Fertilizer International 532 May-Jun 2026

27 May 2026

Fertilizer financial scorecard – a year of solid earnings growth

COMPANY ANNUAL RESULTS

Fertilizer financial scorecard – a year of solid earnings growth

We compare and contrast the 2025 financial performance of selected major fertilizer producers following the publication of fourth quarter results.

Stockpiling potash at Nutrien’s Cory mine site in Saskatchewan, Canada. PHOTO: NUTRIEN

Nutrien – improved performance across all operational segments

Nutrien is the world’s largest crop nutrient company with a market capitalisation of more than $36 billion (Figure 1). The Canadian fertilizer giant produces around 25 million tonnes of potash, nitrogen and phosphate products annually from operations and investments in 13 countries, and then distributes these to agricultural, industrial and feed customers across the globe. Its agriculture retail business serves more than 500,000 farmers worldwide through 2,000 plus retail outlets across the Americas and Australia.

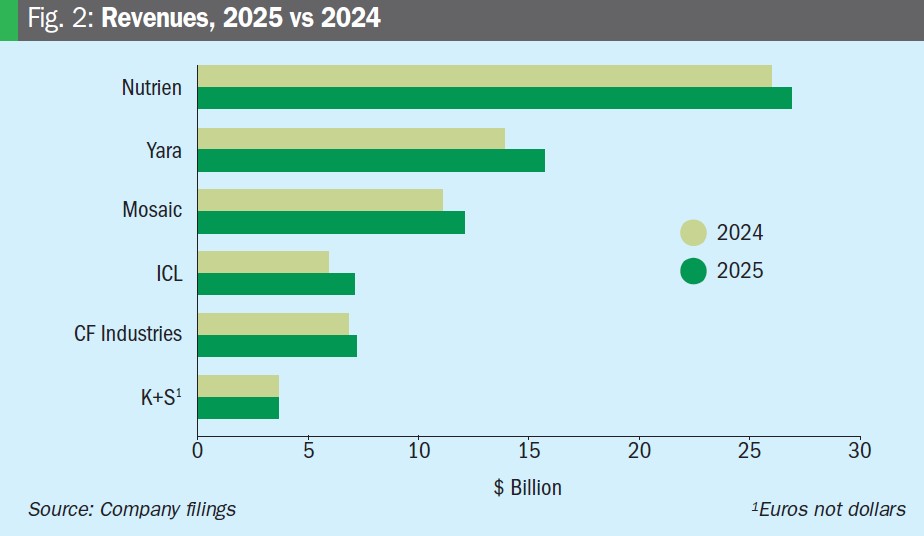

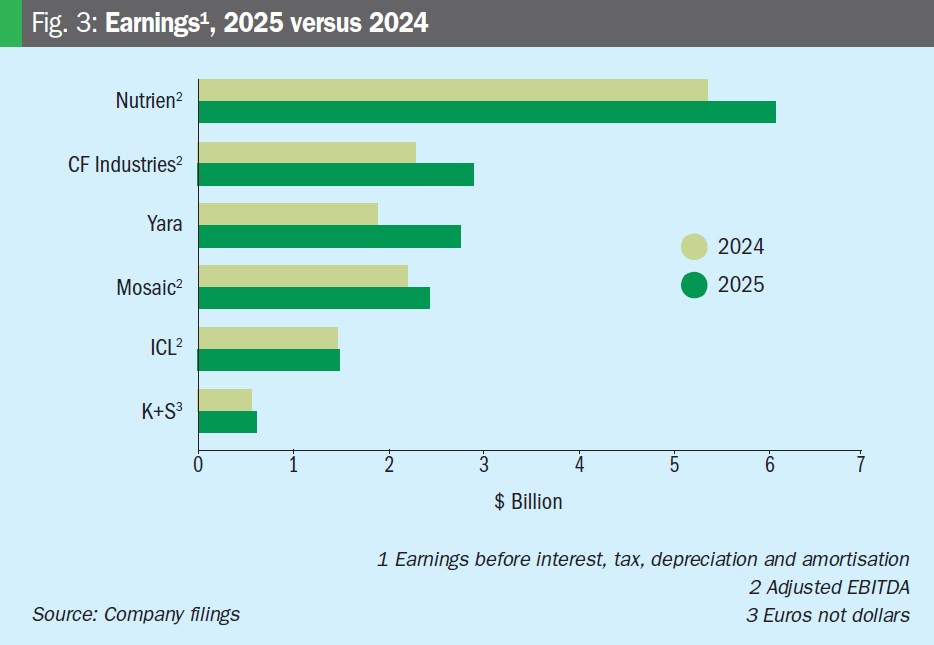

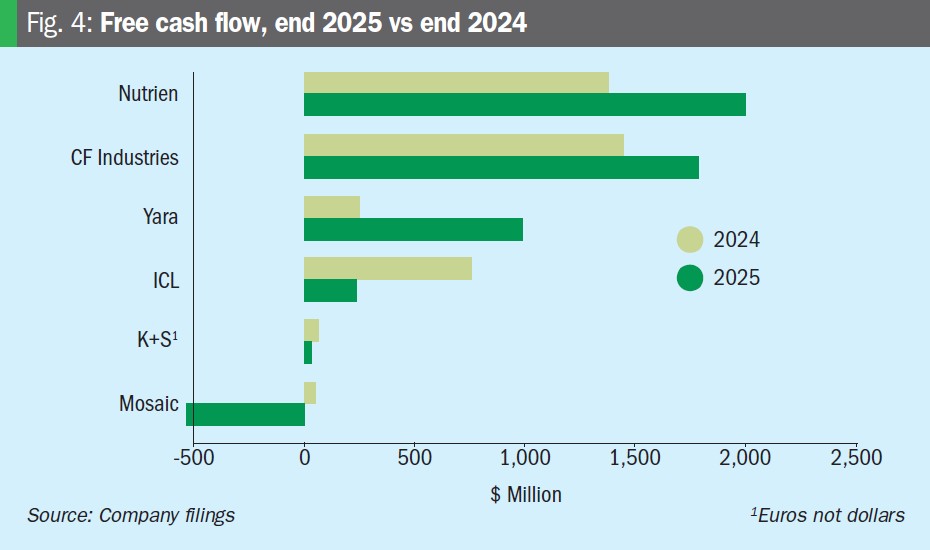

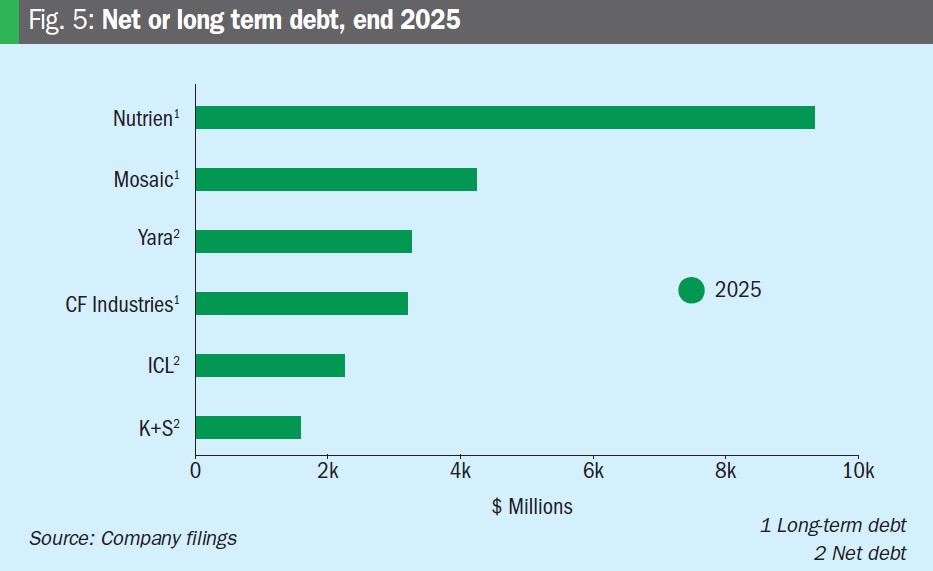

Nutrien’s revenues rose by 4% year-on-year (y-o-y) in 2025 to $26.9 billion (Figure 2). Similarly, annual earnings (adjusted EBITDA) for the year increased by 13% to $6.0 billion (Figure 3). Free cash flow, a measure of profitability, ended 2025 at $2.0 billion (Figure 4), versus $1.4 billion for the preceding year. While the company’s long-term debt increased last year – standing at $9.4 billion at the end 2025 (Figure 5) – its ratio to EBITDA fell to 1.5.

Nutrien linked its 2025 improvement in earnings to higher fertilizer net selling prices, record upstream fertilizer sales volumes and higher retail earnings.

