Fertilizer International 533 Jul-Aug 2026

8 July 2026

CME Group – providing transparency and managing risk in volatile times

INTERVIEW – THE FUTURES MARKET

CME Group – providing transparency and managing risk in volatile times

In increasingly volatile times, companies up and down the fertilizer value chain are being left exposed to price fluctuations. We talk to Alison Coughlin, CME Group’s Director of Commodity Research and Product Development, about the valuable market role of derivatives and the company’s recent introduction of a lower volume 10-Ton Urea US Gulf futures contract. This new smaller sized fertilizer contract allows a broader range of agricultural producers to participate in and access the futures market.

Introduction

Fertilizer derivatives – in the form of futures – have been offered by CME Group since 2011. They enable market participants to hedge their exposure to price volatility and shifts in fertilizer supply and demand. As well as mitigating risks, fertilizer futures also provide a signal to the broader industry about where fertilizer prices are today and, importantly, where they might be heading in the future.

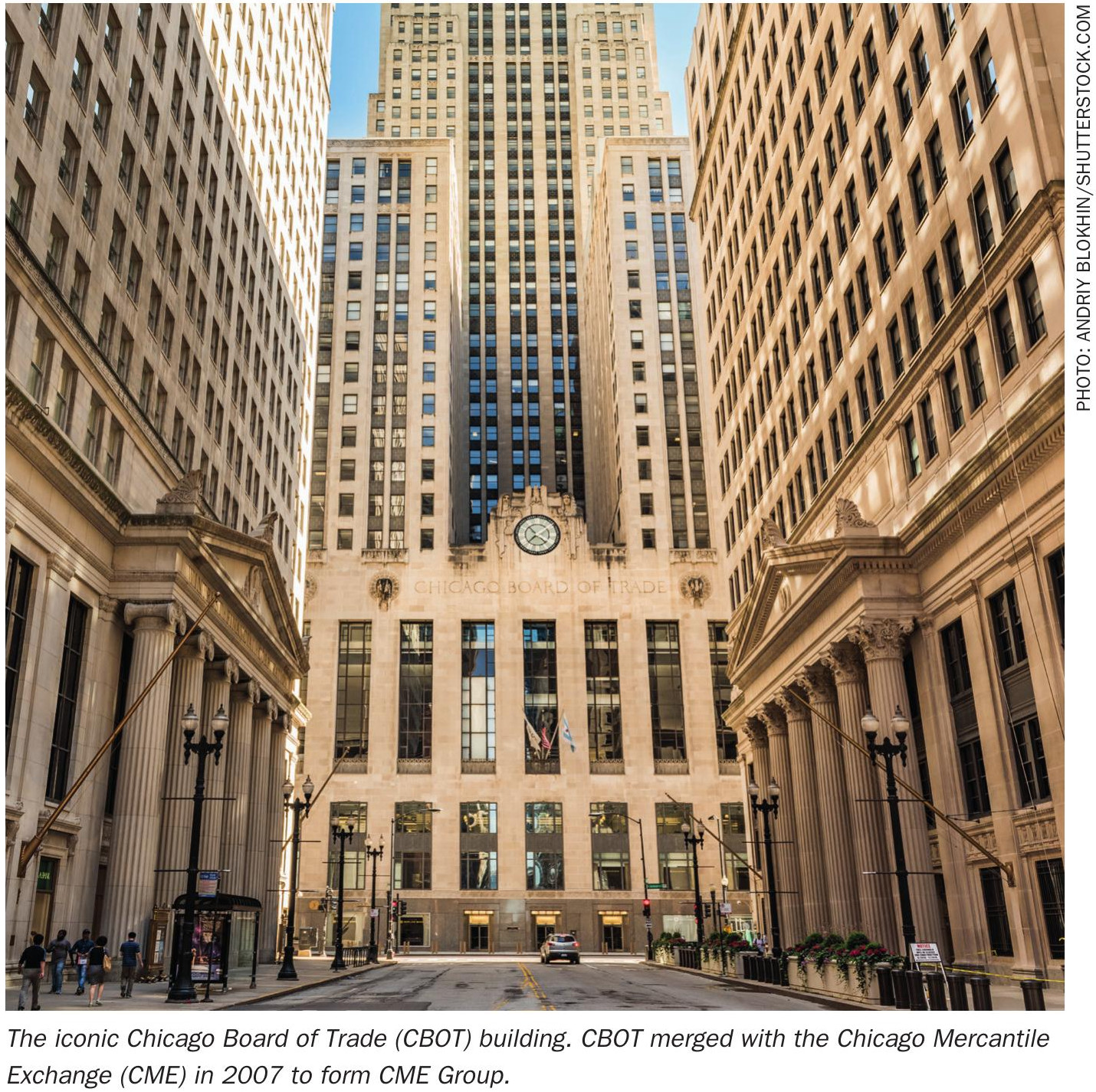

CME Group currently lists fertilizer futures for urea, urea ammonium nitrate (UAN), monoammonium phosphate (MAP) and diammonium phosphate (DAP), with these covering key price benchmarks in the United States, Brazil, Egypt and the Middle East (Figure 1). Each contract has a volume size of 100 tonnes – metric tonnes for the international contracts and short tons for the domestic US-based contracts. At the start of June last year, the company also introduced a new 10-Ton Urea US Gulf futures contract for electronic trading on its CME Globex platform and for clearing via CME ClearPort.

All fertilizer contracts on CME’s exchange are cash settled. This means that no physical product flows through the exchange when the contract expires. A final settlement price is determined at expiry and – instead of the seller transferring ownership of the product to the buyer – each entity settles their position by simply paying money or receiving money. In this way, no one with a position in the expiring futures contract is at risk of being compelled to either make or take delivery of a physical product.

The exchange determines the final settlement price from the Olympic average of the underlying price ranges – daily in the case of Urea US Gulf and weekly for other products – as provided by two price reporting agencies (PRAs). These daily and weekly numbers are averaged on the last Thursday of every month.

Private trades made off-exchange

Although many agricultural futures traded on the exchange are physically delivered and traded through CME Globex (CME’s open access trading platform and electronic order book), the vast majority of fertilizer participants access futures contracts through privately negotiated trades executed off-exchange using CME ClearPort.

This allows market participants to process over-the-counter (OTC) financial and physical transactions backed by the security of a centralised clearing house.

