Koch to acquire half share in JFC 1

Koch Ag & Energy Solutions is buying a 50% share in Jorf Fertilizers Company I (JFC I) as part of a second joint venture with OCP Nutricrops.

Koch Ag & Energy Solutions is buying a 50% share in Jorf Fertilizers Company I (JFC I) as part of a second joint venture with OCP Nutricrops.

Nickel is becoming increasingly important to the sulphur and sulphuric acid markets, with Indonesia now a key importer.

Peter Harrisson, Principal, Sulphur & Sulphuric Acid Market Services, provides a brief snapshot of the global sulphur market at the end of June 2026.

The Ukraine war and associated tariffs and the EU’s carbon pricing system are keeping ammonium nitrate prices high.

VK Arora of Kinetics Process Improvements (KPI) compares the delivered-cost competitiveness of blue ammonia from regions including the US Gulf Coast, Western Canada, Atlantic Canada, the Middle East, Indonesia, and Malaysia into Japan, the European Union, and South Korea.

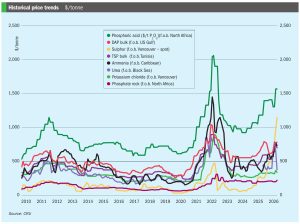

Price trends and market outlook, 17th June 2026.

Peter Harrisson , Principal, Sulphur & Sulphuric Acid Market Services, provides an overview of the global sulphur market.

We speak to Justin Rackleff, CRU’s Americas Lead, Fertilizer Value Chain, about the US market state-of-play ahead of this year's Southwestern Fertilizer Conference.

We interview Alison Coughlin, CME Group’s Director of Commodity Research and Product Development, about the valuable market role of fertilizer futures.

Egypt has introduced a 10% export duty on nitrogen fertilizers under Decree No. 258 of 2026, issued by Minister of Investment and Foreign Trade Mohamed Farid.