Nickel markets

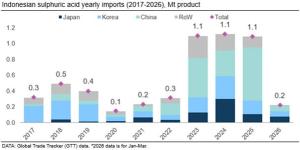

Nickel is becoming increasingly important to the sulphur and sulphuric acid markets, with Indonesia now a key importer.

Nickel is becoming increasingly important to the sulphur and sulphuric acid markets, with Indonesia now a key importer.

Nickel Industries announced started up the sulphuric acid plant at its new Excelsior Nickel Cobalt (ENC) HPAL project in the final week of June. The ENC Project is a massive, multi-billion dollar high-pressure acid leach (HPAL) facility located in the Indonesia Morowali Industrial Park (IMIP) in Central Sulawesi, Indonesia. It is operated by Australia’s Nickel Industries to supply battery-grade materials for the electric vehicle (EV) market. At capacity, it is expected to yield roughly 72,000 t/a of contained nickel equivalent as mixed hydroxide precipitate (MHP), nickel sulphate, and nickel cathode.

As Indonesia's nickel industry drives significant import demand of sulphuric acid in recent years, CRU is launching a new weekly CFR Indonesia acid price assessment on 28 May to bring transparency to this key spot market.

Several battery material nickel miners in Indonesia have reportedly trimmed output by at least 10% due to a shortage of and higher prices for sulphur caused by supply disruptions arising from war in the Middle East. Sulphuric acid is used to process nickel ore into mixed hydroxide precipitate (MHP), a feedstock used in electric vehicle (EV) batteries.

Pertamina New & Renewable Energy (NRE) has signed a memorandum of understanding (MoU) with CRecTech to explore the development of a pilot biogas-to-biomethanol facility.

Three leading regional fertilizer producers have established the Southeast Asia Fertilizer Association (SEAFA).

Four Chinese-operated nickel plants at the Indonesian Morowali Industrial Park have temporarily ceased operations following a fatal landslide in February, in a development that will significantly reduce regional demand for sulphur and sulphuric acid. The shutdowns affect facilities run by China’s GEM Co. and its partners, which together account for 30% of Indonesia’s high-pressure acid leaching (HPAL) capacity. The move comes amid heightened regulatory scrutiny. The largest of the four plants, PT QMB New Energy Materials, could remain offline for up to three months.

PT Pupuk Kalimantan Timur (Pupuk Kaltim) says that it has begun work on a revamp to its number 2 ammonia plant. The plant, which was originally constructed in 1984, has a capacity of around 1,500 t/d of ammonia. The revamp, which is being carried out internally by Pupuk Kaltim, aims to improve energy efficiency at the ageing plant and reduce carbon emissions, according to the company. The revamp is expected to extend the plant’s operational life, improve production reliability, and support Indonesia’s long-term fertilizer supply amid rising domestic demand.

Australia’s Nickel Industries is to sell a 10% share of the Excelsior Nickel Cobalt high-pressure acid leach (HPAL) project in Indonesia to South Korea’s Sphere Corp. The $240 million price tag represents a $2.4 billion valuation for the company. Sphere will acquire the stake from Hong Kong-based Decent Resource, while Nickel Industries will retain its 44% stake in the project, according to Nickel Industries.

PT Vale Indonesia Tbk says it has officially received the first two autoclave units for the Pomalaa high-pressure acid leaching (HPAL) project, a key component of the Indonesia Growth Project (IGP) Pomalaa. This delivery marks a critical milestone in preparing Indonesia’s high-tech nickel processing facility for operation. The welcoming ceremony was attended by PT Vale and PT Kolaka Nickel Industry (KNI) management, along with strategic project partners including Indonesia Pomalaa Industrial Park (IPIP), Huayou Southern Construction Command, MCC20, and other stakeholders.