Fertilizer International 532 May-Jun 2026

28 May 2026

Market Insight

Market Insight

PRICE TRENDS

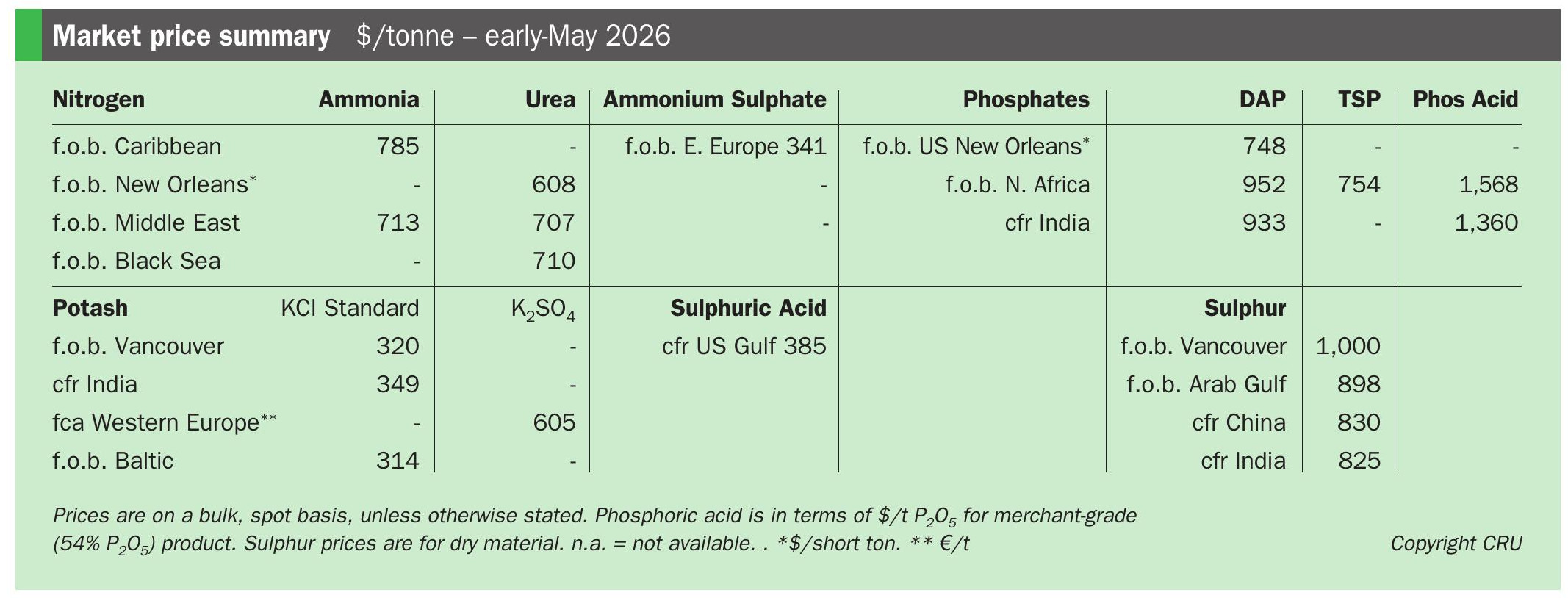

Market snapshot, 7th May 2026

Global urea prices continue their retreat. The downward correction that followed the conclusion of India’s recent urea tender gathered pace in some regions. The most significant business of the week was in Southeast Asia, where Malaysia’s Petronas sold 6,000 tonnes of urea at $790/t f.o.b. The sale marked a $120/t decline on the last confirmed regional business – a sale from Brunei at $910/t f.o.b. awarded two weeks ago.

Middle East activity remained subdued with urea prices lower at $800-830/t f.o.b. In the Gulf, reports emerged that QatarEnergy may have resumed production. Fertiglobe in the UAE also confirmed it was now trucking urea to ports outside of the Gulf to bypass the closure of the Strait of Hormuz.

In India, around 33 vessel nominations totalling approximately 1.43 million tonnes have been heard for Indian Potash Limited’s (IPL) recent urea tender. With domestic production recovering and stock levels healthy, the next urea import tender from National Fertilizers Limited (NFL) is not expected until late May or early June.

West of Suez, Egypt’s NCIC awarded its 4th May urea sales tender at $865/t f.o.b. The sale came as Cairo imposed a temporary $90/t export duty on nitrogen fertilizers. In the Americas, the NOLA market continued its slide, with a loaded urea barge traded at $585/st. The market in Brazil remains quiet, with delivered urea prices at $725-740/t cfr. In the Baltic, a Russian producer sold 10,000 tonnes of prilled urea to Latin America at a price netting back to the $690s/t f.o.b.

Global ammonia market quiet. In the Atlantic region, Trinidad tonnes are largely committed and demand from nitrates producers is steady. The absence of confirmed trades in Northwest Europe continued, with the $905/t cfr ex-Egypt deal from two weeks ago still standing as the last transaction. The May Tampa settlement at $825/t cfr, up $50/t from April, confirms that the Atlantic market remains tight, although the latest month-on-month increase is lower than April’s $160/t jump.

