EU unveils support for farmers hit by fertilizer costs

The Council of the EU has adopted a regulation giving member states new tools to support farmers hit by sharply higher fertilizer and input costs linked to the recent crisis in the Middle East.

The Council of the EU has adopted a regulation giving member states new tools to support farmers hit by sharply higher fertilizer and input costs linked to the recent crisis in the Middle East.

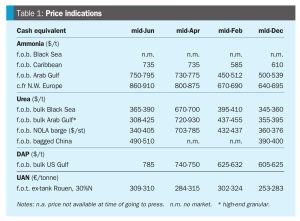

The Ukraine war and associated tariffs and the EU’s carbon pricing system are keeping ammonium nitrate prices high.

The signing of a memorandum of understanding between the United States and Iran on June 17th has provided relief across most markets as both sides agreed to allow ships to transit the Strait of Hormuz, at least in terms of trapped vessels from the Gulf being able to exit.

Ammonia values have continued to ease across most regions at the end of June, as the first ammonia vessels begin to exit the Gulf since the Iranian conflict began. Iranian ammonia had also begun to flow to India following the US Treasury’s issuance of a 60-day sanctions waiver on 22 June, allowing dollar-denominated trade in Iranian petrochemical products through 21 August. As a result, Indian bids have been heard as low as $750/t c.fr, as buyers benefit from a widening pool of available supply - Iranian, Chinese and renewed Southeast Asian material are all competing for the same business.

• Ammonia prices are expected to maintain their current downward trajectory, with the pace of correction likely to accelerate as the supply picture improves. Confirmed trades at materially lower levels remain limited, but the direction of sentiment is clearly softer.

Price trends and market outlook, 17th June 2026.

Peter Harrisson , Principal, Sulphur & Sulphuric Acid Market Services, provides an overview of the global sulphur market.

We speak to Justin Rackleff, CRU’s Americas Lead, Fertilizer Value Chain, about the US market state-of-play ahead of this year's Southwestern Fertilizer Conference.

We interview Alison Coughlin, CME Group’s Director of Commodity Research and Product Development, about the valuable market role of fertilizer futures.

The U.S. Department of Agriculture (USDA) has launched the $500 million Fertilizer Investment & Expansion for Long-Term Domestic Supply (FIELDS) Programme to expand domestic fertilizer manufacturing and reinforce the U.S. fertilizer supply chain.