Sulphur 425 Jul-Aug 2026

14 July 2026

Nickel markets

The nickel market has seen quite a turnaround in the first half of 2026, from what had been a relatively loose market with surplus supply moving towards balance and even, in parts of the market, into outright tightness. The reason has been a combination of supply disruption in Indonesia, tighter sulphur availability, higher ore costs, and a more supportive backdrop for stainless steel and battery demand than many had expected at the start of the year.

In its June market outlook, CRU described 2026 as a rebalancing year, with global nickel supply forecast to fall by 1.5% year on year, the first annual decline since 2015. The market has also become more volatile, as prices rallied sharply in May to a two-year high before falling back in June on a stronger US dollar, profit-taking, and renewed concern about Indonesian supply policy. Indonesia remains the decisive factor. Policy decisions on the RKAB quota, ore pricing, downstream investment, and export restrictions are now more important than the usual cyclical signals. At the same time, demand is no longer the weak link it was during periods of slower growth. Stainless steel production is recovering, battery-related nickel demand is rebounding, and even though the energy transition is evolving in ways that may eventually reduce nickel intensity, the metal still has a strong role in the next few years.

Supply

Supply has seen structural change, due to a combination of Indonesian government policy and sulphur supply disruption. The most important policy move has been the reduction in Indonesia’s 2026 nickel ore mining quota, or RKAB, to 260–270 million tonnes from 379 million tonnes in 2025. That is a major cut and, by design, it is intended to prevent the oversupply that had built up in previous years.

This quota reduction has already had visible consequences. Weda Bay was placed under care and maintenance at the end of May after exhausting its allocation, which is an important signal that the quota is not just a paper measure but is affecting physical production. CRU also notes that lower ore availability, higher ore prices, and the new HPM pricing formula have all tightened the economics of Indonesian nickel production. The result is that growth in Indonesian supply was expected to stall in 2026, even before considering other disruptions.

Sulphur is the second major supply constraint. HPAL operations need sulphur, and the disruption to sulphur supply from the Middle East conflict has raised costs and reduced availability. That has been especially painful for MHP and HPAL producers because it has affected the economics of converting nickel into higher-value intermediate products. CRU expects sulphur availability to improve only gradually, with pressure easing through Q3 and more meaningfully by year-end. In the meantime, producers face a cost squeeze. Some operations can continue by stockpiling or using alternatives such as gypsum or pyrite, but these are more expensive and can only partially offset the problem.

There has also been a shift in the product mix. Indonesian nickel pig iron (NPI) output has declined, but some of that has been offset by higher matte production, especially at operations where it is more profitable than NPI. This means that while class 2 supply has tightened, the system is not collapsing; rather, it is being reallocated toward the products that currently offer better margins.

Outside Indonesia, supply is still not robust enough to compensate. Disruptions elsewhere, including Madagascar and Cuba, have added to the global supply decline. Nevertheless, Indonesia remains the main driver. If the government continues to restrain ore supply, the market should remain much tighter than in recent years. If, however, quotas are loosened or enforcement becomes less strict, the supply picture could change quickly.

Looking further ahead, CRU expects global supply to grow again over the forecast period, but the base case assumes that Indonesia will continue using policy to prevent another supply surge. That is important because it suggests the current tightness is not necessarily a one-off. Instead, it may mark the start of a more managed nickel supply regime.

Demand

Demand is firmer than many market participants may have assumed earlier in the year. The most important demand sector remains stainless steel, which continues to be the largest consumer of nickel globally. CRU has revised upwards its 2026 demand outlook, with global nickel demand expected to rise by a little over 6% year on year, with stainless steel the main contributor to that growth, both in absolute tonnage and in terms of incremental demand share over the medium term. China and Indonesia are both seeing stronger stainless output, while Europe and the US are being influenced by regulatory and trade measures. In the US, Section 232 has supported domestic stainless production by restricting imports and encouraging local output. In Europe, CBAM and tighter safeguarding measures are lowering import penetration and supporting regional stainless production. These measures do not just alter trade flows; they also underpin nickel demand by encouraging more stainless output in regions that consume nickel-containing grades. China’s industrial strategy is also supporting nickel consumption through the “new productive forces” agenda, which prioritises advanced manufacturing, electrification, digital infrastructure, and high-tech industry.

Battery demand is the second major growth area. Nickel demand from batteries is forecast to grow by 12% year on year in 2026 to around 560,000 t/a; a meaningful rebound after several years of weaker growth. The short-term driver is Chinese pCAM production, along with strong European EV demand. Even where battery chemistry is shifting toward LFP, nickel remains important in high-performance applications, especially for vehicles where energy density and fast charging still matter. However, LFP continues to take share, and that will reduce nickel use intensity over time. However, nickel will not disappear from the battery sector, but rather become less dominant in mass-market chemistries while retaining a role in higher-performance segments.