The ammonia supply picture East of Suez is more stretched. India’s IPL consortium tender for 521,000 tonnes – the first of its kind – illustrates the urgency of the ammonia procurement situation as the Kharif season approaches. Spot offers into Taiwan, China have been heard as high as $850/t cfr, while South Korean values are reportedly in the $750-770/t cfr range.

In Indonesia, PT Panca Amara Utama (PAU) began a five-week ammonia plant turnaround on 6th May. Yara’s Pilbara ammonia plant in Australia is also not expected to return until early June now.

Phosphates buyers cautious despite tight supply. Buyers across the globe are showing increasing resistance to price rises due to exceptionally poor affordability.

The key focus this week was on an unprecedented tender from India’s IPL for 1.2 million tonnes of DAP and 0.4 million tonnes of TSP. This drew offers of 2.325 million tonnes of DAP from 18 suppliers and 410,000 tonnes of TSP from four suppliers. The lowest offers for DAP were at $930/t cfr West Coast India (WCI) for 30,000 tonnes and $935/t cfr East Coast India (ECI) for 40,000 tonnes, both submitted by Indagro. The TSP lowest offers were both submitted by OCP – at $770/t cfr WCI for 150,000 tonnes and $775/t cfr ECI for 150,000 tonnes.

The current closure of the Strait of Hormuz is reducing phosphate exports from Saudi Arabia. All of Saudi Arabia’s phosphate facilities typically export through the strait, but producers are currently moving supply to the Red Sea coast, requiring thousands of cross-country truck loads per cargo.

Maaden says it can achieve three to 3-4 cargoes per month via this method. Sabic is also shipping via Red Sea ports. It has sold 50,000 tonnes MAP at $885/t f.o.b. Yanbu for May loading and 40,000 tonnes of DAP at $895/t f.o.b. Neom for June loading.

Modest potash price gains in US, Brazil, China. These prices rose marginally, driven by a slight uptick in demand and tighter supply. Brazilian MOP prices were assessed at $400-410/t cfr, compared with the previous week’s $400-408/t cfr price range. China’s port wholesale MOP price increased to RMB3,000-3,550/t fca, versus RMB3,000-3,530/t fca in the week prior.

Southeast Asian MOP prices were unchanged at $380-400/t cfr for standard grade and $410-450/t cfr for granular grade MOP. In the US market, the New Orleans granular potash price was reported at $330-340/st, a narrowing on the previous week’s range of $320-340/st.

Sulphur price increases pause as demand concerns grow. Most key benchmarks held steady after a period of relentless, record-breaking gains. The demand-side consequences of these historically high price levels – prompted by the supply-side shock from the Strait of Hormuz closure – are becoming an increasing focus.

The fundamental sulphur supply picture remains largely unchanged. A third vessel, the Richsing Lotus, successfully navigated the Strait of Hormuz this week, confirmation that a slow trickle of cargoes is emerging. With a significant number of vessels still stranded, these three passages have done little to alleviate the acute global tightness.

This reality is reflected in the Middle East, where official sulphur selling prices for May were set at record highs across the board: Adnoc’s OSP jumped $160/t to $760/t f.o.b., flanked by QatarEnergy’s QSP at $740/t and KPC’s KSP at $765/t.

In Brazil, the epicentre of the sulphur price rally, the market tested new highs with unconfirmed reports of a sale from the US Gulf at $1,150/t cfr.

OUTLOOK

Continued support for global urea prices. Rising demand in several key markets, ahead of peak application seasons, will confront ongoing supply tightness due to the Middle East conflict. Competition for May-June tonnes is set to be fierce. India will be competing heavily for volume, vying with both the US and Australia for available supply. The resolution of the US-Iran conflict remains uncertain and any failure in negotiations, or a premature end to the ceasefire, would see prices continue to climb sharply.

Ammonia tightness to persist. Prices are expected to remain elevated in the near term, with a series of supply outages further restricting an already short market. The scale of the supply loss from the Strait of Hormuz closure has been considerable. Any meaningful price correction is therefore contingent on a physical resumption of the Hormuz transit. Against this backdrop, CRU expects ammonia prices to remain elevated through May before beginning a more meaningful decline through the second half of 2026.

Granular phosphates prices to climb higher. CRU is forecasting price rises over the coming weeks and months, driven upwards by exceptionally tight availability for both finished products and raw materials. The Middle East conflict makes an earlier return by Chinese exporters less likely, with domestic prices elevated by high sulphur costs. Globally, prices therefore look set to climb higher still, unless the Strait of Hormuz rapidly reopens and/or China relaxes its export policy. Poor affordability remains the key factor limiting price upside.

Potash prices set to rise on logistical costs. MOP prices are expected to rise marginally in the near term due to rising freight, insurance and logistical costs. Potash will continue to remain the most affordable nutrient, however, despite these price pressures. Farmers are already capitalising on this relative affordability, building buffer stocks of potash ahead of potential price increases.

Upward sulphur price trend to continue. With no immediate resolution to the supply disruptions in the Middle East, the upward trend in sulphur prices is now expected to continue until July. ■