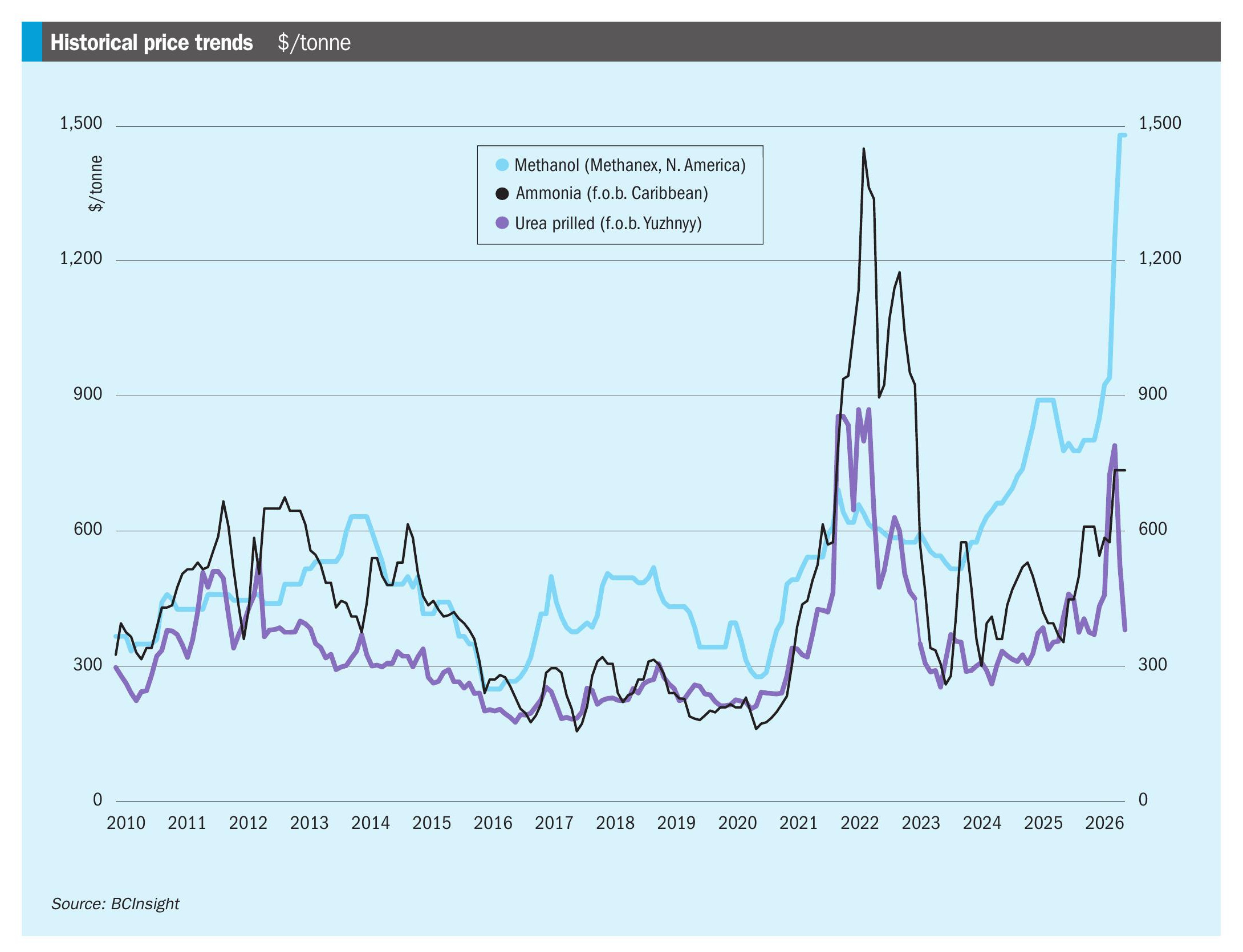

Nitrogen+Syngas 401 May-Jun 2026

20 May 2026

The market for ammonium phosphates

AMMONIUM PHOSPHATES

The market for ammonium phosphates

A market already characterised by tight supply has been thrown into chaos by the Iran war and reduction of phosphate exports from the Gulf at the knock on effect on sulphur prices, a key input into MAP/DAP production.

