North America

24 February 2026

The heat turns up on Mosaic and Nutrien

Written by Natalie Noor-Drugan

North American fertilizer majors Nutrien and Mosaic are coming under more scrutiny after corn grower groups urged the US Department of Justice (DOJ) to disclose progress on its probe into fertilizer pricing and market concentration, as phosphate prices remain elevated ahead of spring applications.

Two grower associations have pressed the issue this February: the Texas Corn Producers Association (TCPA) asked Attorney General Pamela Bondi for a formal status update, while the Iowa Corn Growers Association has also been pushing for tougher scrutiny and more transparency around fertiliser competition and pricing.

The growers’ latest letters land on top of a timeline of steadily escalating federal focus.

In September 2025, DOJ and USDA signed a memorandum of understanding to coordinate more closely on competition issues across agricultural inputs, including fertilizer, through regular consultations and information-sharing protocols. The agreement has become a focal point for US corn grower groups who are now demanding visible signs of progress.

In December 2025, President Donald Trump signed an executive order directing federal antitrust agencies to intensify scrutiny of price-fixing and anti-competitive conduct in the food supply chain, explicitly including fertilizer, and to pursue enforcement and regulatory responses where warranted.

Then, in January 2026, USDA Deputy Secretary Stephen Vaden sharpened the rhetoric by specifically naming Nutrien and Mosaic during a webinar hosted by the National Agricultural Law Center. Vaden called the two companies a “duopoly”, arguing that they constrained fertilizer supply and gained pricing power over farmers. The Trump administration would not allow them to undermine new competition, Vaden added.

“While I remain cautious about the likelihood of any near-term structural shift in supply policy, pressure is clearly building from farm groups and grower associations focused on input costs and access to product,” said CRU’s Justin Rackleff, Americas Lead, Fertilizer Value Chain, Intelligence & Prices.

“And although legislative and trade processes tend to move slowly, the volume and consistency of that pushback is becoming increasingly difficult for producers to ignore,” he added.

Competition and prices: how does it stack up

Nutrien and Mosaic have been singled out because they are the two largest incumbents in North American phosphate and potash—nutrients where critics argue concentrated capacity creates pricing power—and because USDA’s deputy secretary explicitly named them as a duopoly.

In the US phosphate market, Mosaic is the undisputed leader, while Nutrien holds a solid second place following its formation from the merger of Agrium and PotashCorp. Together, they represent over 90% of North American phosphate capacity. In third and fourth place are J.R. Simplot Company and Itafos, with just over 10% and over 5% of US capacity, respectively. Mosaic and Nutrien are also both the largest potash suppliers in North America.

Nutrien is not only a fertilizer producer; it also runs a major retail platform (Nutrien Ag Solutions). Farm Action, a farmer-led watchdog group focused on market concentration in agriculture, argues a large share of retail fertilizer sold through that channel is tied back to Nutrien’s own production.

So in a political narrative about ‘choice’, it is easy for some to frame Nutrien as having influence both upstream (production) and downstream (retail/service), while Mosaic is the undisputed heavyweight in US phosphate production.

A complicated supply picture

The underlying reasons for higher prices are, however, more complex than simple industry consolidation. Humphry Knight, Principal Consultant, CRU and Mariana Fortuna, Phosphate Analyst, CRU, argue that US phosphate prices have become the highest globally on a combination of declining domestic production, in addition to duties and tariffs raising import barriers to prohibitive levels.

Once the world’s largest producer and exporter of both phosphate rock and phosphate fertilizers, the US has seen granular phosphate production diminish substantially over the past decade. In 2024, combined US granular phosphate production of Mosaic, Nutrien, and Itafos fell below 8 Mt, one third lower than that achieved ten years prior, according to CRU.

The decline in US output of DAP+MAP has proven most acute. CRU estimates total US production has fallen by nearly 60% since 2010, with Mosaic’s output falling the fastest. The declining quantity and quality of US domestic phosphate rock supply, has acted as the primary driver of overall lower granular phosphate output and shows little sign of improving into the future. Producers have mitigated the issue by reducing exports and by changes to product formulations, which use less phosphoric acid and rock.

The domestic supply issue is colliding with a trade framework that has repeatedly raised the landed cost of imported phosphate into the US and reduced the pool of competitive supply options. The most direct example is US countervailing duties (CVDs) on phosphate fertilizer imports from Morocco and Russia —filed by Mosaic—where Commerce’s final determinations set subsidy rates including 19.97% for Morocco’s OCP and higher rates for named Russian producers, with the order issued in early April 2021.

Separately, the Trump administration’s ‘reciprocal tariff’ regime added another layer of uncertainty for fertilizer import flows, even as it was later narrowed for agriculture. While a White House order updated Annex II to remove certain imported agricultural products from reciprocal tariffs from 13 November 2025, it did not unwind the Morocco/Russia CVD regime.

In CRU’s view, the only way the US will materially improve its phosphate fertilizer supply is by a shift in trade policy. That said, under the country’s current administration, the prospect of such an outcome (either regarding the CVDs or the tariffs) looks similarly slim and substantial price premiums seem set to endure. Should such conditions persist, longer term, they could lead to a distortion in US nutrient application, potentially impacting crop yields, according to CRU.

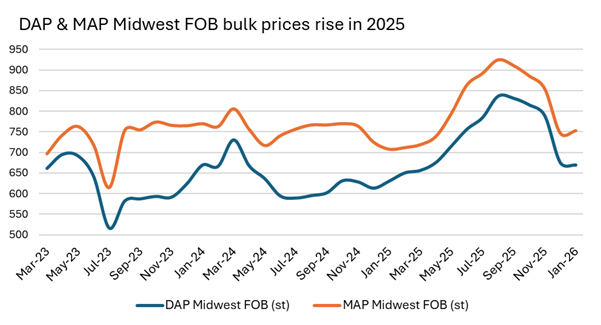

CRU’s Fertilizer Week data indicates phosphate pricing remains firm in the US interior. Midwest FOB DAP was $670/st in January 2026, up $39/st y-o-y, while Midwest FOB MAP was $753/st, up $45/st y-o-y. Month-on-month, DAP slipped $6/st from $676/st in Dec-25, while MAP rose $6/st from $747/st.

Main image taken from the White House, depicts President Trump after signing an Executive Order.