Nutrien is the world’s largest potash producer. The company’s potash sales from its Canadian mines reached 14.3 million tonnes in 2025, a new annual record. Higher overseas sales volumes (9.6 million tonnes) were supported by strong potash affordability and consumption growth in key markets. North American sales volumes in 2025 (4.6 million tonnes), meanwhile, were stable y-o-y.

Potash accounted for 37% of Nutrien’s full-year earnings. Potash earnings, at $2.3 billion (adjusted EBITDA) in 2025, were up 20% y-o-y due to higher net selling prices and higher sales volumes, albeit partially offset by higher mining taxes.

The average cost of goods sold (COGS) for potash rose slightly to $111/t last year, mainly due to higher royalties, maintenance costs and depreciation. Nutrien mined almost half (49%) of its potash ore using automated methods in 2025, with this strengthening its cost advantage, according to the company.

Nutrien’s nitrogen earnings rose by 14% in 2025 to $2.1 billion. Higher net selling prices and slightly higher sales volumes (10.9 million tonnes for fertilizer, industrial and feed) were partially offset by lower equity earnings from Profertil. The average COGS for nitrogen products increased by 3% y-o-y to $219/t in 2025 due to higher natural gas costs, mainly driven by the Henry Hub benchmark.

Annual earnings at Nutrien’s retail business, Nutrien Ag Solutions, grew by 2% y-o-y to $1.7 billion in 2025, with the company citing factors such as cost savings, higher margins on proprietary products and the successful execution of a plan to improve retail margins in Brazil. Crop nutrient product sales were up by 1% on the previous year at $7.2 billion, mainly due to higher selling prices. Crop nutrient sales volumes in international markets, meanwhile, were lower in 2025. This was largely a consequence of strategic decision making in South America, the company said.

Nutrien’s phosphate earnings were down slightly y-o-y at $382 million. Higher sulphur input costs and lower sales volumes were only partially offset by higher net selling prices. Phosphate sales volumes were lower for the full year, down by 3% to 2.4 million tonnes, due to lower production volumes in the first quarter of 2025. The average COGS for phosphate products increased (+9%) to $657/t in 2025, primarily due to higher sulphur input costs.

Nutrien announced a strategic review of its phosphate business unit – by far its smallest operational segment – in November last year. Future options include a reconfiguration of operations, bringing in external partners or divestment.

“2025 was a defining year for our Company, with exceptional performance across all our operating segments and a reduction in cost and capital expenditures that surpassed our targets,” said Ken Seitz, Nutrien’s president and CEO. “Alongside delivering structural free cash flow growth, we took decisive actions to optimize our portfolio, strengthen our balance sheet and increase cash returns to shareholder.”

Looking ahead, Nutrien’s priorities for the current year are unchanged.

“As we move into 2026, we expect to build on our momentum supported by strong potash market fundamentals, an improved Nitrogen margin profile, and higher Retail earnings. I am excited about Nutrien’s extraordinary potential as we continue to position the Company for long-term growth and resilience,” Seitz added.

Yara – higher volumes and margins and lower fixed costs

Norway’s Yara International, with a market capitalisation of $14.7 billion (Figure 1) and 18,000 global employees, is one of world’s largest crop nutrient providers, vying internationally with Nutrien for leadership on production and deliveries.

The Oslo-headquartered company produced 20.0 million tonnes of finished fertilizers and 7.1 million tonnes of ammonia from its global assets in 2025. Finished fertilizer production included:

- 6.42 million tonnes of compound NPKs

- 6.02 million tonnes of nitrates

- 4.74 million tonnes of urea

• 1.73 million tonnes of calcium nitrate (CN)

• 0.92 million tonnes of urea ammonium nitrate (UAN)

• 0.14 million tonnes of single superphosphate (SSP).

Yara calculated that premium product sales in 2025 – namely its straight nitrate fertilizers and premium NPK offering – generated $1.4 billion in added-value, compared to the commodity fertilizer alternatives.

Yara’s deliveries rose by 3% y-o-y to 32.1 million tonnes last year. These were divided between:

- 23.8 million tonnes of fertilizers

• 6.4 million tonnes of industrial products

• 1.9 million tonnes of traded ammonia.

Regionally:

• European deliveries were 5% higher, driven by increased premium product volumes.

• In the Americas, deliveries were 6% higher, driven by NPKs and a recovery from lost sales in Brazil due to floods in 2024.

• Deliveries to Africa and Asia, meanwhile, were stable.