The ammonium phosphate market is seeing a run of high prices at present, supported by two powerful forces: tighter-than-expected global supply, and exceptionally high sulphur input costs. Mono- and diammonium phosphate (MAP/ DAP) prices had already begun to recover at the start of 2026 after easing somewhat towards the end of 2025, and that rebound is likely to become more pronounced as 2026 progresses. The main reason is not a simple cyclical upturn in demand, but rather a structural tightening of availability, especially because China is set to impose its harshest export restrictions yet. At the same time, supply from other major exporters, including OCP in Morocco and Ma’aden in Saudi Arabia, although strong and expanding, will not be sufficient to offset the loss of Chinese volumes. At the same time, however, crop prices remain relatively weak, which limits how far fertilizer prices can climb before affordability pressures restrain demand.

Regional dynamics are also shifting. India and Brazil remain major import markets, but their product preferences and sourcing patterns are changing. Brazil is moving back toward MAP after substituting into NPs and SSPs during 2025, while India continues to import heavily but from a changing supplier mix, with near-zero Chinese DAP and stronger flows from Morocco. The United States is also expected to become more active on the import side after tariffs have been lifted, even though domestic production remains under pressure.

Supply

Supply constraints are the dominant bullish factor in the market. Global phosphate fertilizer supply remains tight because China, historically one of the most important export sources, is set to constrain exports even more aggressively in 2026. China exported 129,900 tonnes of DAP/MAP during January-March 2026, representing a 17% increase from the first quarter of 2025, but since then the Chinese authorities have announced that exports of DAP, MAP, and NP will be prohibited until at least August 2026, and there are fears this may be further extended. This is a major loss to the seaborne market.

China’s previous restrictions on phosphate products have already reshaped export patterns. Rather than simply reducing total phosphate trade, the country’s controls encouraged more exports of alternative phosphate grades such as NP, SSP, and TSP. However, the latest round of restrictions is wider and more severe. Because NP is now included, the ability to compensate for weak DAP and MAP exports with other phosphate products is much reduced. This makes the overall supply outlook far tighter than in previous years, even on a P2 O5 basis.

Outside China, supply is insufficient to balance the market. OCP in Morocco had been continuing to expand export volumes, and was expected to keep breaking export records this year, particularly as it shifts toward more TSP production. However, high sulphur and acid prices have prompted the company to announce that it is bringing forward its maintenance schedule and expects a reduction of up to 30% in output for the second quarter of 2026. A potential reduction in supply from the producer is causing concern in a global market that is already exceptionally tight.

Ma’aden in Saudi Arabia has also posted strong growth and had also been expected to continue ramping up exports after successful debottlenecking, with expectations that its Phosphate III unit may come online by the end of 2026, or possibly even earlier. However, the closure of the Strait of Hormuz has halted Gulf exports from the east coast for now. Maaden is currently moving supply to Yanbu on the Red Sea coast, though this requires thousands of trucks per cargo. The producer indicated it may achieve three to four cargoes per month via this method, which would still leave export volumes well below typical norms of around 400-600,000 tonnes/month DAP/MAP.

The other knock-on effect of that closure has been the exacerbating of sulphur prices that were already high before the war in Iran. Sulphur to make sulphuric acid to produce phosphoric acid is one of the key input costs in phosphate fertilizer production, and prices have risen to extraordinary levels, above previous peaks. This has materially squeezed producer margins around the world. Russia has extended its ban on sulphur exports, contributing to tightening the market.

As well as Morocco, above, it is likely that some phosphate producers will reduce output. China’s output decisions are shaped much more by policy than by cost, but in Brazil, Mosaic has suspended SSP production at Fospar and Araxá. Those plants account for a substantial share of Mosaic’s Brazilian capacity, and their idling is likely to push Brazilian import demand higher.

The United States has seen margins deteriorate sharply, and China’s producer margins are very poor. However, because US production issues are tied partly to declining rock quality and because China’s output is governed by policy rather than pure economics, supply from these sources will likely remain tight rather than collapsing outright.

Demand

Demand is strong enough to absorb supply where available, but not so strong that it is the main driver of price formation. Instead, demand growth is heavily constrained by availability and affordability. The largest price increases had previously been expected in the Americas, especially in Brazil and the United States. In Brazil, demand is expected to recover as the market shifts back from NPs and SSPs toward MAP. This does not represent broad-based expansion in phosphate consumption so much as a product-mix reversal. Brazil had used cheaper NP and SSP grades in 2025 when they were available at favourable prices, but the report expects that this pattern will not repeat in 2026 because Chinese NP supply will be much weaker, and SSP availability will also be reduced.

