Nitrogen+Syngas 402 Jul-Aug 2026

13 July 2026

Market Outlook

Market Outlook

AMMONIA

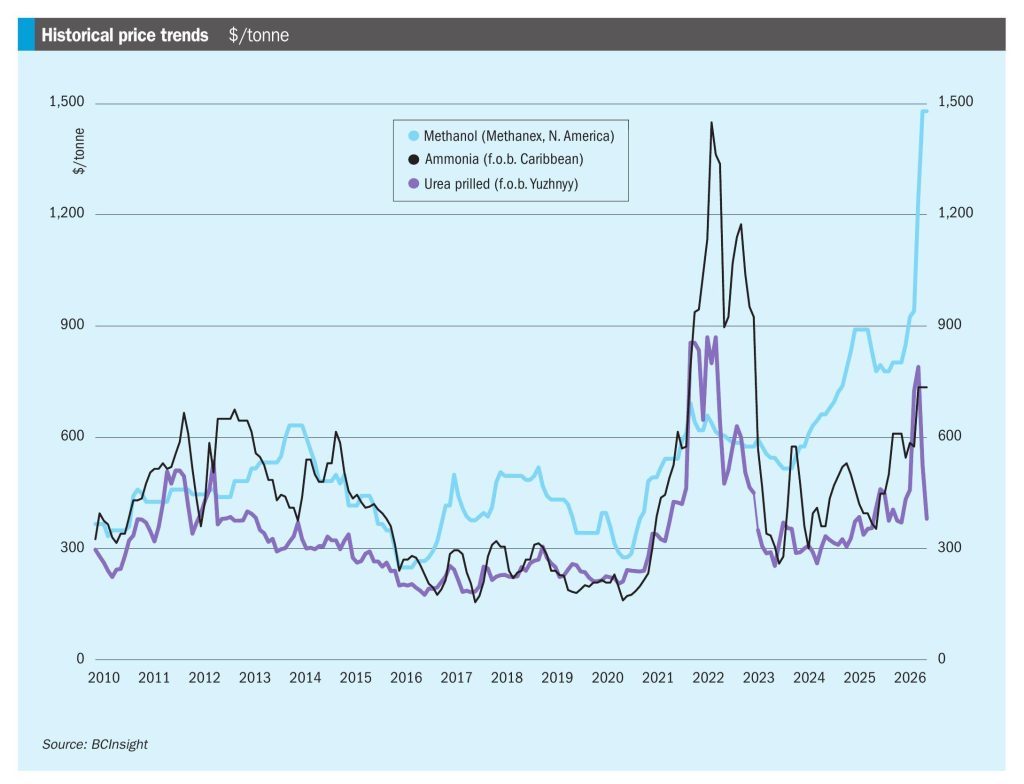

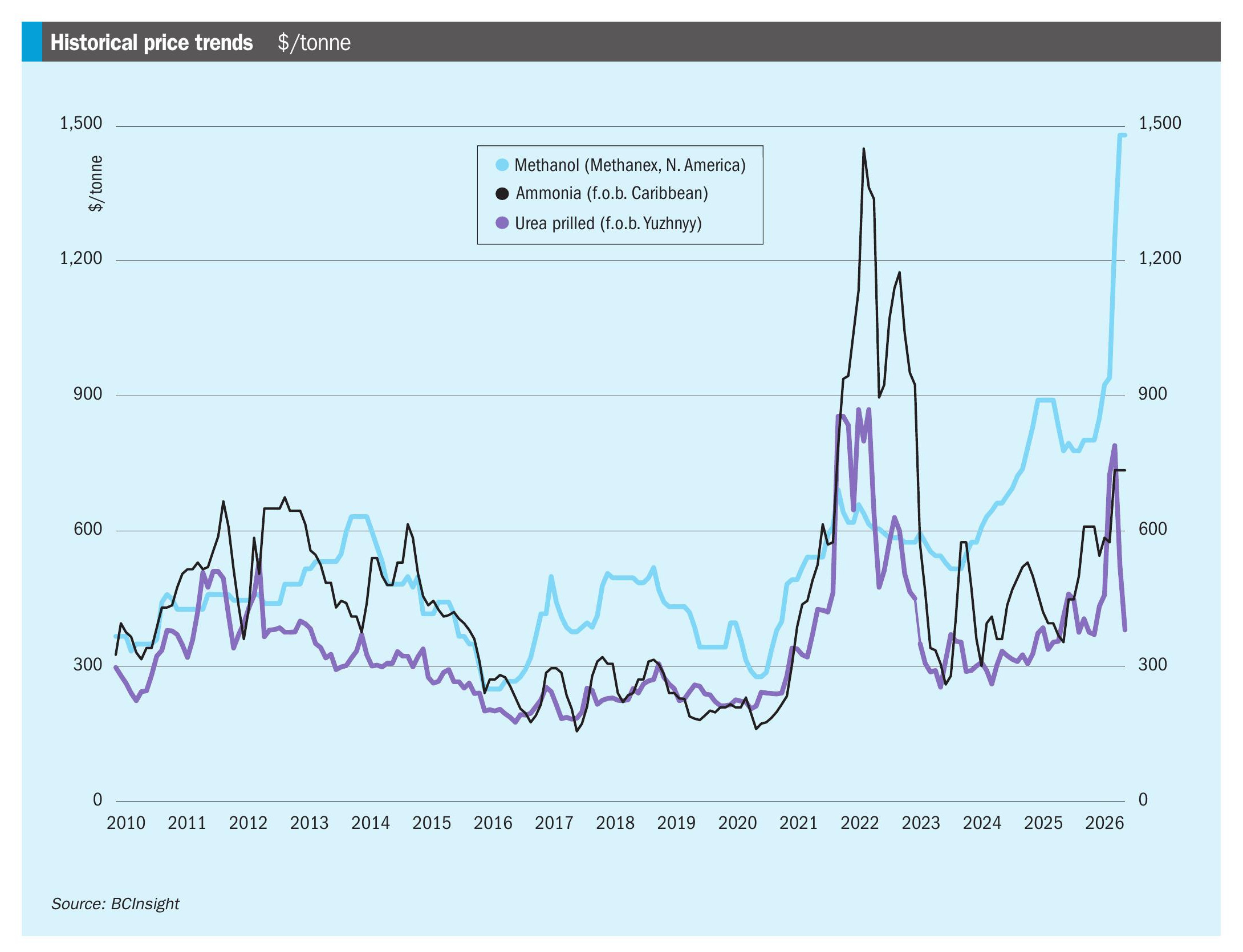

• Ammonia prices are expected to maintain their current downward trajectory, with the pace of correction likely to accelerate as the supply picture improves. Confirmed trades at materially lower levels remain limited, but the direction of sentiment is clearly softer.

• Nevertheless, market participants remain cautious regarding the pace at which Middle East supply will return to the market. Freight costs remain elevated, war risk premiums are still reportedly in place, and commercial caution persists around the route.

• US inland prices have been dropping sharply, with CF Industries launching a fill and prepay programme. It is widely understood growing length in the US Gulf market persists, supported by steady production at GCA and Beaumont.

UREA

• The easing of the situation in the Strait of Hormuz has seen dramatic declines in urea prices, with Middle Eastern f.o.b. rates halving in two months. Urea prices are now trading in what is a traditional range for this time of year. At least 17 vessels containing 427,000 tonnes of urea are known to have transited the Strait, with another 120,000 tonnes transhipped overland and exported via Oman.

• There were some concerns about a fresh attack on Ras Laffan near time of writing, but for the time being Middle Eastern prices were holding steady.

• The market is now looking for a price floor, with discussions at the IFA Annual Conference in Monaco at the end of June/start of July likely to be crucial.

• Further price easing is forecast over the year as supply improves, though policy and geopolitics will continue to drive volatility.

METHANOL

• In spite of record quoted prices for Methanex in North America, the company kept its June Asian reference price unchanged at $740/t, unchanged since April.

• Chinese spot prices were reported at $450/t, with declining operating rates at key methanol to olefins (MTO) producers leading to weaker domestic demand.

• Further relief is expected from the restart of Iranian production, with around 8 million t/a of capacity now believed to be operational again. Iran exported only 120,000 tonnes in April.

• Falling oil prices are expected to bring further relief to the methanol market, which tends to take its price cues from oil, but sluggish demand in construction and automotive sectors and overcapacity in olefins markets may keep demand constrained.