Yara’s annual revenues grew by 13% y-o-y to $15.7 billion in 2025 (Figure 2), while earnings (EBITDA) leapt by 45% to $2.8 billion (Figure 3). The drastic earnings improvement mainly reflected higher margins and volumes, according to the company, as well as a reduction in fixed costs. Free cash flow stood at $988 million at the end of last year, an increase of $782 million on 2024 (Figure 4), while the company’s net debt fell by $459 million y-o-y to $3.3 billion in 2025 (Figure 5).

Commenting on its full year results, Yara highlighted a strong performance based on higher deliveries and higher production – and its success in hitting targets for reducing fixed costs and capex set at the start of 2024.

Svein Tore Holsether, Yara’s president and CEO, said: “Yara delivers a strong quarter and full year for 2025. We have worked diligently to deliver on our cost reduction targets and sharpen our strategic focus to increase returns. I am pleased to say we have delivered on both, and we are well positioned to build on this momentum to further strengthen long-term value creation.”

Mosaic reports reliable production and progress on costs and efficiency

Florida-headquartered The Mosaic Company is the world’s leading combined phosphate and potash producer with a market capitalisation of $8.4 billion (Figure 1). The company sold around 23.9 million tonnes of products in 2025 – slightly down on 24.1 million tonnes in 2024 – with sales volumes split between three business segments:

• Potash segment: 9.0 million tonnes

• Phosphates segment: 5.9 million tonnes

• Mosaic Fertilizantes: 9.0 million tonnes.

Mosaic’s earnings climbed by 10% y-o-y to $2.4 billion (adjusted EBITDA) in 2025 (Figure 3). These results were achieved from full year revenues of $12.1 billion (Figure 2).

“Mosaic made significant progress in 2025. We fortified our assets to ensure reliable production, delivered meaningful cost and efficiency progress and divested non-core assets,” said Mosaic’s president and CEO Bruce Bodine. “Deferred demand and higher raw material costs negatively impacted our year end results, but demand is expected to recover as we move toward the planting season.”

The company’s potash earnings (adjusted EBITDA) totalled $1.2 billion in 2025, up from $944 million in 2024, with this largely reflecting higher sales volumes and prices. Mosaic’s potash sales volumes increased from 8.7 million tonnes in 2024 to 9.0 million tonnes last year. Compared to 2024, Mosaic’s average MOP (muriate of potash) selling price last year also increased by $33/t to $255/t. Its average gross potash margin for the year also increased to $97/t, versus the less lucrative 2024 average of $74/t.

Phosphate earnings (adjusted EBITDA) declined to $917 million in 2025, compared to $1.2 billion in 2024, with this reflecting higher cash costs and idling/ turnaround expenses, according to the company, partially offset by higher stripping margins and lower blended rock costs. Mosaic’s phosphate sales volumes declined from 6.4 million tonnes in 2024 to 5.9 million tonnes in 2025, while the average diammonium phosphate (DAP) selling price rose by around $85/t to $670/t. The gross average phosphate margin, in contrast, fell by $18/t to $74/t last year.

Full year earnings (adjusted EBITDA) at Mosaic’s Brazilian subsidiary Mosaic Fertilizantes, meanwhile, grew strongly by 65% to $567 million in 2025. This major earnings improvement reflected higher prices and improved operating margins, the company said. Full year sales volumes were stable at 9.0 million tonnes. Higher sulphur prices and a market preference for lower-margin single superphosphate (SSP) did, however, negatively affect fourth quarter (Q4) results: Q4 earnings (adjusted EBITDA) declined to $45 million in 2025, versus $82 million in Q4 2024. As a result, Mosaic temporarily curtailed SSP production at its Fospar joint venture and Araxa unit. These two sites together account for around 30% of Mosaic’s Brazilian production.

Mosaic Biosciences launched five new products in 2025 and doubled it net sales to more to $68 million. The company expects this relatively new but high growth business unit to launch 8-10 new products in 2026 and, again, double its annual net sales this year compared to 2025.

CF Industries – operational performance and market conditions drive strong results

Leading North American and UK nitrogen producer CF industries reported a significant upswing in both revenues and earnings in 2025. The Illinois-headquartered company has a market capitalisation of $19.7 billion (Figure 1). Full-year revenues ($7.1 billion) and earnings ($2.9 billion adjusted EBITDA) increased by 19% and 27% y-o-y, respectively (Figures 2 and 3). Full year net cash from operating activities ($2.3 billion) and free cash flow ($1.8 billion, Figure 4) were also healthy.

