Nitrogen+Syngas 401 May-Jun 2026

20 May 2026

Market Outlook

Market Outlook

AMMONIA

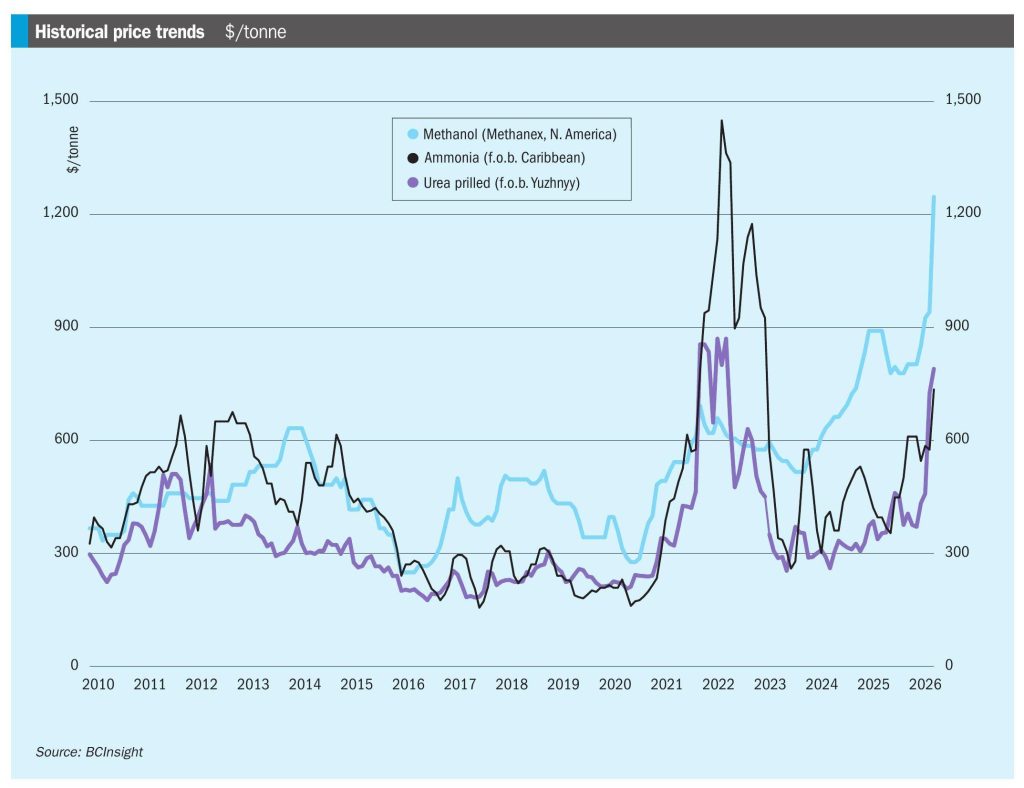

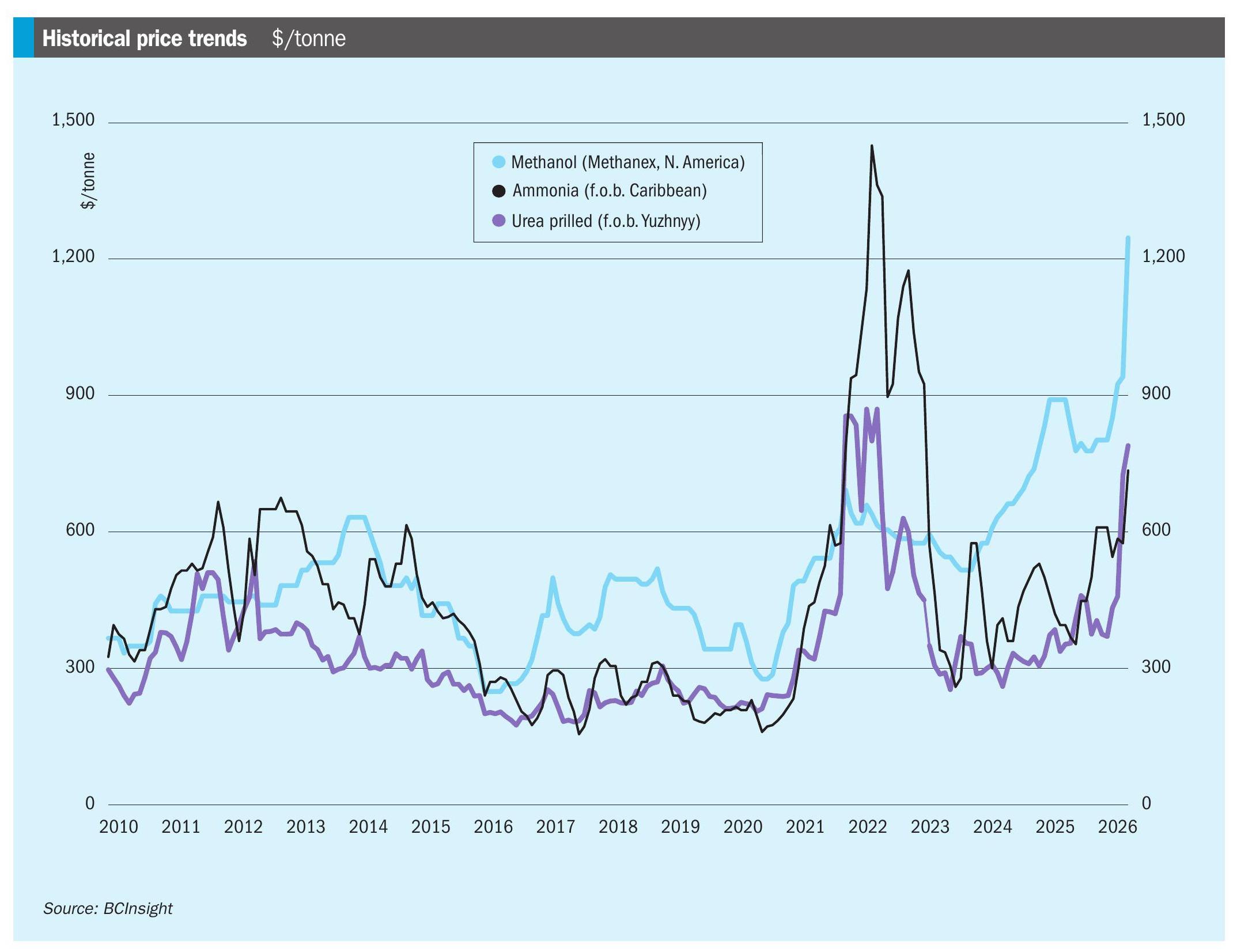

• Short-term outlook: Ammonia benchmarks are expected to remain under upward pressure. The PAU turnaround removes a key supply source from an already tight SE Asian market.

• North African availability is similarly constrained, and the Hormuz closure continues with no clear resolution timeline. War risk insurance shows no signs of normalising, and vessel operators remain unwilling to commit to Gulf transits under current conditions.

• In the US, strong domestic spring demand is competing with demand from Northwest European buyers, who are continuing to buy even though the spring application season is drawing to a close.

• China’s export suspension remains unconfirmed, with sources indicating the policy has not been formally implemented. Q1 export data showed 207,000 tonnes shipped in 1Q 2026, a 645% year-on-year surge, underlining how consequential any formal ban would be for regional markets.

UREA

• Short-term outlook: Prices should remain supported for as long as the Strait of Hormuz remains closed.

• It remains unlikely that China will participate in India’s tender, with Beijing still to release new quota allocations for exports. CRU expects exports to be released from May, though the exact timeframe is unclear.

• India is set to mop up a huge proportion of global supply through mid-June and with the question of availability from the Middle East still wholly unclear, the potential supply tightness that was anticipated for US buyers may well turn out to be the case. The US likely still needs to secure around 600,000 tonnes for May-June, pitting it directly against India – and also Australia – for available tonnes.

METHANOL

• Methanol prices are experiencing a significant surge to multi-year highs, driven by supply disruptions in the Middle East, with 2026 prices expected to remain firm to bullish due to continued geopolitical instability and strong demand. Conflict in the Middle East has disrupted exports, particularly affecting Asia and driving up global prices. Some futures have seen a 60% price increase year on year. Methanex’s US NDRP has reached $1,480/t.

• In China, high inventory levels have created a floor on prices in some areas, but regional instability keeps them high.

• North American and European demand remains steady, driven by construction and chemical applications.

• Chinese coal-based methanol producers and North American gas-based methanol producers are seeing very beneficial margins as supply from the Arab Gulf remains constrained.