Other uses of nickel also contribute. Superalloys, aerospace, defence, and refinery catalysts provide smaller but still relevant demand support.

Trade

Policy decisions continue to reshape trade flows. As noted above, in Europe, CBAM is already affecting imports of ferronickel and related products. EU ferronickel imports were down sharply in Q1 2026, with consumers having stocked up in advance during Q4 2025. Likewise in the US, import restrictions under Section 232 support domestic stainless production, but they also influence the origin and pricing of imported nickel units. As with Europe, this does not eliminate imports; it changes where they come from and how competitive they are relative to domestic supply.

China has continued to import nickel at volumes exceeding domestic demand, suggesting that China is acting as a buffer market, absorbing surplus class 1 units even as domestic consumption patterns evolve. Indonesia’s trade position is equally significant. The country is trying to move further down the value chain, expanding sulphate, precursor, and cathode capacity. That means not just exporting ore or intermediate nickel products, but increasingly capturing more value domestically. In the short term, however, the tightening of ore supply and the high cost of sulphur make that expansion more complicated. Nickel and nickel product flows are also increasingly being shaped by strategic stockpiling.

Prices

Price action in June and early July reflects the market’s new volatility. The LME 3M nickel price had rallied strongly in May, touching a two-year high of about $19,675/t, before falling back below $16,500/t in June and then rising to nearer $18,000/t. The decline was driven by a stronger US dollar, concerns about a broader commodity sell-off, profit-taking, and renewed speculation that Indonesian supply might increase if RKAB rules were relaxed. CRU’s base case remains constructive, with prices averaging above $18,000/t over the forecast period. That view is underpinned by the higher cost base, the tighter supply environment, and the expectation that Indonesia will continue to prevent a return to oversupply.

Cost support has clearly risen. Higher ore prices, the revised ore formula, and expensive sulphur have pushed breakeven levels higher for many producers. The conversion cost support level for NPI to sulphate or cathode has moved up from around $15,000– 16,000/t to $17,000–18,000/t. HPAL operations that pay market prices for feedstock are also under more pressure, with breakeven levels above $15,000/t. This creates a firmer floor under the market. Even if demand were to soften, prices now have to clear a higher production-cost threshold.

Conclusion

Nickel supply is being deliberately restrained, especially in Indonesia, while demand remains healthy across stainless steel and batteries. That has removed the large surplus that previously weighed on the market and replaced it with a much tighter balance. Prices reacted strongly to this change, even if short-term macro factors caused a pullback in June.

Looking ahead, the main question is whether Indonesia continues to manage supply tightly enough to keep the market balanced. If it does, nickel should remain well supported, with a price floor shaped by higher ore and sulphur costs. If policy eases, the market could quickly shift back toward surplus. For now, the base case is a finely balanced market, supported by resilient demand and constrained supply, but vulnerable to volatility from policy surprises, the US dollar, and geopolitical developments.