Average selling prices for 2025 were higher y-o-y for all product segments, as follows:

• Ammonia up by $48/t at $473/t

• Urea up by $79/t at $433/t

• Urea ammonium nitrate (UAN) up by $63/t at $311t

• Ammonium nitrate (AN) up by $31/t at $317/t.

These average price increases were driven by strong global nitrogen demand, supply disruptions from geopolitical issues and natural gas availability, according to the company. CF said its average cost of sales for 2025 was higher than in 2024, primarily due to higher realised natural gas costs. Its average natural gas cost last year was $3.31/MMBtu compared to the average of $2.40/MMBtu in 2024.

CF’s total production volume of 22.6 million tonnes in 2025 – up slightly on 22.4 million tonnes in 2024 – was split between:

• 10.1 million tonnes of ammonia

• 4.3 million tonnes of granular urea

• 6.9 million tonnes of UAN (32%)

• 1.3 million tonnes of AN.

Its total product sales volume (19.1 million tonnes) was also up slightly on 2024 (18.9 million tonnes).

“CF Industries delivered outstanding results in 2025, demonstrating the strength of our business and of our team,” said Chris Bohn, president and CEO, CF Industries. “We remain committed to creating long-term value for our shareholders through accretive investments both within our cost-advantaged North American manufacturing and distribution network and across our clean energy growth platform as well as through returning capital to shareholders.”

The company reported two asset impairments totalling $76 million in the fourth quarter of 2025.

One of these impairments ($51 million) relates to the Donaldsonville complex electrolyser project. The commissioning of the project’s 20-megawatt alkaline water electrolysis plant was suspended at the end of 2024. Further investment in the project, which would have produced green ammonia using hydrogen generated by the electrolyser, was ruled out in December 2025 following a review. This concluded that investing in carbon capture and sequestration (CCS) technology to produce low-carbon ammonia would generate better returns. CF is pursuing two CCS projects currently:

• The Blue Point joint venture with JERA and Mitsui. This $3.7 billion project will construct an autothermal reforming (ATR) ammonia production plant with a carbon dioxide dehydration and compression unit. This will enable CCS at the company’s Blue Point complex in Modeste, Louisiana. Detailed engineering is continuing and regulatory permits are being sought to enable construction to start in 2026.

• The Yazoo City CCS project. The company plans to transport and sequester, via permanent geologic storage, up to 500,000 tonnes of CO2 generated annually from ammonia production at the Yazoo City complex in Mississippi, under a definitive agreement with ExxonMobil. It is investing approximately $100 million in the project’s CO2 dehydration and compression unit at the site. Equipment is currently being ordered and detailed engineering is progressing with the aim of achieving startup in 2028. The company expects the project to qualify for tax credits under Section 45Q of the Internal Revenue Code.

CF also recorded a $25 million asset impairment following an incident at its Yazoo City complex on 5th November 2025. This sum is based of a preliminary review of the damage to ammonium nitrate production machinery and equipment. Production is not expected to resume at Yazoo City until the fourth quarter of 2026 at the earliest, based on time required for fabrication and equipment delivery. Due to this outage, the company expects to produce around 9.5 million tonnes of ammonia in 2026.

ICL highlights solid sales growth across its business segments

Israel’s ICL Group is a leading producer of potash, phosphates and specialty fertilizers with a market capitalisation of around $7.9 billion (Figure 1). The company delivered annual sales of $7.2 billion and earnings (adjusted EBITDA) of $1.5 billion in 2025 – up by 5% and 1%, respectively, y-o-y – along with free cash flow of $236 million (Figures 2, 3 and 4).

The company highlighted the growth in specialties-driven sales in 2025. It also distributed approximately $224 million in dividends to shareholders last year.

“ICL delivered a solid finish to 2025, with fourth quarter sales increasing 6% to $1.7 billion and adjusted EBITDA improving 10% to $380 million. All four of our segments delivered sales growth, with sales for our Industrial Products, Phosphate Solutions and Growing Solutions segments up 4% in the fourth quarter, and we remain committed to growing our leadership position in these segments,” said Elad Aharonson, president and CEO of ICL. “Throughout 2025, we benefitted from our distinctive global presence and relied on our regionally diversified operations to expand our specialties solutions offerings to our global customers using local production. This focus helped us to deliver a 5% increase in sales in 2025.”

