Nitrogen+Syngas 402 Jul-Aug 2026

13 July 2026

The market for ammonium nitrate

AMMONIUM NITRATE

The market for ammonium nitrate

The Ukraine war and associated tariffs and the EU’s carbon pricing system are keeping ammonium nitrate prices high.

Ammonium nitrate markets are ending the spring-summer period in a stronger position than many buyers had expected. What began as a story of weak demand and high affordability pressure has developed into something more durable: a market supported by supply disruption, elevated feedstock costs and new policy friction in Europe. The result is a sector that remains firm even where end-user demand is hesitant, and one where regional pricing patterns are becoming increasingly detached from the old seasonal playbook.

In Europe, the key issue is no longer simply whether buyers are willing to return to the market. It is whether the market can offer enough product at a price that makes sense once carbon costs, import barriers and gas prices are all taken into account. In the Black Sea, the question is whether Russian export volumes can recover quickly enough to ease pressure. In the US, the focus is whether seasonal demand can continue to support prices as the application window closes. And in Latin America, buyers are beginning to return, but later than usual, which may prolong the period of tightness in some trade routes.

Firm market

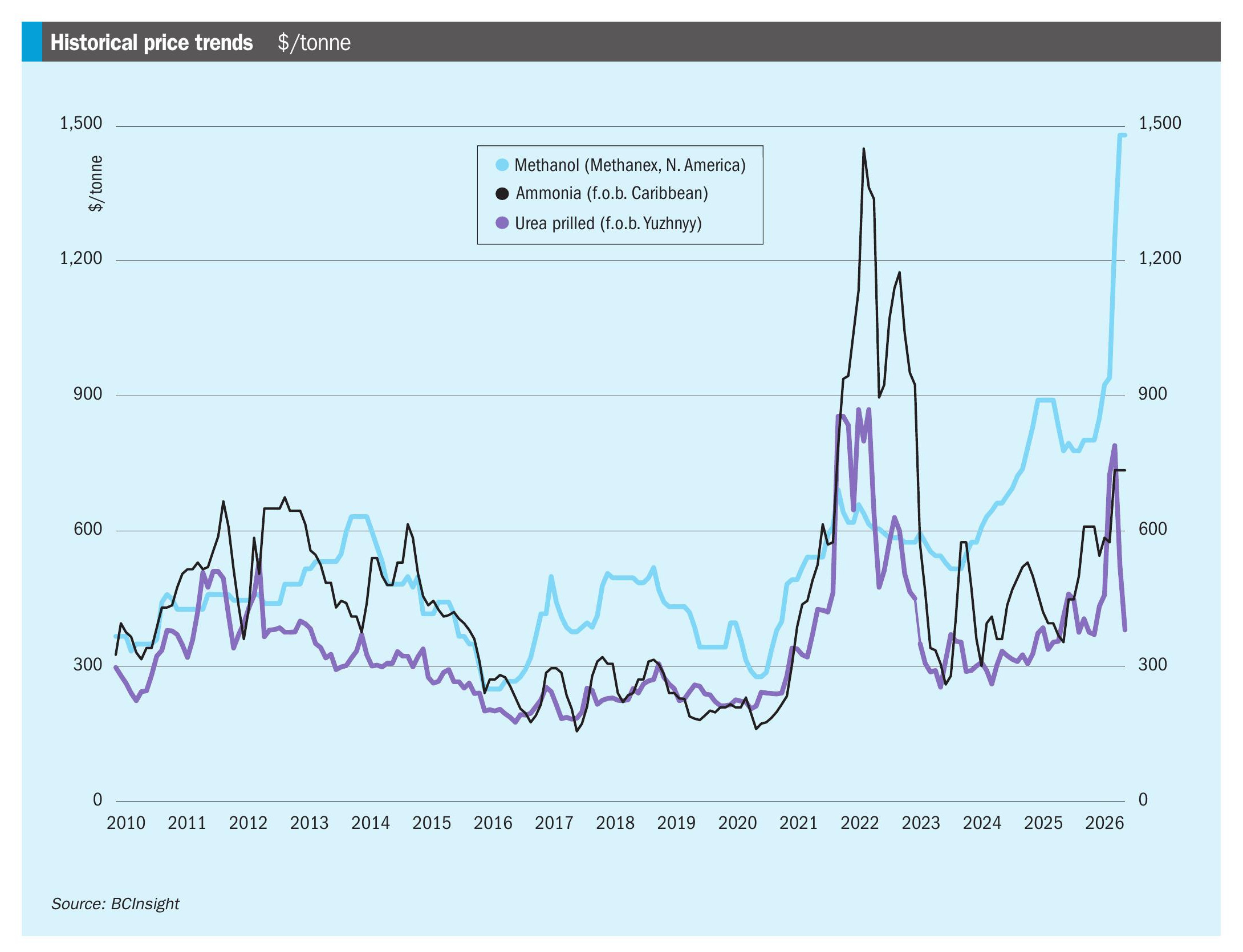

The current ammonium nitrate landscape is best described as firm rather than bullish. There is support under prices, but it is not coming from one single source. Instead, multiple factors are reinforcing each other. Firstly, natural-gas costs remain elevated, keeping producer economics under