Any entity wanting to engage in a fertilizer trade can contact a brokerage firm. These brokers will then find a counterparty, aligned on quantity and price, and submit the trade to CME ClearPort. The minimum transaction size for these block trades is two contracts. In practice, however, US-based contracts tend to trade in increments of 15 lots and international contracts tend to trade in increments of 50 lots.

Brokers, by providing a forward curve for daily settlement prices, play an important role in the fertilizer futures market. Approved brokers submit daily quotes to the exchange. These indicate the price of a given commodity at a specific time of day. The exchange then determines the daily settlement price for the expiry of each individual product by aggregating and blending all the submitted broker contributions. Daily settlement prices are a major tool for alerting the broader industry to price movements and an absolutely crucial input in mark-to-market calculations.

“We offer a diverse portfolio of fertilizer risk management tools and have expanded into this 10-Ton option on the Urea US Gulf contract. So we are responsive to customer needs and what kind of contracts they’re looking for, whether that’s new fertilizer products or new fertilizer geographies.”

Going short or long

Those who might benefit from an increase in the futures price, or who are looking to mitigate any potential increases in cash prices, can hedge by buying futures. Generally, these types of hedgers are actual fertilizer buyers in the cash market. If prices do increase, they end up paying more for their physical fertilizer purchases. Yet, through hedging, such losses are offset by corresponding gains in the futures market by selling the position at a price higher than they bought it for.

Conversely, those who produce fertilizers and could be negatively impacted by fertilizer price reductions can sell futures, also known as taking a short position. If prices do decrease, these producers, while receiving lower prices in the cash market for their product, will have made gains in their futures position.

We sat down with Alison Coughlin, CME Group’s Director of Commodity Research and Product Development, ahead of Southwestern Fertilizer Conference in New Orleans, for a deep dive into fertilizer futures, price transparency and risk management.

Pioneering fertilizer futures

Alison, CME Group has pioneered the market for fertilizer derivatives since their introduction in 2011. How important is the fertilizer futures market and how is this positioned within CME’s broader agricultural commodities offering?

“Fertilizer futures were unique to CME and, yes, pioneering for a couple of reasons. They were some of our first cash-settled contracts.

“Fertilizer futures proved to us that there were ways of looking at agricultural commodities that weren’t necessarily just through physical delivery or USDA-reported numbers. Instead, we could partner with price reporting agencies (PRAs), if that’s how the underlying physical market priced their commodity.