CRU LAUNCHES INDONESIA ACID PRICE

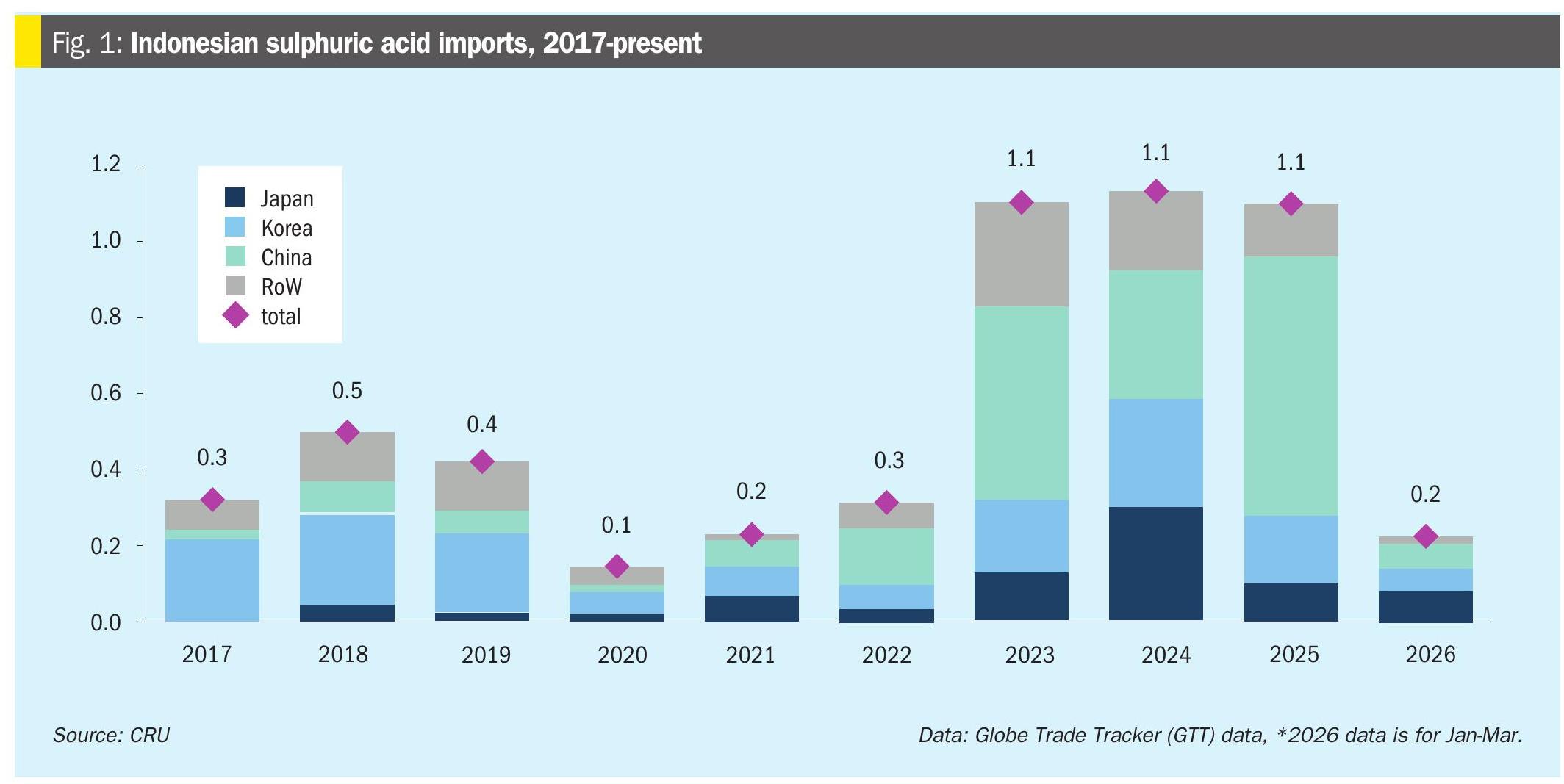

As Indonesia’s nickel industry drives significant import demand of sulphuric acid in recent years, CRU has launched a new weekly c.fr Indonesia acid price assessment to bring transparency to this key spot market.

Over the past five years, Indonesia has emerged as a key player in the sulphuric acid market, driven primarily by the rapid expansion of its nickel industry. Growing interest in the battery materials sector has triggered a wave of high-pressure acid leach (HPAL) projects, with Indonesia at the centre of these additions. As a result, nickel-related acid demand has surged to 16 million t/a in 2025 from 3.5 million t/a in 2021. Alongside this rapid growth in demand, domestic acid production has also increased, supported by a combination of integrated acid units at nickel operations and new smelter capacity. Sulphur-burnt acid is the main source of acid in Indonesia amid the increased sulphur burning capacity in the country. However, despite rising local output, Indonesia’s acid requirements have outpaced supply. While sulphur imports meet most demand, faster-than-expected expansion of HPAL capacity has driven a sharp rise in acid import needs. Acid import volumes have increased steadily, reaching 1.million t/a in 2025, equivalent to a 47% CAGR since 2021.

The supply mix for these imports has also evolved. The market saw a pivotal shift in 2023 when total import volumes surged by over 250% year-on-year, jumping from around 310,000 t/a in 2022 to nearly 1.1 million t/a. This initial demand was primarily met by increased flows from Japan and South Korea. However, China emerged as the single largest supplier in 2025, shipping over 670,000 t. This trend has continued into the current year; for the first quarter of 2026, Indonesia imported 220,652 t, sourced almost evenly from its three main partners: Japan (77,259 t), South Korea (67,949 t), and China (67,642 t).

This new benchmark will provide essential price clarity for a market now defined by spot purchasing, and builds on CRU’s price tracking since the start of 2026, which has already captured significant market volatility. The year began with relative stability, as prices held within a $150-185/t c.fr range through the first quarter. In April, however, tighter global supply and consistent spot demand from the HPAL sector pushed prices sharply higher, reaching $380-410/t c.fr at the end of May. This represents an increase of more than 160% since January and demonstrates the market’s sensitivity to global supply shifts and the need for a consistent weekly reference.