European ammonia imports

Europe is likely to become an increasing ammonia importer over the coming years as low global ammonia prices and high European gas prices squeeze producer margins, but CBAM remains a wild card.

Europe is likely to become an increasing ammonia importer over the coming years as low global ammonia prices and high European gas prices squeeze producer margins, but CBAM remains a wild card.

Gas consumption is rebounding in Europe as prices stabilise at lower levels, while the LNG market continues to see large capacity additions.

The 2026 Nitrogen+Syngas Expoconference will take place in Barcelona, Spain, from 9-12 February. Join us at this industry leading event where leading market and technology experts and producers will gather to connect, share knowledge and learn about the latest developments in operations, technology, processes and equipment.

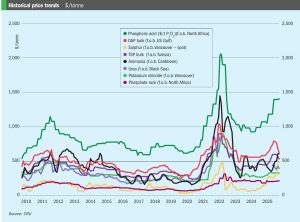

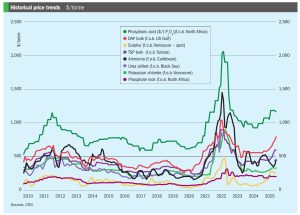

Price trends and market outlook, 18th December 2025.

We look ahead at fertilizer industry prospects for the next 12 months, and the key economic and agricultural drivers likely to shape the market.

Fertilizer sales to Brazilian farmers are currently in line with the average of the past three years, despite variations by crop and state. CRU’s Anthony Rizzo and Bruno Fardim Christo of Veeries provide an update on the status of fertilizers and crops in the Brazilian market.

Filipe Gouveia , BIMCO’s shipping analysis manager, looks ahead at the dry bulk market and freight rate prospects for 2026.

In this CRU Insight, Humphrey Knight assesses the key market factors driving high SOP pricing.

Globally, operational renewable ammonia projects have exceeded one gigawatt (GW) of installed electrolyser capacity for the first time. Kevin Rouwenhorst of the Ammonia Energy Association (AEA) provides an overview of well-advanced projects and the associated technology options for ammonia synthesis.

Price trends and market outlook, 23rd October 2025