“The price reporting agency model for fertilizers was also very different for the agriculture space and unique. Cattle and hogs were cash settled, but to USDA rather than a PRA. Private block trades were also new to ag and again unique in that, back then, almost everything else traded on the screen.

“So, fertilizers are definitely a unique product suite for all those reasons – and for their diversity too. By that, I mean corn is corn, right? If you’re in China, if you’re in Brazil, you are talking about the same, single commodity. Wherever it’s from, wherever it’s going, it’s very commoditised.

“While in fertilizer, you have urea, UAN, DAP, MAP, you have sulphur, ammonium sulphate, you have this broad range of products and geographies. CME had a lot of straightforward US-based commodities, whereas there are so many different geographies that play a key role in fertilizer pricing. Having urea, UAN, MAP, and DAP products based in the Middle East, China, Brazil, US, North Africa within one product suite is pretty unique on the agricultural side.

“We have global participation in fertilizer futures, just like the rest of our products, mostly North American, but certainly some EMEA and APAC participation. That’s true across the suite.

“Fertilizers are also more bilaterally traded – versus many of our other agricultural products traded on the screen – and more heavily commercial.

“There’s also a large over-the-counter (OTC) market. Every commodity has this, but in the fertilizer suite it’s definitely pronounced. With OTC contracts cleared using CME ClearPort, we act as the buyer to every seller and the seller to every buyer. What’s key for us, and gets to the heart of those contracts, is that we stand in the middle of all transactions.”

A spotlight on transparency

Are fertilizer derivatives an important way of understanding the pricing relationships between fertilizer commodities – such as urea, UAN, MAP and DAP – across the globe?

“I give a lot of presentations to groups across commodities and I often say futures really have a few key purposes – and the first one is price transparency. It’s so key because that was how the Chicago Board of Trade was founded.

“There’s also a large over-the-counter (OTC) market in the fertilizer suite. With CME ClearPort, we act as the buyer to every seller and the seller to every buyer. What gets to the heart of those contracts is that we stand in the middle of all transactions.”

“Back in the 19th century, there were farmers who would literally bring their harvest up to Chicago and merchants would stand around the city and buy these commodities. And in 1848, 12 businessmen said, ‘What if we put this in one location?’ So every time a transaction was made, they’d write the price and quantity on a chalkboard – and that was the start of the futures and price transparency that we now have today.

“What’s really amazing is this is available to the entire world. You don’t have to be a market participant in order to benefit from this transparency. Anyone can go to CME’s website and see what the price of a commodity is. And it’s not us determining that price, it’s the marketplace, buyers and sellers coming together to determine what that price is.

“There is value in knowing, ‘Urea US Gulf is trading at X dollars today.’ But because we list out 12 months, anyone can go on our website and see where the market is pricing fertilizer months from now. That transparency is the basis for futures and is why futures exist, although it is only the start. There are many things that you can do once you have that price transparency and once you know how the market is valuing any commodity.

“Talking about the products that we offer, we have Urea US Gulf, which is our most liquid 100-tonne futures contract. So, we have options on the urea US Gulf contract, we have urea Egypt, urea Middle East, and urea Brazil – and then we also have DAP NOLA, MAP Brazil, and UAN NOLA.

“The impetus for our new 10-Ton Urea US Gulf contract launched about a year ago was price transparency. We had this barge-size 100-Ton Urea US Gulf contract but US agricultural producers were saying, ‘I have fertilizer risk and I need something to offset that risk.’ These ag producers do have this inherent exposure to fertilizer price – it can be up to 30% of their input costs.

“The 100-Ton Urea US Gulf contract is almost always transacted in barge-size 15 lots. That was partly why we moved forward with this more producer-centric 10-Ton contract. We put it on the screen and it’s still pricing the Gulf, but agricultural producers and anyone in the market can have access to it – getting transparency out there was really key for us.

“Now we have this very interesting global picture that means farmers are arguably even more exposed to global supply and demand fundamentals than they have been in prior years. The 10-Ton Urea US Gulf contract has really come into its own at this particular moment. It trades most days and has a good bid offer range. It’s incumbent upon us to educate the market, but there are certainly a lot of people paying attention to this contract and where it’s pricing and how it works.”

