Fertilizer International 533 Jul-Aug 2026

8 July 2026

Market Insight

Market Insight

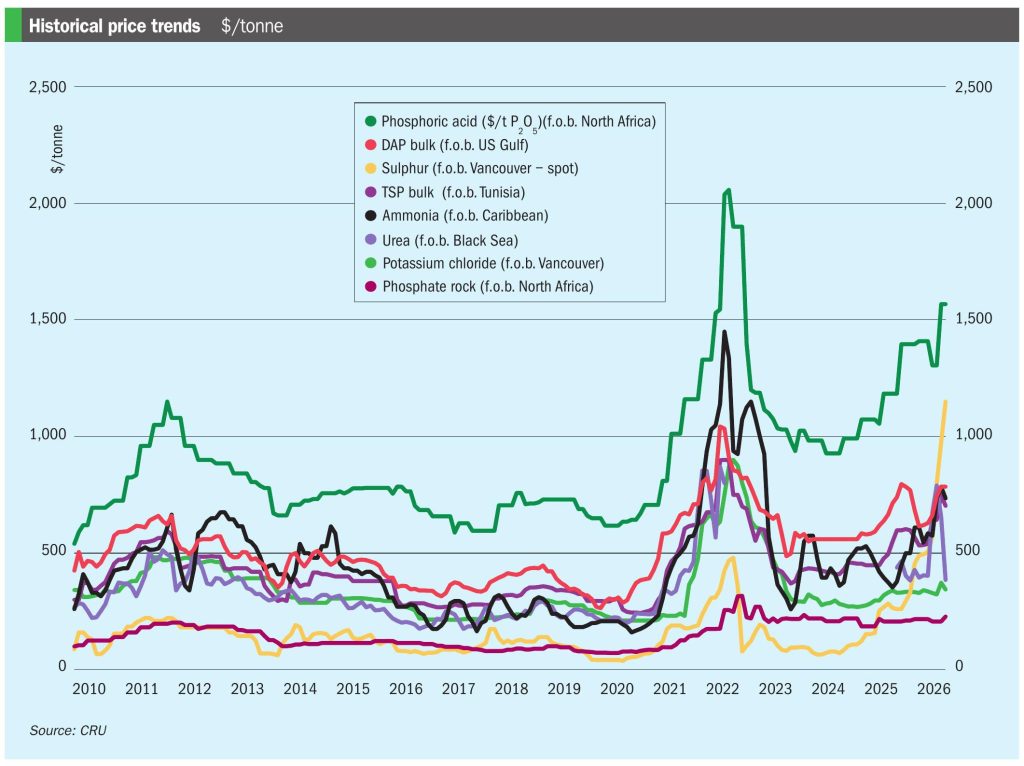

PRICE TRENDS

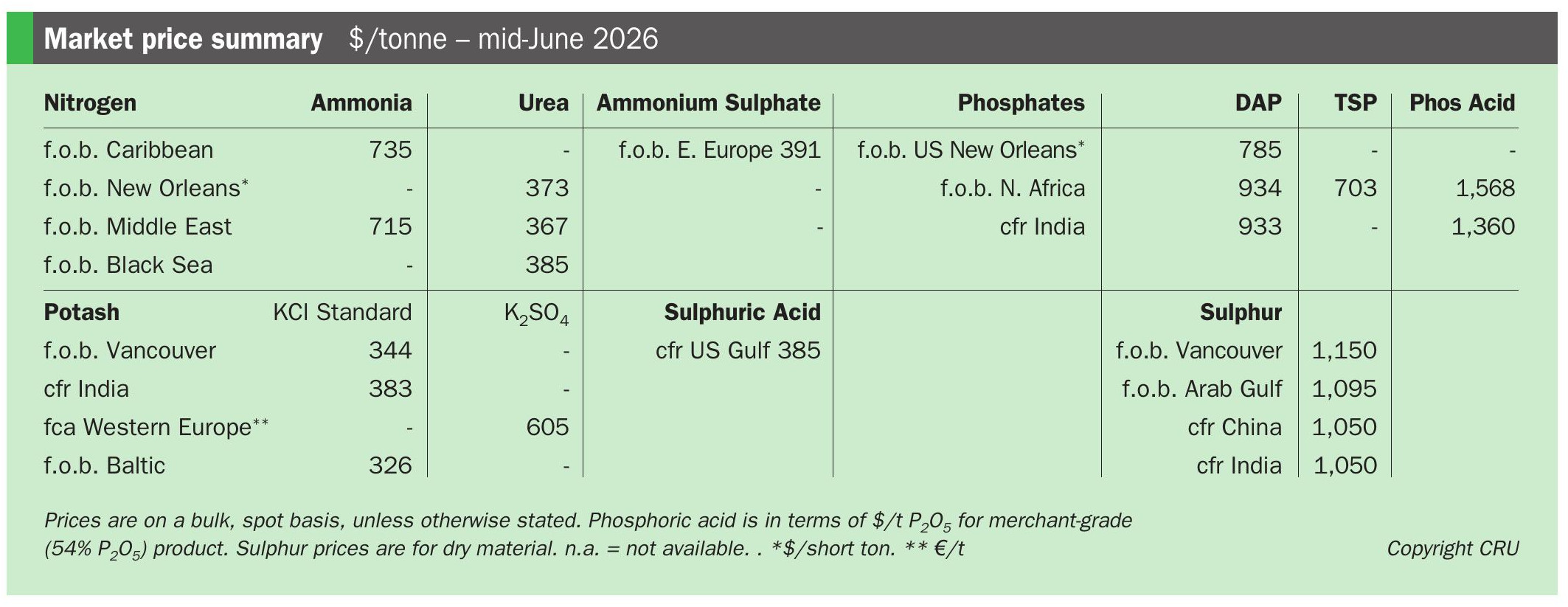

Market snapshot, 18th June 2026

Urea softens as India concludes tender and peace prevails: Global urea prices retreated further as the market digested two major developments: the conclusion of India’s latest tender and a major diplomatic breakthrough between the US and Iran. The 17th June agreement to end hostilities, if it holds, is expected to lead to the gradual normalisation of Middle East supply in the weeks to come.

In India, National Fertilizers Limited (NFL) issued letters of intent for 1.7 million tonnes of urea, following its 8th June tender. The final volume was secured on the lowest offer prices of $444.90/t cfr east coast and $449.30/t cfr west coast.

In the Middle East, a sale by Sabic was reported at $500/t f.o.b for July shipment from the Red Sea port of Yanbu. Omani offers were heard in the $410s/t f.o.b. range. In Iran, the official price was cut to $375/t f.o.b., with Shiraz selling 22,000 tonnes of prilled urea at this price for shipment from Bandar Abbas.

In Southeast Asia, a Petronas sale to Latin America at $480/t f.o.b. highlighted the sharp price correction from its last business of $790/t f.o.b. in early May. In Australia, Canberra secured three further urea shipments totalling approximately 98,500 tonnes, although access to Middle Eastern supply – which normally accounts for around two thirds of Australian urea imports – could soon be back on the agenda.

Prices west of Suez have softened. Egyptian producers continue to seek prices of $500/t f.o.b. or more, despite the lack of interest from Europe and elsewhere at these price levels. The Americas saw sharp declines. In Brazil, a sale of 40,000 tonnes was reported into Aratu at a new low of $400/t cfr. The NOLA market also hit a 17-month low, with a July barge trading at $340/st. In the US Midwest, prices fell for the ninth consecutive week. European markets have also seen prices fall significantly. In the Baltic, indications moved as low as $365/t f.o.b., while prices in France dropped to the €520-530/t fca range. UK prices for farm delivery were cited as low as £495/t.

Ammonia markets soften as bearish signals build: Ammonia prices fell across most regions in mid-June. Returning Southeast Asian supply, sharply lower Chinese export offers and the signing of the US-Iran deal on 17th June all weighed on sentiment.

In India, price indications eased to around $800/t cfr as multiple bearish factors converged. Chinese f.o.b. offers were heard in the low $600s/t. Maaden’s Searambler vessel, which has been stranded in the Gulf since March, is now due at Vizag by 25th June. This would be the first Saudi cargo to exit the Strait since the conflict began, should it complete the journey as scheduled.