pressure. Second, firm urea prices are preventing a broader correction across nitrate products. Third, the Carbon Border Adjustment Mechanism (CBAM) and related import costs are making imports into Europe less attractive. Fourth, Russian supply has been disrupted by export restrictions and plant outages, removing tonnage from the market at a time when nearby supply was already limited.

At the same time, demand is not strong enough to create a runaway price environment. Buyers in Europe remain cautious, many entered the season with significant stocks, and the usual spring recovery was weaker than expected. Producers have therefore been forced to balance two conflicting objectives: defend margins without pricing themselves out of the market.

Europe the centre of gravity

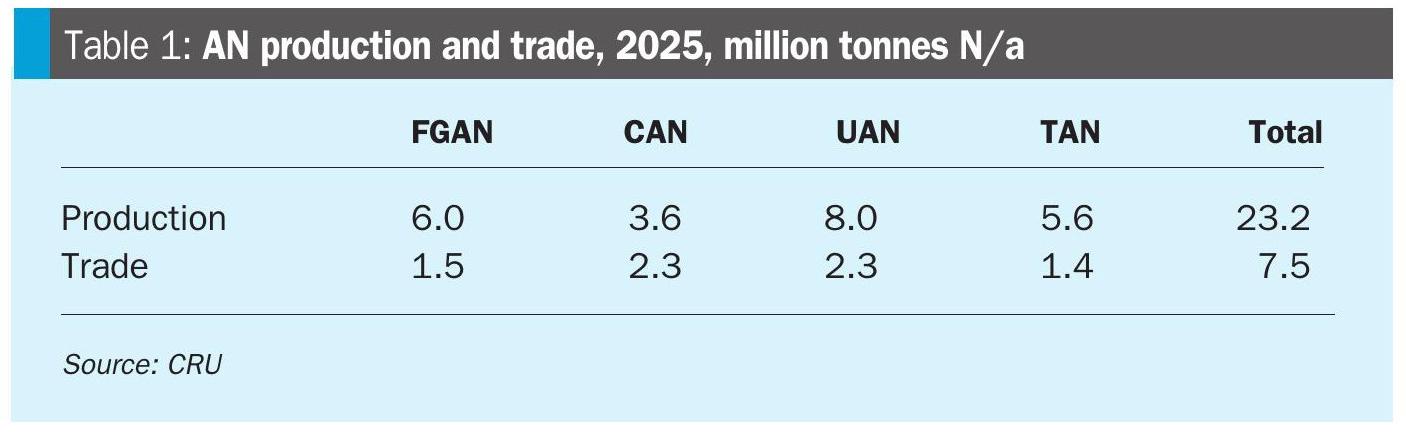

Europe is where the structural shifts are most visible. The region’s nitrate market has been shaped by seasonal buying, CBAM preparation and trade policy changes, but the biggest influence remains cost. CAN is comparatively less exposed to CBAM because it is mainly produced and consumed within Europe, where producers already face EU ETS costs. UAN is different however; roughly half of Europe’s UAN supply is imported, mainly from the US and Trinidad, which makes CBAM far more relevant for its landed cost. That has helped narrow the historic discount between UAN and CAN and, at times, pushed UAN into parity or even a premium. The suspension of Most Favoured Nation (MFN) nitrogen import tariffs in Europe has done little to change that picture. The estimated saving is too small to shift the market materially. What matters far more is the combined effect of carbon costs, logistics, and the underlying cost of production.