ICL’s Potash ($552 million) and Phosphate Solutions ($528 million) business segments contributed 35% and 34%, respectively, to overall company earnings (adjusted EBITDA) in 2025. The Industrial Products segment ($280 million) also generated a 18% share of earnings, while ICL’s specialty fertilizer business, Growing Solutions, delivered the final 14% of earnings ($213 million).

ICL operates potash production assets in Israel (Dead Sea works) and Spain (Cabanasses mine). Total potash output in 2025 (4.4 million tonnes) was down by 125,000 tonnes y-o-y, mainly due to operational challenges. Potash sales (4.3 million tonnes) were 236,000 tonnes lower y-o-y, mainly due to lower production in the first half of 2025. Disrupted loading operations at Ashdod Port, linked to adverse weather conditions at the end of the year, also reduced sales volumes, primarily to the US and South America.

ICL’s Potash business unit generated relatively stable revenues of $1.7 billion in 2025. The company befitted from a higher average potash price (CIF) of $316/t in 2025, versus an average of $299/t in 2024.

Total revenues accrued by ICL’s Growing Solutions business segment were $2.1 billion in 2025. This segment markets and sells the company’s controlled-release fertilizers (CRFs), water-soluble fertilizers (WSFs), liquid fertilizers and straights (MKP/MAP/PeKacid), polyhalite products (FertilizerpluS), soil and foliar micronutrients, secondary nutrients, biostimulants, soil conditioners, seed treatment products and adjuvants.

ICL uses phosphate rock and fertilizer-grade phosphoric acid to produce phosphate-based fertilizers and value-added specialty products. The company’s Phosphate Solutions unit generated revenues of $2.3 billion in 2025.

Looking ahead, Elad Aharonson said: “For this year, we expect our two growth engines – specialty crop nutrition, which is part of Growing Solutions, and specialty food solutions, part of our Phosphate Solutions – to help drive improvement, and this will be via M&A, like our recent acquisition of Bartek Ingredients, and as we expand geographically.”

ICL is expecting earnings (adjusted EBITDA) of between $1.4-1.6 billion for 2026 with full year potash sales volumes of 4.5-4.7 million tonnes. The company is currently reviewing its capital allocation priorities, including:

• Discontinuation of its downstream expansion into cathode materials for LFP batteries.

• Divestment opportunities for its UK Boulby polyhalite mine as part of a review.

K+S meets upper end of its earning guidance

Revenues at K+S Aktiengesellschaft were stable y-o-y to €3.6 billion (Figure 2), while earnings (EBITDA) for the year were up by 10% percent to €613 million (Figure 3). The increase in earnings was attributed to higher prices for agricultural and industrial products. These factors, together with lower freight costs, more than offset higher energy and staff costs. The company generated free cash flow of €29 million in 2025 (Figure 4) while its net debt stood at €1.6 billion (Figure 5).

With a market capitalisation of $3.3 billion (Figure 1), K+S is western Europe’s largest potash producer, having a global market share of around nine percent. It also has a production presence in Canada, owning and operating the Bethune potash mine in Saskatchewan. The company is also enlarging its portfolio of specialty fertilizers. These products are chloride-free and/or supplement potassium with other elements such as magnesium, sulphur, sodium and micronutrients.

“Despite several negative factors, such as the unfavorable development of the U.S. dollar, we reached the upper end of our original EBITDA guidance range for the 2025 financial year,” said Dr Christian Meyer, CEO of K+S. “We succeeded in meeting our expectations with a slightly positive adjusted free cash flow despite elevated capital expenditures in our major projects,”

Revenues generated by the company’s two customer segments, Agriculture and Industry+, were broadly stable at €2.55 billion and €1.10 billion, respectively, in 2025. For its agricultural segment, price increases almost completely offset lower sales volumes and negative currency effects in overseas markets. K+S fertilizer products sold at an average price of €337/t in 2025 versus an average of €323/t in 2024. The company’s agricultural segment sold 7.57 million tonnes of fertilizer products in 2025, 4% down on the previous year, with this sales volume divided between 4.43 million tonnes of potash and 3.14 million tonnes of specialty fertilizers.

K+S is currently forecasting earnings (EBITDA) of €600-700 million for 2026. Reaching the upper end of this estimate assumes that Brazil’s potassium chloride price will recover during the spring season, compared to the mid-February 2026 price, with this price level then spilling over and being maintained in other markets during the second half of the year; it also assumes agricultural product sales of 7.6 million tonnes. ■