East Asian spot values moved lower, with Taiwan, China offers for July heard at $770/t cfr, down from the $830-850/t cfr range of recent weeks. Southeast Asian offers also corrected lower to $730-750/t f.o.b.

Northwest Europe was quiet with thin liquidity. EU January-April ammonia imports fell 30% year-on-year (y-o-y), with Algeria remaining the bloc’s largest ammonia supplier – despite a 13% y-o-y decline – while US import volumes dropped 39% y-o-y, with CBAM costs likely to have redirected flows.

Lower phosphate production prompted a 17% y-o-y decline in Morocco’s January-April ammonia imports. The US remained the country’s largest ammonia supplier, accounting for 46% of total imports over this four-month period.

Pressure builds for phosphates price falls: Buyers continue to push for price decreases, despite the exceptionally tight supply outlook and historically high raw material prices.

In the US, DAP and MAP prices fell further, both for NOLA barges and for Midwest business. The Brazil MAP assessment was steady for the ninth consecutive week at $900/t cfr, although pressure was building for decreases. India’s spot DAP assessment was also steady for the seventh consecutive week at $930-935/t cfr. The Pakistan DAP assessment, meanwhile, tumbled from the $960s/t cfr to the $920s/t cfr.

Phosphate affordability remains a major concern, with many players across the globe waiting in hope that supply improves and prices decline, although the clock is ticking for buyers to secure cargoes within the next couple of months.

Potash prices fall back in Brazil as buying interest wanes: Potash prices in Brazil eased amid thin trade. Buyers are well covered and in no rush to return, having already met their requirements during the peak season. Suppliers, nonetheless, remain bullish, expecting prices to rise into August–September.

US NOLA prices have remained broadly stable. In Europe, expectations are building for prices to increase on tight supply during the third quarter.

Potash imports into southeast Asia are down 21% in the year-to-date. While affordability is good, buying sentiment remains cautious. China, in contrast, continues to import heavily. Its potash imports are up 7.8 million tonnes in the year-to-date, an increase of roughly 30% y-o-y.

Sulphur market holds its breath as US-Iran deal offers hope: The US-Iran deal has injected cautious optimism into a market desperate for supply, but has also brought spot activity to a near standstill. While the market remains sceptical about whether the deal will hold, buyers are unwilling to commit to current record-high prices, if a wave of previously stranded Middle Eastern supply is on the horizon.

The release of the 590,801 tonne backlog of sulphur currently stranded in the Strait of Hormuz will be critical for a market that has seen prices soar to record highs. While some vessels have begun to navigate the strait, a full return to normal is far from guaranteed.

Reported Ukrainian drone strikes on a Russian oil refinery, on top of the Kazakh rail transit ban, could tighten Russia’s sulphur balance, while leaving Kazakh export volumes largely stranded.

The disruptions have solidified North America’s role as a critical alternative supplier, with buyers turning to the region to diversify their sources. This has pushed prices in both Vancouver and the US Gulf to $1,100-1,200/t f.o.b.

Sulphur’s supply-driven price surge is now creating significant demand destruction in key markets. In Brazil, where prices have climbed to $1,100-1,250/t cfr, affordability has hit a crisis point. Buyer resistance is visible in import data: Brazil’s sulphur imports for the year to date are at a 17-year low while India’s are down 26%.

OUTLOOK

Uncertainty over where urea prices will land: The market is now wondering just how much further prices can slide before a floor is reached, with little in the way of demand-side support currently.

Ammonia tracks downwards: Ammonia prices are expected to continue easing as the market adjusts to returning supply, softer demand and the prospect of Middle East tonnes re-entering trade.

Phosphate prices to climb further: While phosphates prices may remain relatively stable for the next few weeks – as buyers hold back – they are expected to climb further over the coming months on exceptionally tight finished product and raw material availability. Poor affordability, however, remains a key factor limiting the price upside.

Potash to move higher: MOP prices are expected to rise in the near term due to tight supply. Suppliers remain sold out until August, while demand remains robust in some regions.

Sulphur market in a holding pattern: Short-term price direction is currently entirely dependent on tangible developments in the Middle East. Price movement now hinges less on underlying demand and more on whether the US-Iran deal holds. This will either force buyers back into a tight market or exert downward pressure on prices as stranded supply is released.