Locking in prices

Firms with any physical exposure – typically fertilizer producers, distributors and buyers – can effectively lock in prices for any product they hold by taking a position in the futures market. Could you provide examples of how this might benefit market participants?

“Another purpose of the futures market in commodities – once the price is transparent – is how do you manage price risk? That’s where the concept of hedging comes in. It relies on this relationship between futures prices and cash prices. The reason that is important is because hedgers can take an opposite position in the futures market from their cash position.

“If I’m a grain producer exposed to fertilizer prices going higher, I can take a long position and buy a futures contract, because if the price goes up I can sell that for a gain. If I have to buy fertilizer in the cash market for a higher price, the gain in my futures account can offset that cash price rise.

“Similarly, if I’m a fertilizer producer my risk is that the price goes down. So I take a short position in the futures market which means I sell a contract. To get out of that contract I can either buy it back or let it expire.

“I always tell people hedging is protection – it’s a way to lock in margin. Also, because futures contracts are cash settled, no one has concerns over physical delivery. Really, the contracts are written and are designed to be commercial hedge tools. So someone can offset in the futures market the exposure risk they have to cash market swings. The market needs speculators to come in and take on risk, whereas the hedger’s job is to lay off risk.

“The 100-Ton Urea US Gulf contract is almost always transacted in barge-size 15 lots. That was partly why we moved forward with this more producer-centric 10-Ton contract.”

“A lot of agricultural producers will think in terms of how many bushels of corn does it take to buy one ton of fertilizer. If they expect the fertilizer price is going to go higher, they will have to produce more bushels of corn to buy one ton of fertilizer. So, the ability for producers to lock in that ratio – by taking an offsetting position in the futures market – is an important advantage.”

The buyer to every seller and the seller to every buyer

The vast majority of fertilizer futures contracts use CME ClearPort for privately negotiated trades executed off-exchange. What’s behind this preference for over-the-counter (OTC) transactions versus a traditional trading platform and electronic order book such CME Globex?

“That’s a great question. Like I said, it’s unique that the percentage of these bilateral trades that are submitted for clearing account for a much higher percentage in fertilizer than they do for any of our other agricultural products.

“Just to be clear, these over-the-counter transactions (OTC) that brokers put together can either be cleared or uncleared. Sometimes the counterparties will agree to retain the counterparty credit risk off-exchange or they will say ‘put this through CME clearing so that we have all the protections that a clearing house will give’ and we then guarantee the transaction.

“The [CME ClearPort] clearing house provides a service that in uncleared transactions does not exist. We are monitoring our markets to make sure that they are orderly and dealing with the entire ‘pays-and-collects’ process daily and on final settlement.

“There are a couple of reasons why fertilizer transactions continue to be more privately negotiated versus on the screen trades. The fertilizer industry is more heavily concentrated than many other agricultural industries with a lot of large corporations who can do privately negotiated trades. You have to be an eligible contract participant in order to do a block trade. All of the large fertilizer commercials are easily eligible as contract participants, whereas many US grain producers, who may be hedging corn or 10 tons of fertilizer, are not.

“There is also some comfort in showing your business to a broker and allowing that broker to find the counterparty as opposed to putting it on a screen for anyone to transact with. There may be existing cash relationships in place and brokers play a really pivotal role in that. We look at how markets are currently structured so we are not disenfranchising any of the existing participants in the supply chain. The physical fertilizer market relies on these brokers – therefore the futures market should look similarly.

“I always tell people hedging is protection – it’s a way to lock in margin. Also, because futures contracts are cash settled, no one has concerns over physical delivery. Really, the contracts are written and are designed to be commercial hedge tools. So someone can offset in the futures market the exposure risk they have to cash market swings.”

“Our job within CME research is to make sure that the way the futures work mimics the way the cash market works. Brokers are such a pivotal part of this fertilizer supply chain that we want to empower them to submit trades how they see fit.

“Our on screen trading platform is always available and we always offer the ability for people to post bids or offers on that transparent marketplace. We also report all of the privately negotiated trades that are submitted for clearing. Those all need to be reported within a certain window and are public information.

“Those are some of the reasons why this market continues to be more privately negotiated with many of those trades being submitted for clearing through CME ClearPort. We’re agnostic about how the market wants to trade, whether that’s privately negotiated or through trades on the screen. We just want our tools to be there regardless of how people choose to execute.”

Ever higher volumes

Has CME seen an increase in the volume of futures contracts traded over the last 12 months?

