Sulphur 424 May-Jun 2026

21 May 2026

Market Outlook

Market Outlook

SULPHUR

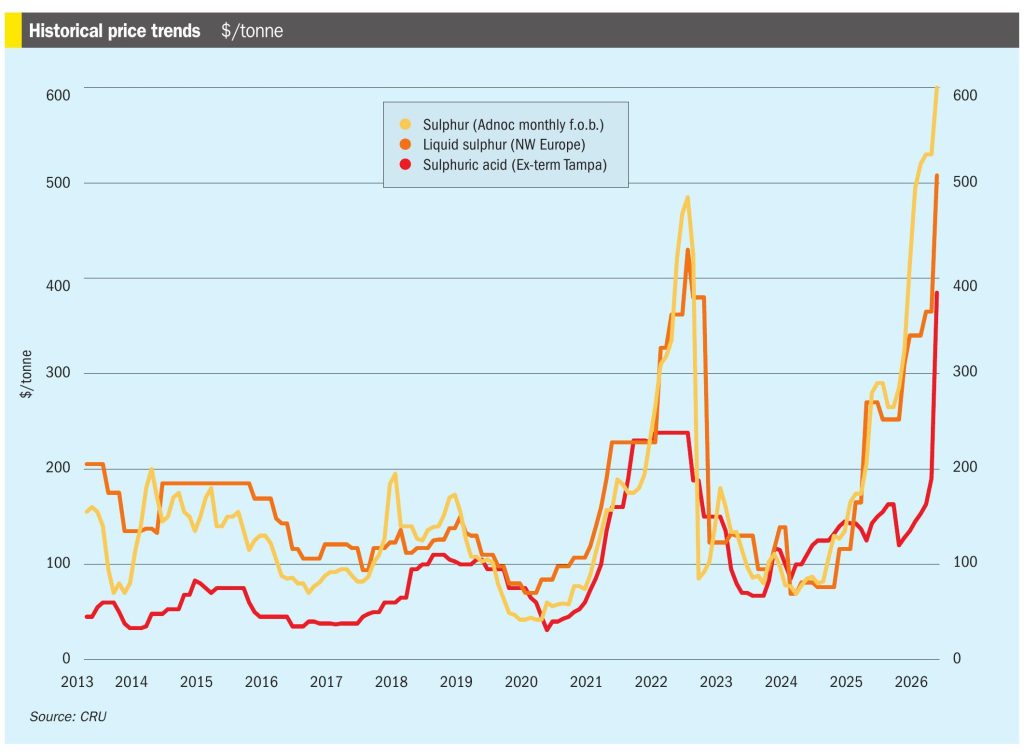

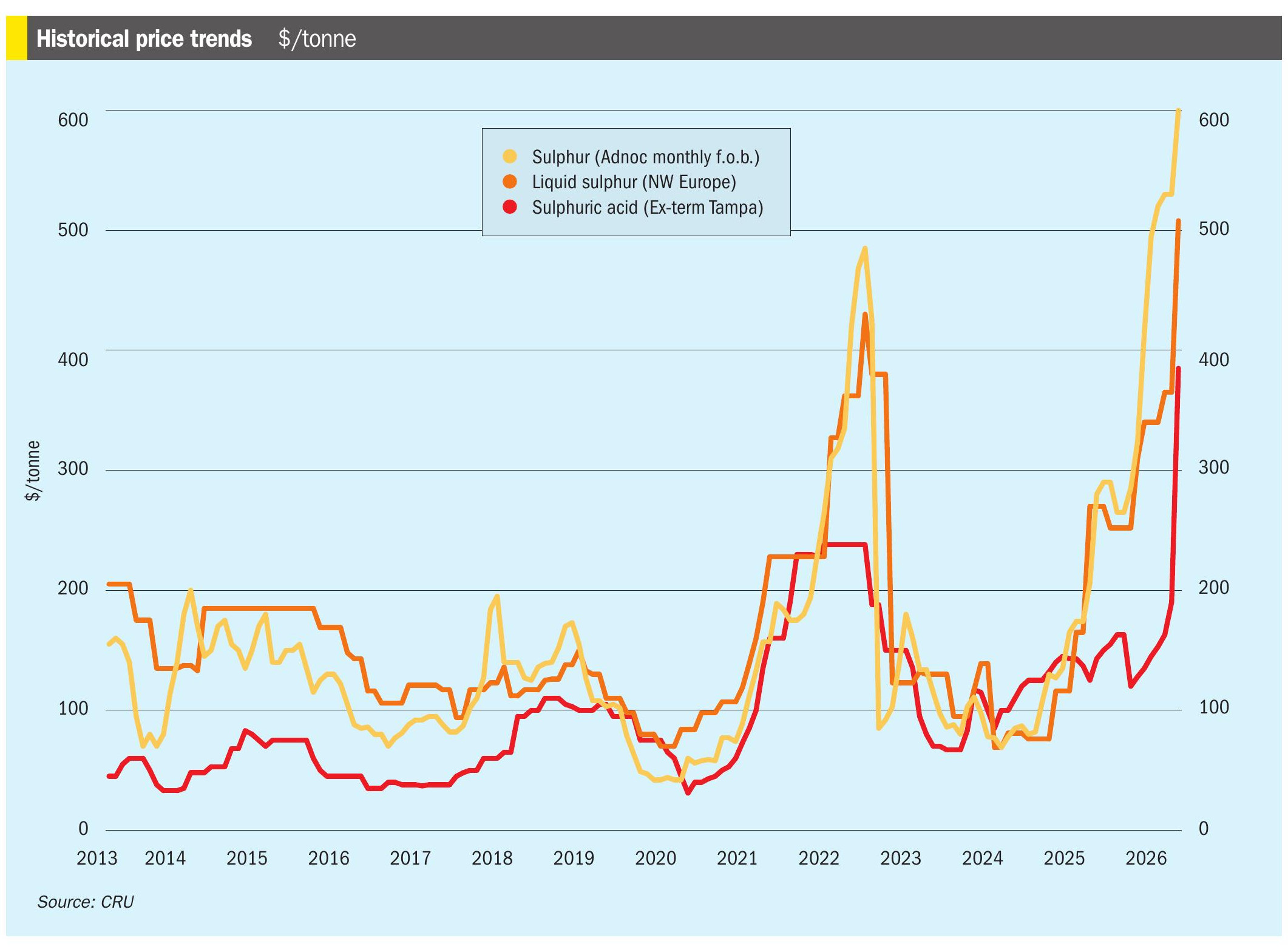

• Prices are expected to hold at historically high levels as long as the Strait of Hormuz remains effectively closed. If the situation persists, further price increases are likely, which will only intensify the affordability crisis for global consumers.

• The Middle East contract price range for sulphur sales in the second quarter of 2026 has been settled at $540-600/t f.o.b., despite major logistical turmoil stemming from the regional conflict. The ongoing hostilities have created a significant shipping backlog, with an estimated 700,000 tonnes of sulphur stranded on vessels unable to exit the Strait of Hormuz. While a significant increase, the price remains below the record high of $790/t f.o.b. seen in mid-2008. The benchmark is up by more than 130% from a year prior, when 2025 Q2 contracts were $240-250/t f.o.b.

• China is beginning to see some demand destruction. Sulphur affordability has deteriorated significantly, leaving consumers buying from ports to meet immediate requirements only. Chinese imports were already down 35% year on year in January and February, and China announced in December that its phosphate export window would remain closed until August 2026, with price caps on domestic phosphate fertilizer sales, leaving many Chinese phosphate producers operating at significant losses.

• At the recent TSI conference in Vancouver, Canadian supply was a central topic of conversation. Market players are keen to see if Canadian producers can respond to the record-high prices, but the consensus is that logistical hurdles are a major limiting factor.

• Sulphur supply may be down 3-4 million tonnes in 2026 and stock drawdowns are struggling to keep pace with supply losses.

• With no immediate resolution to the supply disruptions in the Middle East, the upward trend in sulphur prices is now expected to continue until July

SULPHURIC ACID

• Sulphuric acid prices are expected to remain historically high, supported by the fundamental lack of Chinese supply and tight availability from other regions, with the Chilean market expected to be the strongest as affordability concerns sideline some buyers.

• China’s export halt from May has redirected significant global demand towards other key exporting regions. Any spot cargoes that do become available for forward loading are expected to command prices at or above current levels. Indonesia, Chile, Saudi Arabia, Morocco and India are all exposed to some degree; in Indonesia’s case 62% of its acid came from China last year.

• Some additional exports are expected from India, Europe, Japan and South Korea, but demand destruction means that overall, the traded acid market is expected to shrink in 2026, from around 17.1 million t/a in 2025 to 13.8 million t/a in 2026