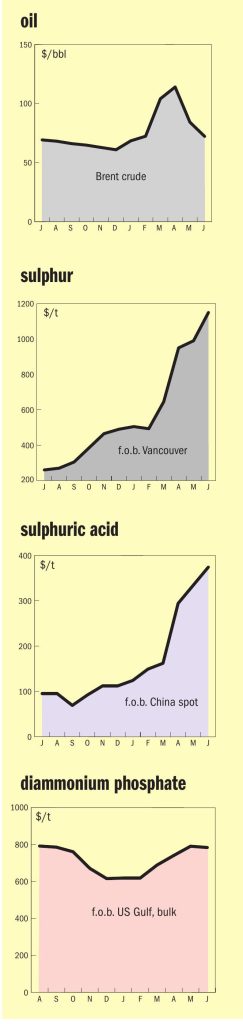

SULPHUR

The global sulphur market has entered a holding pattern, as a wave of bearish sentiment has so far failed to move stubbornly high spot prices. The departure of a significant volume of product from the Middle East has emboldened buyers and shifted market sentiment firmly towards bearish, but at time of writing this has so far failed to translate into lower prices. With sellers in no hurry to lower prices and spot availability still tight, the market has stalled as both sides wait for the other to blink first.

The source of this sentiment shift is the memorandum of understanding between the US and Iran, which has created a narrow window for passage through the Strait of Hormuz. The 60-day ceasefire, in spite of violations by both sides, has nevertheless held firm enough to allow 22 vessels carrying a combined 1.07 million tonnes of sulphur to depart the region. While these cargoes are now en route to key demand centres like Morocco, Indonesia, and India, the product is understood to be largely pre-sold or under contract. As a result, the shipments have not added fresh liquidity to the spot market, but the partial success of the deal has provided significant psychological relief to buyers, reinforcing the belief that the period of extreme tightness is ending. Even so, the pace of new loadings has stalled, with no new sulphur vessels understood to have loaded from the region in the last week of June. This leaves a backlog of 380,000 tonnes of sulphur stranded on eight vessels inside the Gulf.

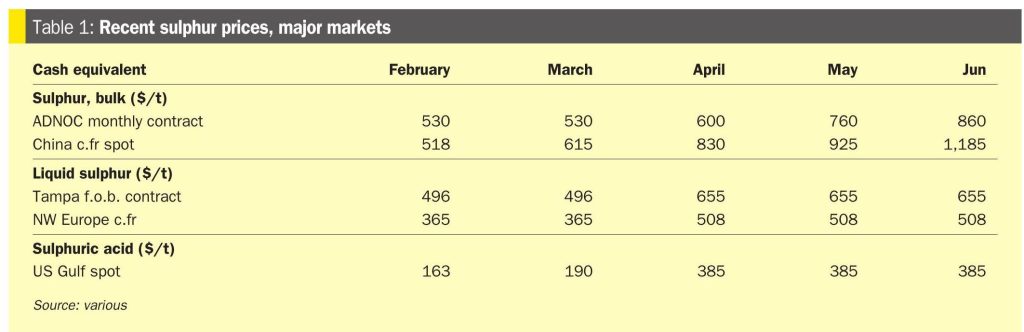

The change in buyer attitude is most apparent in major c.fr markets. In Brazil, a new tender from CMOC is expected to test the lower end of the $1,100-1,250/t c.fr range. In India, bids are holding at a firm ceiling of $1,000/t c.fr. This purchasing restraint is clearly reflected in import data, with Brazilian arrivals for May-June down 45% year-on-year, according to Wilson Sons data and Indian volumes for the same period halving. Elsewhere, buyers in China and Indonesia are limiting purchases to immediate needs, operating on the assumption that waiting will yield lower prices. Strong buyer resistance has emerged in Indonesia, a response to record-high prices squeezing margins. This has been compounded by a recent decrease in LME nickel prices, which fell to $16,610/t. As a result, buyers are reportedly bidding only at the low end of the current price range, or even below it, and are limiting purchases to a hand-to-mouth basis. While acknowledging buyer resistance, sellers report no immediate pressure to reduce price ideas. Nevertheless, with fresh supply on the horizon and demand being curtailed by affordability, the next concluded deals are widely expected to be below the $1,200/t level.

Producer positions, however, remain largely unchanged. In North America, prices remain steady at $1,100-1,200/t f.o.b., with suppliers reporting no pressure to lower offers, citing healthy forward sales and continued inquiries. This has opened up a wide gap between seller pricing ideas and the price levels buyers are now willing to entertain. However, this level’s stability is viewed as temporary amid widespread expectations that prices will soften slightly. The focus remains on the Q3 Tampa contract, though negotiations have reportedly not yet commenced.