“We have seen continued growth over 2026 with a couple hundred more transactions volume-wise versus 2025. We’ve also seen a pretty significant jump in open interest. Those are two different things.

“If I go in and I buy or sell a futures contract that counts as volume. But if I buy a contract and leave my position, don’t sell out of it, that’s open interest. So both volume and open interest are key indicators of a healthy market. You like to see growth in both, with some people holding their positions and other people engaging in trading activity. We have seen a significant jump in open interest contracts year-on-year during the first five months of 2026 – 321,261 for 2025 and 339,122 this year.

“Generally, Urea US Gulf is going to be the most liquid. It’s what a lot of people, even internationally, will base their contracting on. That continues to be our biggest contract most of the time. Which contract gets hot just depends on the market and where people want to put their liquidity. Occasionally, Urea Middle East will give it a run for its money, especially depending on what we’re seeing right now with the Strait of Hormuz.

“The January-May Urea US Gulf volume stats are interesting: 2025 was 144,351 contracts and 2026 is 180,622 contracts. Then Urea Middle East for the first five months of last year was 54,800 contracts and this year, unsurprisingly, we’ve seen a significant increase to 79,020 contracts.

“This market continues to be more privately negotiated with many fertilizer trades being submitted for clearing through CME ClearPort. We’re agnostic about how the market wants to trade, whether that’s privately negotiated or through trades or on the screen. We just want our tools to be there regardless of how people choose to execute.”

“We have also seen DAP NOLA grow by a pretty significant amount. Granted, it was a small base, but we were at just below 9,000 contracts of volume in 2025 and we are at almost 24,000 contracts this year over the same January-May period.”

Managing risk in a volatile and supply constrained market

Would you say fertilizer futures contracts now have a more important role than ever – especially given the current conflict in the Middle East and the resulting disruption to the supply of fertilizers and fertilizer raw materials?

“Price transparency and price risk management are always important but get more visibility and become even more important when we see these periods of volatility, especially supply and demand volatility. Back in 2022 there were supply shocks, increased natural gas prices and some fertilizer plant closures. Now it’s the Strait of Hormuz that’s closed, and so many top producers rely on that for logistics.

“So, when there’s either geopolitical or supply and demand volatility, price transparency and risk management mechanisms become even more crucial. We’re seeing rising fertilizer and input costs in the US, but agricultural commodity prices aren’t changing all that much. It will definitely be interesting to see if there’s a shift away from nitrogen use or nitrogen-intensive crops.

“A really important point is that the reopening of the Strait of Hormuz is not an instantaneous shift back to ‘normalcy’. There are backlogs and it will take longer no matter what, because even if the blockade ends, it shifts global dynamics for a longer period than expected.

“China plays a big part and high natural gas costs are still playing a big part in market pricing and volatility. All of those combined mean there are probably more eyes on the fertilizer price, and therefore it’s even more crucial to have a vessel for risk management.

“We’ve had a lot of inbound questions and attention on our 10-Ton Urea US Gulf contract, because US grain producers are keen to find a way to manage that key input risk, especially as grain prices aren’t necessarily rising to cover those costs.”

Summing up

“We offer a diverse portfolio of fertilizer risk management tools and have expanded into this 10-Ton option on the Urea US Gulf contract. So we are responsive to customer needs and what kind of contracts they’re looking for, whether that’s new fertilizer products or new fertilizer geographies.

“We provide a diverse set of tools for producers, wholesale distributors, farmers, anyone along the supply chain, to manage risk. In periods where we see heightened volatility – whether that’s due to geopolitical factors, supply shocks or shifts in demand – the ability to hedge that risk and exposure becomes vitally important. We’re the place that provides the industry with the tools to do that.

“As for growth and where I potentially see the future of this market, I think education of our domestic growers is crucial. They might participate in our corn, soybean and wheat markets, but their awareness that we have this tool to manage fertilizers, one of their biggest input costs, is something we are focused on. We would love to get the message across that we’re the place that you can come to manage that input cost risk.

“I think that there’s a lot of US market growth potential. Historically, grain producers have not had access to the existing fertilizer futures contracts because they come in barge-size increments and are privately negotiated trades where you have to be an eligible participant. Agricultural producers are a large segment that needed a risk management tool for their inputs – and now they have one with our 10-Ton Urea US Gulf Contract!”

Note

This interview took place on 8th June and reflects market conditions at that time.