Market Insight

Price trends and market outlook, 7th May 2026.

Price trends and market outlook, 7th May 2026.

We compare and contrast the 2025 financial performance of selected major fertilizer producers.

Sulphur production continues to expand in the Middle East and East and South Asia both from new refineries and major sour gas projects.

A review of papers presented at this year’s Sulphur World Symposium, held by The Sulphur Institute (TSI) in Vancouver, Canada this year from April 28 to 30.

CRU’s Phosphates+Potash Expoconference was held in Paris in mid-April, with the Iran crisis uppermost in everyone’s mind. Margins are under pressure, sulphur has become a strategic constraint, and the phosphates investment pipeline is thin. CRU Principal Consultant Humphrey Knight examined the fallout from the closure of the Strait of Hormuz, noting that fertilizers have been hit harder than most bulk commodities. A large share of exportable sulphur and traded urea normally originates in, or passes through, Gulf producers. The effective closure of the strait has squeezed the traded part of these markets, where international prices are set, and pushed benchmarks up sharply. The global phosphate market is structurally tight, and the combination of Chinese export policy and Middle East logistics has pushed the traded segment into a much more fragile state.

It is two months on from our previous issue, and almost none of the news has been good from sulphur and downstream markets. Only three sulphur cargoes are confirmed to have transited the Strait of Hormuz since the US and Israeli strikes on Iran began, all loaded at Ruwais, with destinations in India, Tanzania and Morocco, carrying a total of 160,000 tonnes. It is believed that a couple of Iranian vessels with a total of 75,000 tonnes may also have left covertly. But in spite of some Middle Eastern sulphur making its way to Saudi Red Sea ports or Duqm on Oman’s Indian Ocean coast, around 700,000 tonnes is still trapped on ships stranded in the Gulf, and coupled with production cuts in the region, it is estimated that over 1.2 million tonnes has so far been removed from the market.

Sour gas production is costly because hydrogen sulphide and carbon dioxide require extensive sweetening, sulphur recovery, safety, and compliance infrastructure, with sulphur sales helping offset but rarely eliminating those added costs.

• Prices are expected to hold at historically high levels as long as the Strait of Hormuz remains effectively closed. If the situation persists, further price increases are likely, which will only intensify the affordability crisis for global consumers.

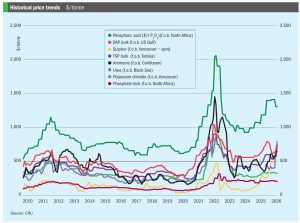

Sulphur continued to break historic records in most key international markets at the start of May as the scarcity of spot supply propelled prices higher, which triggered production cuts at some downstream markets, and increased costs in other industrial sectors. The effective blockade of the Strait of Hormuz, which halted the flow of Middle East supply, has forced desperate buyers to compete for the limited available spot cargoes, primarily from North America. Although fresh transactions were limited, export and delivered prices climbed higher, and market sentiment remained jittery. QatarEnergy hiked its sulphur price to $740/t f.o.b., a new record high for this contract since its inception in August 2013.

Nitrogen markets, and urea in particular, have been impacted by a series of geopolitical shocks in recent years which have driven markets over and above normal market factors such as feedstock and shipping costs, crop prices etc.