Syngas from biomass gasification

For many years confined to pilot projects and feasibility studies, biomass based gasification is seeing rapid take up in China for methanol production and may mark a new era in syngas generation.

For many years confined to pilot projects and feasibility studies, biomass based gasification is seeing rapid take up in China for methanol production and may mark a new era in syngas generation.

A market already characterised by tight supply has been thrown into chaos by the Iran war and reduction of phosphate exports from the Gulf at the knock on effect on sulphur prices, a key input into MAP/DAP production.

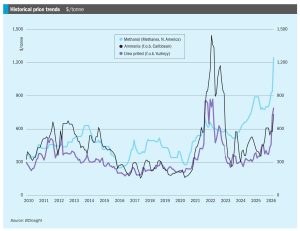

The start of May saw urea prices start to decline from the yearly highs seen in mid-April, as buyers from India, the US, and Europe stayed away from the markets. India is not expected to return with another tender before late May or early June at the earliest, after booking 2.5 million tonnes for shipment through mid-June, covering immediate requirements, and with domestic production having improved and stocks at a healthy level of over 7 million tonnes. In the US, earlier concerns over May shipments have eased, with net import figures not as low as initially feared, and even some re-export of cargoes to Latin America where higher prices can be earned. With the potential for China to return to export sales towards the end of May and start of June, there was at least a hope that the worst of the current price spike may be over.

• Short-term outlook: Ammonia benchmarks are expected to remain under upward pressure. The PAU turnaround removes a key supply source from an already tight SE Asian market.

Global ammonia benchmarks pushed to fresh highs in April, with a reported trade from Egypt to NW Europe at $905/t c.fr, marking the highest Atlantic level seen since the Middle East conflict began. The move was driven primarily by tightening North African supply, with Algerian offer levels climbing to $840-850/t f.o.b., and Egyptian availability constrained by EBIC being sold out through June, together with limited prompt tonnage from Abu Qir.

The effective closure of the Straits of Hormuz by Iran in the wake of US and Israeli attacks has sent shockwaves through all markets, but sulphur has been particularly badly affected. While the Straits carry 22% of global phosphate exports and 35% of urea, for sulphur around 45% of the 39 million tonnes transported internationally every year must traverse the narrow waterway, with major suppliers like Abu Dhabi and Saudi Arabia relying upon it for their export cargoes.

The US and Israel attacks on Iran and the Iranian response have thrown commodity markets into chaos, with sulphur and sulphuric acid particularly affected.

With the decline of Venezuela’s production, Canada’s oil sands now represent 90% of all oil sands output, and a significant share of North America’s sulphur production.

• Market sentiment has shifted decisively from bearish to bullish as the conflict in the Middle East has triggers a significant price rally.

Conflict in the Middle East has halted all vessel traffic through the Strait of Hormuz, effectively paralysing a region that accounts for 48% of global seaborne sulphur trade. As a result, the sulphur spot market has ground to a halt, with prices notionally holding unchanged in the $490-515/t f.o.b. range simply due to a lack of activity. No spot offers were reported out of the Middle East.