German CAN prices were revised higher in June, but the market still looks more like one of controlled easing than fresh strength. Buyers are pushing back against new-season offers, and producers still appear to have some room to reduce prices if they need to stimulate demand. French UAN is also expected to soften after June, although that easing is likely to be gradual rather than dramatic. French buyers remain notably price-sensitive, which limits the upside even when gas costs stay firm. The overall European picture is one of high but manageable prices, with producers protected by costs and policy, but buyers resisting anything that feels excessive.

Baltic AN remains tight

If Europe is the centre of gravity, the Baltic AN market is the clearest example of why the sector remains tight. The price has stayed elevated relative to last year because supply in the near term is simply scarce. Russian export restrictions have removed a substantial volume of product from the market. At the same time, several plants have been offline or under maintenance, including Dorogobuzh, Nevinka and Uralchem’s Azot plant at Bereznik. That combination has tightened availability through the early summer months and left buyers with fewer alternative sourcing options than normal.

The effect is amplified by the fact that Russian domestic price caps are setting a floor under export netbacks. In practical terms, that means exporters cannot simply discount heavily to regain share. So even where domestic demand is weaker, the export market does not automatically clear at lower levels.

There is still an upside risk. Further Ukrainian drone strikes on Russian nitrogen infrastructure could prompt additional export restrictions or prolonged outages. Market participants expect such events to remove tonnes that are difficult to recover quickly. That gives the Baltic market a vulnerability that could keep prices firmer for longer than buyers would prefer.

The US market is easing

The US UAN market has been strong through the spring, with prices reaching year-to-date highs. But the market is now moving past the most supportive part of the season. As the application window closes, the market is expected to soften. That does not mean US demand is weak. On the contrary, domestic demand has been solid enough to keep producers focused at home rather than on exports. But it does mean the market is entering a less supportive phase, where prices should retreat from their highs as seasonal buying subsides.

One important consequence is that US exports to Europe have fallen sharply. That has removed a key pricing floor from the European market. When those exports were flowing more freely, they helped define the lower boundary for European buyers. With that support reduced, Europe is more exposed to its own internal cost and policy dynamics. The expected US price easing is therefore less a sign of structural weakness than a normal seasonal adjustment. The market still has support, but the easy part of the upcycle is over.

Latin American demand to return

Latin America is not a source of immediate pressure, but it remains important to the overall balance. Buyers are expected to return later in the summer ahead of the coffee and sugarcane application season. That means demand is delayed rather than lost. The timing matters because it could prolong the period in which Russian tonnes remain difficult to place. If Brazilian and other regional buyers begin bidding later than usual, that may support Russian export volumes just as the Baltic market is trying to normalise. But for now, the market still looks relatively tight.

Latin America also matters because it illustrates how ammonium nitrate trade is becoming more seasonal and region-specific. The global market is not moving as one block. Instead, each region is responding to its own planting calendar, import economics and supply constraints.

Changing market structure

The bigger story is that ammonium nitrate is no longer trading in the same way it did before the current cycle of energy and policy shocks. The old assumption that prices would soften reliably after the spring season is less dependable now. Instead the market has become more structurally sensitive to gas prices, carbon policy, import tariffs, logistics disruption, and geopolitical risk. That is why the current tone is firmer than it might look from a purely demand-led perspective. Buyers are cautious, inventories are not especially tight in every region, and affordability is poor. But producers face a cost base that does not allow deep cuts, while supply losses in key export regions have kept the market from loosening materially.

Outlook

The next few months are likely to be defined by three questions. First, will gas prices remain high enough to keep European production costs elevated? Second, will Russian nitrogen infrastructure continue to experience disruption, or will export availability begin to recover more normally? Third, will buyers in Europe and Latin America return in sufficient volumes to give producers enough confidence to hold prices?

For now, the balance of evidence suggests the market will stay firm, with regional differences remaining pronounced. Europe will continue to be shaped by CBAM and carbon costs. The Baltic market will remain vulnerable to supply disruption. The US will ease seasonally. Latin America will return later. None of these developments points to a dramatic collapse in prices.