Nitrogen+Syngas 402 Jul-Aug 2026

13 July 2026

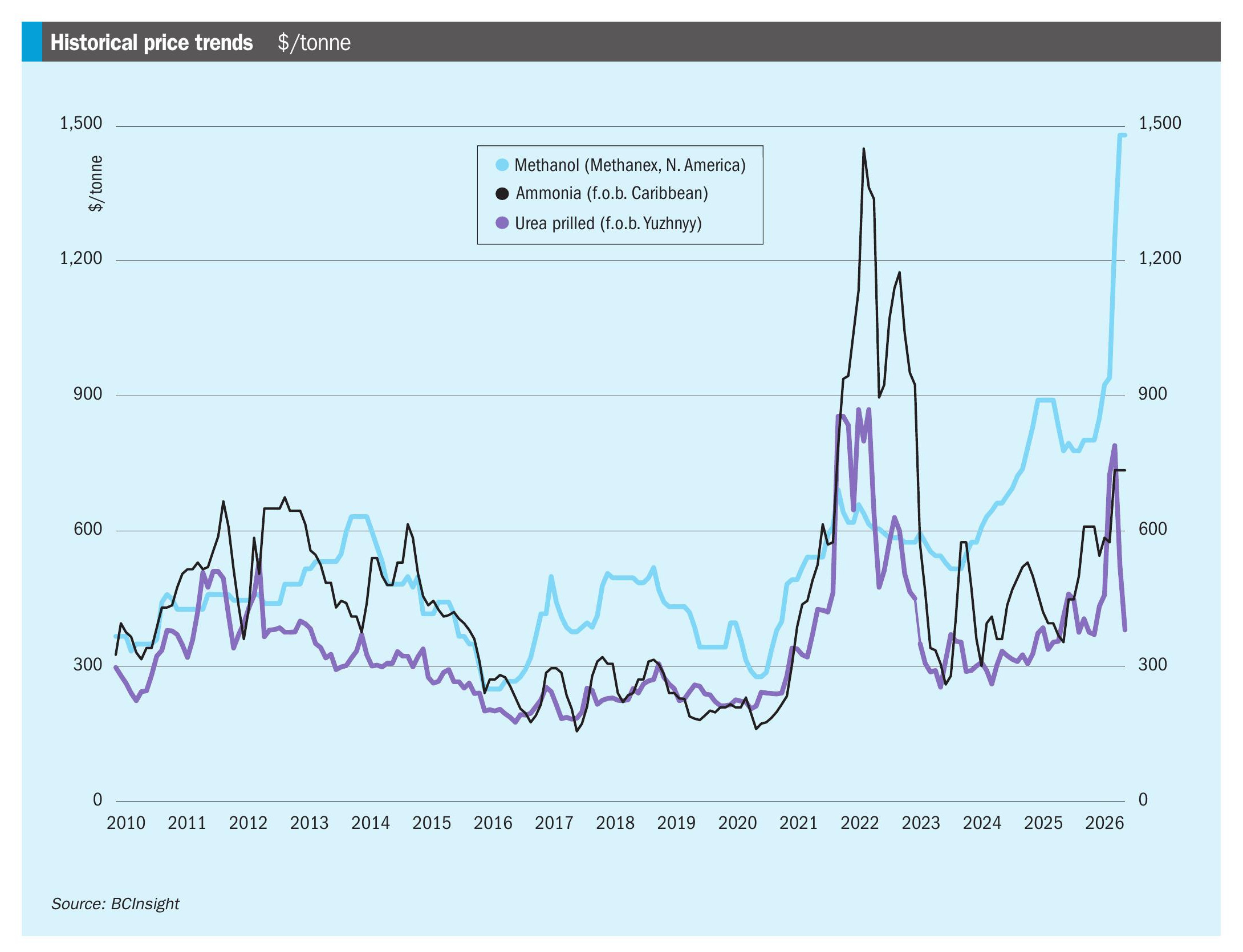

Price Trends

Price Trends

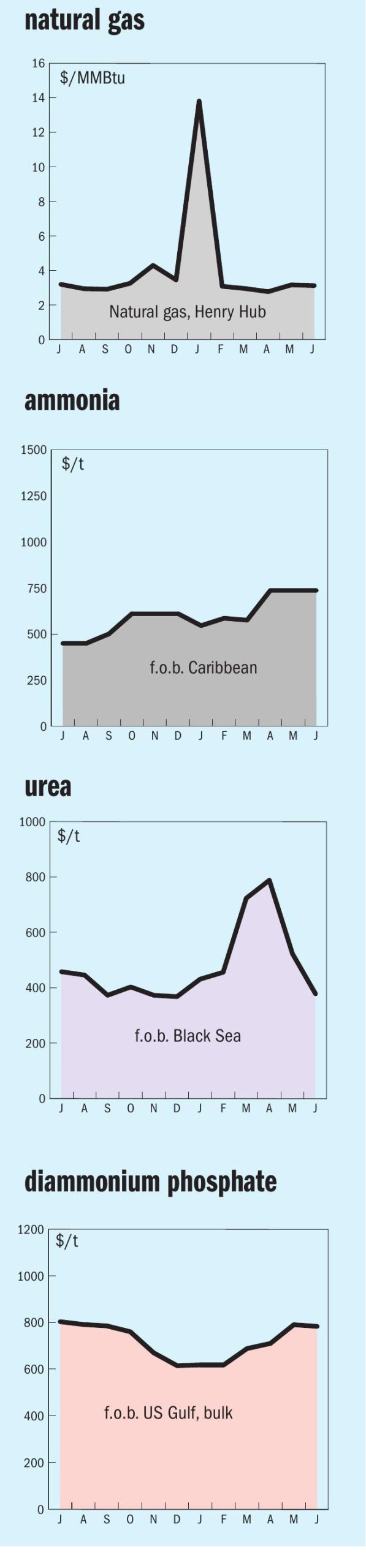

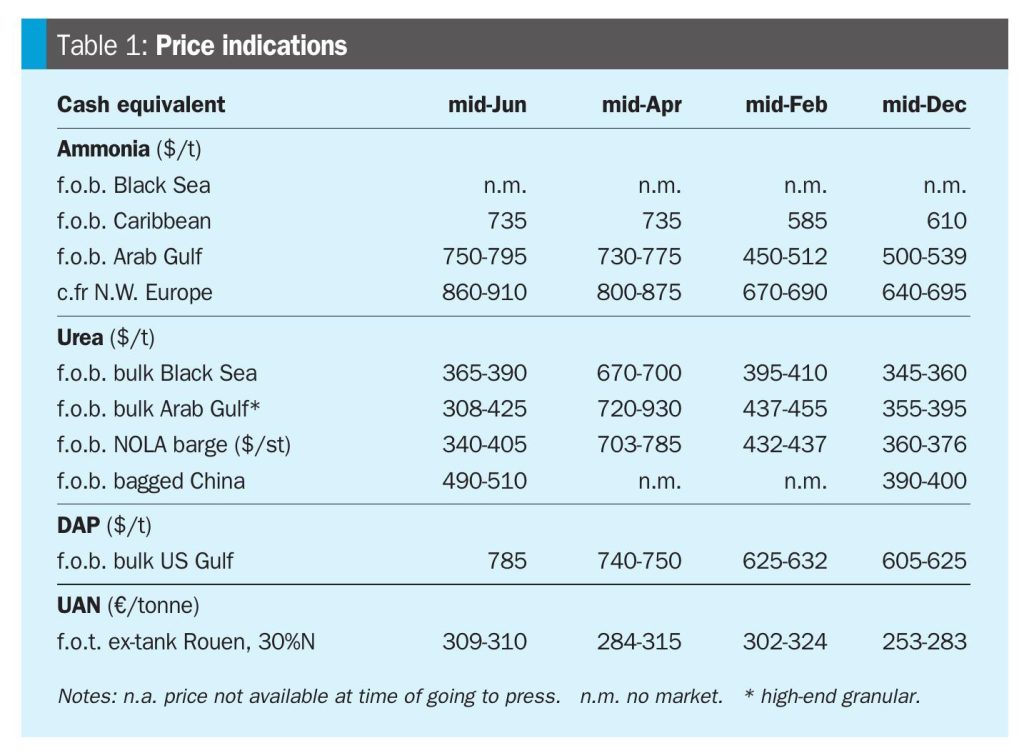

Ammonia values have continued to ease across most regions at the end of June, as the first ammonia vessels begin to exit the Gulf since the Iranian conflict began. Iranian ammonia had also begun to flow to India following the US Treasury’s issuance of a 60-day sanctions waiver on 22 June, allowing dollar-denominated trade in Iranian petrochemical products through 21 August. As a result, Indian bids have been heard as low as $750/t c.fr, as buyers benefit from a widening pool of available supply – Iranian, Chinese and renewed Southeast Asian material are all competing for the same business.

Chinese exports reached a record 185,022 tonnes in May, bringing cumulative January to May volumes to 462,322 tonnes, up 882% year-on-year, with f.o.b. offers dropping to the low $600s/t. In East Asia, spot values were heard to have declined to at and below $750/t c.fr for July. However, in Northwest Europe no fresh business has been for some weeks, and views on where prices have moved to vary widely. Seasonal demand continues to fade, and domestic production is running at strong rates. In the US, market expectations for the July Tampa settlement point to a decline of around $75/t to $700/t c.fr, although the earthquake in Venezuela has raised concerns over regional ammonia supply.

