Sulphur 424 May-Jun 2026

21 May 2026

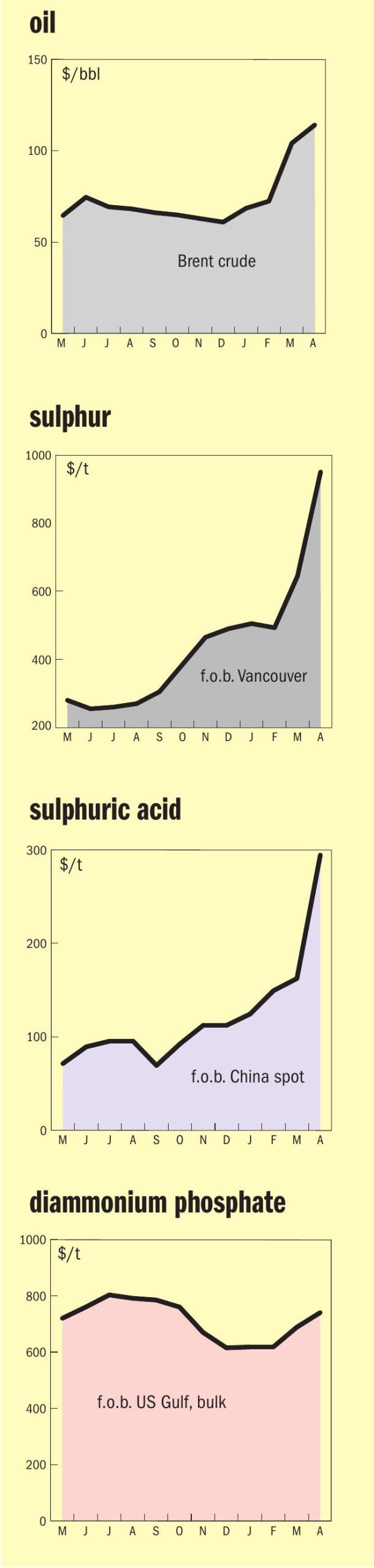

Price Trends

Price Trends

SULPHUR

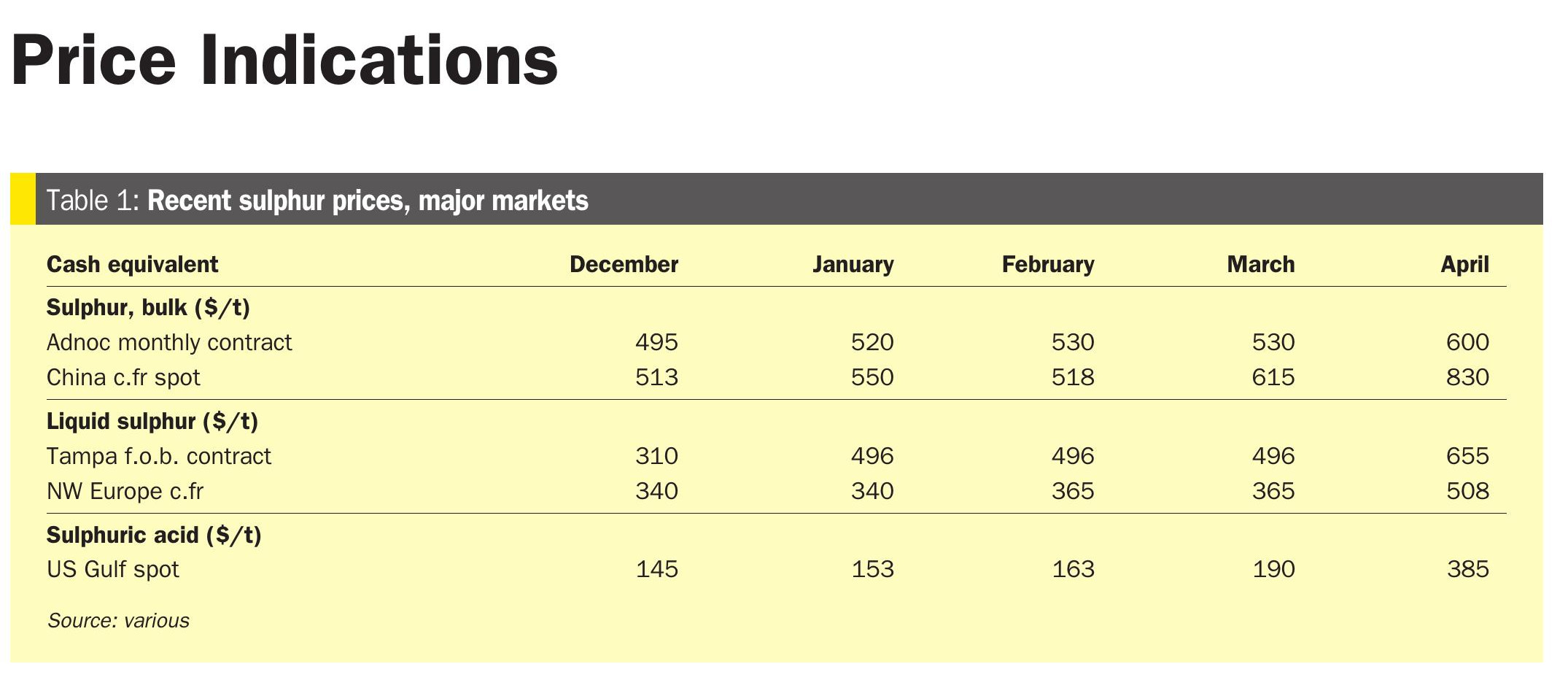

Sulphur continued to break historic records in most key international markets at the start of May as the scarcity of spot supply propelled prices higher, which triggered production cuts at some downstream markets, and increased costs in other industrial sectors. The effective blockade of the Strait of Hormuz, which halted the flow of Middle East supply, has forced desperate buyers to compete for the limited available spot cargoes, primarily from North America. Although fresh transactions were limited, export and delivered prices climbed higher, and market sentiment remained jittery. QatarEnergy hiked its sulphur price to $740/t f.o.b., a new record high for this contract since its inception in August 2013.

Brazilian prices decisively stayed above the $1,000/t c.fr mark this week and advanced to a new high of $1,000-1,100/t c.fr, which shocked the market and gave it a clear price signal. Given this price jump, market participants expect other consumer markets to follow Brazil prices higher – a trend already seen in Indonesia, India and China.

Mosaic says that it plans to reduce phosphate fertilizer output in both the US and Brazil due to high prices and limited availability of sulphur, the company said as it reported a net loss of $258 million for the first quarter of 2026 despite strong sales. Mosaic said that it is closely monitoring raw material markets, particularly sulphur, amid record-high prices and limited availability. As a result, the company has withdrawn its phosphate production guidance for 2026 as it reviews its operating plan for the rest of the year. As part of the review, Mosaic has taken initial steps to partially curtail production at Louisiana and Bartow in the US, and is also scaling back additional production in Brazil.