The United States is another key demand story. The lifting of tariffs on DAP and MAP in October 2025 should support a surge in imports in 2026, particularly as domestic production remains weak. US phosphate sales fell significantly in late 2025, reflecting both poor affordability and weakening domestic output. Overall US import demand could rise over the year, though the US could see temporary discounts relative to international markets if demand fails to recover quickly enough.

India remains a very important demand centre. Indian imports were extremely strong in 2025, supported by government subsidy arrangements and active purchasing even though import margins were negative. However, India’s phosphate fertilizer production is rumoured to have declined 20-25% in recent months due to limited raw material supply and planned shutdowns, though official data has not been released since late February to confirm actual figures. The Fertilizer Association of India (FAI) has been unable to obtain production data from companies, raising concerns about transparency during a critical supply period. Several major producers have brought forward planned maintenance from April/May to March due to raw material supply constraints. Paradeep Phosphates Limited (PPL) commenced a month-long phased turnaround in early March, while Coromandel International Limited (CIL) planned a series of maintenance stoppages from late March through early April. IFFCO’s Paradeep operation started a month-long turnaround on 12 March, with rumours of lower production rates at its Kandla operations. Deepak Fertilizers, Greenstar, and Indorama were all understood to be carrying out maintenance in H2 March and April, according to sources. Buyers are relying on existing stocks for Q2 and show no urgency to return at current prices (>$865/t), despite the approaching Kharif season. Early April buying by some importers briefly suggested India might re-enter the market, but limited cargo availability has kept buyers sidelined.

China’s demand picture is more opaque. Despite export controls, domestic phosphate production was strong in 2025, which suggests solid internal consumption. However, much of the local pricing structure is shaped by the export policy framework rather than by true demand strength. China is less of a demand-growth story and more a policy-controlled market whose domestic consumption matters chiefly because it determines export restrictions.

Affordability is a decisive demand constraint across regions. Crop prices, especially for corn and soybeans, have remained relatively weak or only modestly improved. In Brazil and the United States, the affordability of phosphate fertilizers remains poor or at decade lows. This means that even though planted area remains supportive in some cases, buyers are sensitive to price spikes. If crop prices do not strengthen, fertilizer prices cannot rise indefinitely. So demand is present, but its elasticity and purchasing timing are both highly sensitive to price and policy.

Trade

Prior to the war in Iran, China’s reduced exports had been the main trade disruption. Chinese DAP+MAP exports will be sharply lower and NP exports, which helped support overall Chinese P2O5 trade in 2025, are also likely to weaken. This means that global buyers who previously relied on Chinese product will need to turn elsewhere. There are fears that China may even extend its export ban beyond August to the end of the year.

Brazil is one of the clearest examples of trade reallocation. In 2025, Brazilian imports shifted away from MAP toward NPs and SSPs because those cheaper alternatives were available from China. This pattern is expected to reverse in 2026, with Brazil returning toward MAP and TSP as NP availability falls. Brazilian imports of NP rose sharply in 2025, driven partly by products such as 8-40-00, a by-product of tMAP production in China, but the lack of Chinese supply will shut off this source. Brazilian TSP imports also increased, and OCP has been successful in marketing discounted TSP into the country, but may face output restrictions if disruptions continue.

India’s trade pattern has changed more dramatically on the origin side. Chinese DAP imports have all but disappeared, and India has been drawing much more from Morocco and other suppliers. India imported approximately 27,000 tonnes of DAP in March, delivered to Indian Potash Limited (IPL) at Vizag from Saudi Arabia. April arrivals show two vessels totalling 60,800 tonnes from Morocco and Jordan. DAP port stocks have dropped sharply, reflecting steady drawdowns with minimal replenishment. The thin import pipeline heading into the Kharif season confirms the severity of the supply disruption, with no alternative origins capable of replacing Middle Eastern volumes in the near term. The combination of declining port stocks, reduced production, and limited import volumes creates a precarious supply position ahead of peak Kharif demand.

Outlook uncertain

As with most markets, the key determinant of phosphate markets going forward will be how the conflict in Iran plays out. Prices were already expected to climb even higher than 2025’s peaks, given severe export restrictions in China, but the conflict in the Middle East is set to tighten the market further and push prices even higher over the coming weeks and months, with the impact on sulphur availability and prices also adding upwards pressure on phosphates.