Likewise in Europe, the focus remains entirely on the Q3 European contract price, but negotiations have reportedly stalled. The deadlock stems from the significant gap between the Q2 settlement of $430-515/t c.fr and the current strength of the global spot market. Buyers are resisting a substantial increase, citing not only concerns over affordability but also the potential for a softening market as more vessels begin to move more freely from the Middle East. With neither side willing to make the first move, the negotiations have reached a standstill.

This tension between tight underlying fundamentals and the shift to bearish buyer sentiment has brought the market to a pause. On one hand, underlying supply fundamentals remain tight – arguably more so than before the Hormuz crisis, given the ongoing Russian export ban and new disruptions to Kazakh rail transit. Russia’s sulphur rail-transit ban in late May has stranded material produced in Kazakhstan. This structural deficit is expected to provide a floor for prices. On the other hand, the release of Middle East cargoes has created a strong expectation of price relief among buyers. The result is a quiet, tentative market, with the outcome of Brazil’s upcoming CMOC tender poised to provide the first concrete indication of future price direction.

SULPHURIC ACID

Global sulphuric acid prices were largely unchanged at the end of June as the market settled into a wait-and-see mode, with entrenched buyer resistance halting the recent upward momentum. With affordability stretched to its limit, buyers are now looking to the feedstock sulphur market and geopolitical stability in the Middle East for any sign that a price correction might be on the horizon.

This buyer-led slowdown is most pronounced in Chile, where major consumers are not just absent from the spot market but are actively implementing operational efficiencies to reduce overall acid consumption. The purchasing resistance is evident in the Chilean market, where delivered prices declined to an average of $489/t in June from $498/t in May, despite persistent supply tightness due to China’s ban on acid exports from May to December. This resistance is compounded by uncertainty over a potential supply deal from China; with no official approval confirmed for the rumoured acid-for-concentrates swap, a key source of potential relief remains purely speculative.

The situation is similar in Brazil, where affordability concerns have brought spot purchasing to a near standstill, reinforcing the theme of strong buyer pushback across South America. In Indonesia, the market is now defined by hand-to-mouth purchasing, with bids reportedly emerging below the key $400/t c.fr mark, even as a forward cargo for August was fixed at a firm $445/t c.fr. This highlights the growing disconnect between prompt demand and forward seller expectations. In India, the import market is quiet, with buyers finding a temporary solution by increasing domestic coastal shipments to fill the gap left by the absence of Chinese material.

India’s sulphuric acid imports were volatile across May and June, with combined volumes down 14.4% from 2025. A 63% year-on-year drop in May, driven by the absence of Chinese material, was followed by a 68.5% rebound in June. This recovery was fuelled by a significant increase in domestic coastal shipments, which compensated for the lack of Chinese imports and a concurrent reduction in cargoes from Japan and South Korea.

Despite the lull in buying, supply-side fundamentals remain unequivocally tight, keeping sellers’ price ideas firm. The ongoing Chinese export ban, which began in May, continues to be the primary driver, with its impact now starkly visible in trade data and the sharp rally in China’s domestic prices. China’s sulphuric acid exports in the first five months of 2026 totalled 783,509 tonnes, dropping 57% from the same period last year, according to Global Trade Tracker (GTT) data. The export ban has coincided with a sharp rise in Chinese domestic sulphuric acid prices, which have continued to strengthen since the restrictions were put in place, according to data from Longzhong. In Jiangsu province, for example, prices have climbed from rmb 1,900/t ($260.49/t) at the end of April to rmb 2,450/t ($335.89/t) by late June, a jump of nearly 29%. Similarly, prices in Anhui province increased from rmb 2,050/t ($281.05/t) to rmb 2,350/t ($322.18/t) over the same period.

This tightness is reinforced by strong export markets. A new tender in Japan was concluded at the top end of the range at $380-390/t f.o.b., while a flurry of deals from India’s West Coast were also done at a firm $380/t f.o.b.

In Europe, while prices are stable for now, the sentiment is clearly pointed upwards, with sellers targeting $380/t f.o.b. to keep pace with other regions, supported by a series of upcoming maintenance turnarounds that will further constrain supply. Discussions are reportedly underway with sellers leveraging the tight global supply to push for significant increases over the record-high Q2 contract levels.

Market rumours suggest that a Chinese smelter is negotiating a deal to supply acid to a Chile-based miner in exchange for copper concentrate. The deal has reportedly been approved by the Chinese government, but details remain unconfirmed. Volumes were rumoured at 99,000 tonnes. Still, despite being a prominent topic of conversation in the market, details on the arrangement remain elusive and unconfirmed.

The market is seeing a clear divergence in market sentiment, which is stalling activity. While tight supply keeps seller offers firm, buyer sentiment has turned more bearish, with most consumers concluding that the risk of purchasing at a potential market peak when a downside pricing trend may be around the corner outweighs the immediate need to secure volume.

END OF MONTH SPOT PRICES