Sulphur prices in Indonesia hovered near the $1,000/t c.fr mark, with only deals for small volumes heard above this level. Indonesian prices are at the highest since CRU began assessments in June 2022 and were assessed at a narrower range of $970-990/t c.fr at the end of April. Elsewhere in the region, Zhejiang Huayou Cobalt said its Indonesian unit will temporarily halt part of its production lines from 1 May, cutting around half the output at its mixed hydroxide precipitate (MHP) plant on rising sulphur costs.

Indonesian sulphur imports fell 30% year on year in the first quarter of 2026, totalling 966,000 tonnes compared with nearly 1.4 million tonnes in the same period last year, according to latest data from Global Trade Tracker (GTT). However, the decline is from a record high in 2025, and this year’s Q1 volume still remains the second-highest on record, well above the 371,500 tonnes imported in the same period of 2024.

Mediterranean sulphur prices surged to new record highs in early May, with delivered prices assessed at $920-940/t c.fr. This is the highest level recorded since CRU’s assessment began in 2011. Mediterranean f.o.b. prices are seeing netbacks of around $880-900/t, another record since that benchmark started in 2017. The market has remained largely quiet as buyers and sellers adapt to the new pricing environment. Despite the quiet, underlying demand remains present, with reports that buyers in Egypt are still in the market for product. The price strength is a direct reflection of the acute tightness in the global market, which has been exacerbated by the ongoing disruptions in the Middle East.

