Sulphur 425 Jul-Aug 2026

14 July 2026

Market Outlook

Market Outlook

SULPHUR

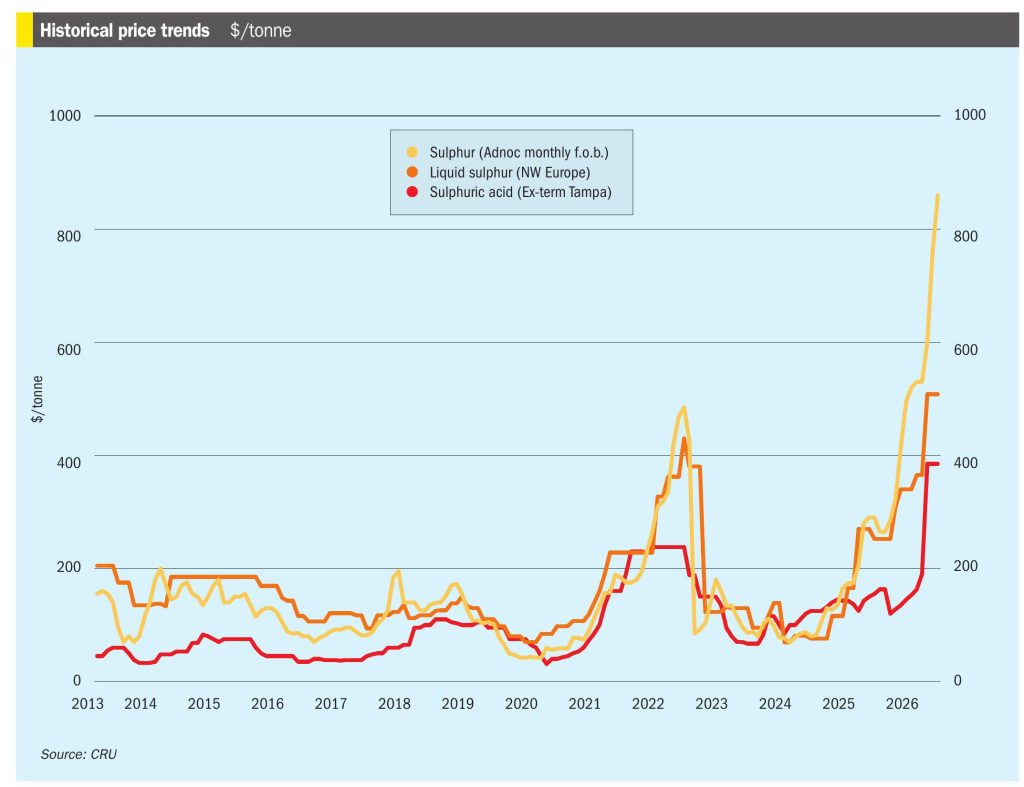

• The market has paused as bearish buyer sentiment has not yet translated into lower spot prices. The direction of the next major deal is now the critical test. This will either initiate a downward price correction, validating buyer caution, or force a recognition of the market’s underlying tightness and bring purchasers back to the table at current levels.

• While a sustained reopening of the strait points to a downward price correction, a price collapse is seen as unlikely. The backlogged cargoes are understood to be contracted or pre-sold tonnes. The release of the vessel will ease immediate spot pressure, but several factors are expected to cushion the price drop. Logistical hurdles, including vessel availability and high insurance costs, will likely mean a gradual return to normal shipping flows.

• Market fundamentals are also significantly tighter than during the last price peak and crash in 2008, with the market in a supply deficit even before the recent disruptions. Therefore, the consensus is for a slow, controlled price descent rather than a sharp crash

SULPHURIC ACID

• Weak demand has stalled further price increases, countering the upward pressure from tight supply caused by the Chinese export ban. The key factor to watch is the upstream sulphur market; any easing in feedstock costs could give buyers leverage to negotiate lower acid prices. While this quiet period is expected to continue, underlying supply tightness will support prices when significant buying volume returns.

• The official Chinese ban on sulphuric acid exports is effective from May through to the end of 2026. The decision removes a significant volume from the seaborne market and will force key importing regions to compete for alternative sources for the remainder of the year, supporting firm global prices.

• While some buyer resistance has been noted from the key Chilean market in recent weeks, the strong outcome of the PPC tender indicates that underlying demand remains robust enough to support current price levels. The eventual return of major buyers, particularly from Chile, who will need to secure volumes for the fourth quarter, is expected in July or August, and will test the current price stability. It is now widely understood that a Chilean copper producer and a Chinese smelter have finalised an agreement under which 100,000 t of acid will be supplied to the miner. The conclusion of this deal is expected to significantly reduce spot market pressure for one of Chile’s largest acid consumers heading into Q4.