In urea markets, a sense of optimism has emerged following an apparent diplomatic breakthrough between the US and Iran. Since the deal, around 425,000 tonnes of ammonia has transited the Strait of Hormuz, though 618,000 tonnes remains within the Gulf. In India, NFL has issued Letters of Intent (LoIs) for just under 1.8 million tonnes of urea following its 8 June tender. Latest data for May showed a 12.7% year-on-year rise in production and a 41% increase in imports.

In China, a new, lower export price floor was set for destinations outside of India at $430/t f.o.b. for prills and $440/t for granular. In the Middle East, prices have continued to ease, with granular now indicated no higher than $400-410/t f.o.b. In Iran, amid a resurgence in production, the official producer price was slashed $10/t week on week to $365/t f.o.b. In Southeast Asia, prices were indicated in the $400-420/t f.o.b. range, with buying interest absent.

West of Suez, African producers have also seen prices soften. In Egypt, a tender sale by NCIC was reported at $425/t f.o.b., with the government also implementing a new 10% export tax. In Algeria, producers were understood to be targeting $450/t f.o.b., although as with price targets elsewhere, appetite at this level is likely to be limited.

The Americas saw further sharp declines. The US NOLA market continued to weaken, with July barges trading in the $345-360/st f.o.b. range. A cargo from Venezuela is also reportedly heading to NOLA for the first time since 2018. In Brazil, demand has picked up slightly, with prices noted just above $400/t c.fr.

European markets also remained quiet and under pressure. In the Baltic, prills sales to Brazil were reported in the mid-to-high $360s/t f.o.b. In the Black Sea, prices were indicated in the $370-390/t f.o.b. range. In northern Europe, prices in France extended declines as buyers shied away amid soaring temperatures.

END OF MONTH SPOT PRICES