In India, sulphur prices surged to $800–850/t c.fr, as importers looked for available supply but suppliers and traders struggled to source any cargoes to meet demand. Concerns are growing over the potential production cuts or halts from fertilizer producers in the country on the back of surging sulphur costs, NBS subsidy limitations, and ahead of the approaching Kharif season demand. Market talk suggests offers in the mid-to-high $900s/t c.fr have circulated without firm commitments, while Omani and Kazakh offers have emerged at around $830-875/t c.fr. Paradeep Phosphates Limited (PPL) received supply relief as a 55,000 tonne ADNOC cargo cleared the Strait of Hormuz and is expected at Paradip Port around 4–5 May. This marks the first significant Middle Eastern sulphur arrival in India since the conflict began, with industry viewing the development as a positive signal. Another sulphur vessel similarly cleared the strait bound for Africa. India is expected to receive approximately 20,000 tonnes of sulphur from Vancouver on the vessel TN Dawn, destined for Kakinada. IFFCO previously received two Canadian cargoes of 55,000 tonnes each in February and March, providing partial coverage. Overall, February imports totalled 144,250 tonnes, with the UAE supplying 62% and Canada the remainder. March data shows two vessels totalling over 65,000 tonnes, and April shows just one vessel of 11,600 tonnes from the UAE, delivered to Kandla on 23 April.

Many Chinese buyers dipped into port inventory stocks for supplies ahead of the Labour Day holiday after halting any purchases from the international market, prompting port prices up this week to $943-980/t, up 7% week on week. On the back of increased port prices, the delivered prices were assessed higher at $800-860/t c.fr.

The market continues to monitor the situation in the Middle East, where the successful transit of two vessels through the Strait of Hormuz, the Valsamitis (33,600 tonnes) and the Frosso K (55,000 tonnes) from Ruwais, UAE, in the past weeks has lifted sentiment. But this trickle of volume from the region versus the near 700,000 tonnes trapped behind the waterway has failed to provide much respite.

SULPHURIC ACID

Constricted global availability continues to push up sulphuric acid prices, with several benchmarks reaching new record highs at the end of April. Amid the lack of Far East supply, with China’s export ban set to start from the start of May and Japanese and Korean smelters well committed, Europe was the key outlet for fresh supply, though spot supply from there was also scarce. Spot prices for acid exports from northwest Europe climbed to $320-350/t f.o.b. from $300/t flat, with indications that the latest sales tender from Poland was awarded around the assessment high end.

On the import side, Latin America remained the key demand region driving price increases. The Chile spot assessment climbed to $450-470/t c.fr from $410-450/t, up 145% since the start of the year and representing its highest level since CRU began publishing the benchmark in December 2008. The price surge is a direct consequence of the Chinese export halt, which has left Chilean consumers exposed for their second half 2026 requirements. Chile’s need to cover its estimated 1 million tonne spot requirement for the second half of the year continues to set the ceiling for the global market. Chilean buyers are under extreme pressure, with those that have a greater acid use per tonne of copper less willing or able to accept current price levels. Still, buyers are ultimately having to pay up to secure tonnes where they can find them, and the Chilean metals sector is expected to have less issues with affordability than some other acid demand markets.

Sulphuric acid prices in Indonesia have increased further, and are indicated at $380-400/t c.fr, supported by a sale reported in the high $390s/t c.fr, reportedly to Pupuk, following a previous sale at $380/t c.fr for May delivery. Sources indicate that Gresik is likely to return to the market with a purchase tender soon. The price rise is a direct result of the confirmed halt in exports for the remainder of 2026 from China, which was a critical supplier to the Indonesian market. During the May-December period in 2025, GTT trade data shows Indonesia was the second-largest destination for Chinese acid exports, importing 476,000 tonnes. Still, a domestic headwind persists. A new mineral ore pricing mechanism, announced by Indonesia’s Ministry of Energy and Mineral Resources (ESDM) on 13 April, is set to increase ore costs for the country’s nickel processors. This may impact the ability of these key acid consumers to continue affording high-priced imported material.

Spot prices for acid to Brazil were assessed up at $420-430/t c.fr from $400-420/t, representing a new record high for the assessment, which CRU has published since 2003. The price far outstrips the long-standing 2008 record of $335/t, which was surpassed for the first time two weeks ago. The high acid prices are being met with strong resistance from local fertilizer producers. Although the need to secure tonnes is forcing deals to be done, many buyers are now facing extreme margin pressure on phosphate fertilizer products. This raises significant questions over demand destruction, as it is unclear how long the market can continue to absorb these costs.

There were indications that Morocco’s OCP was re-entering the acid market, but details could not be confirmed. OCP will be finding it challenging to source raw material sulphur due to the closure of the Strait of Hormuz, but any acid purchases are unlikely to make much impact to offset lost sulphur supply. For now, the c.fr assessment climbed based on the high European f.o.b. prices.

END OF MONTH SPOT PRICES