Fertilizer International 527 Jul-Aug 2025

7 July 2025

Market Insight

Market Insight

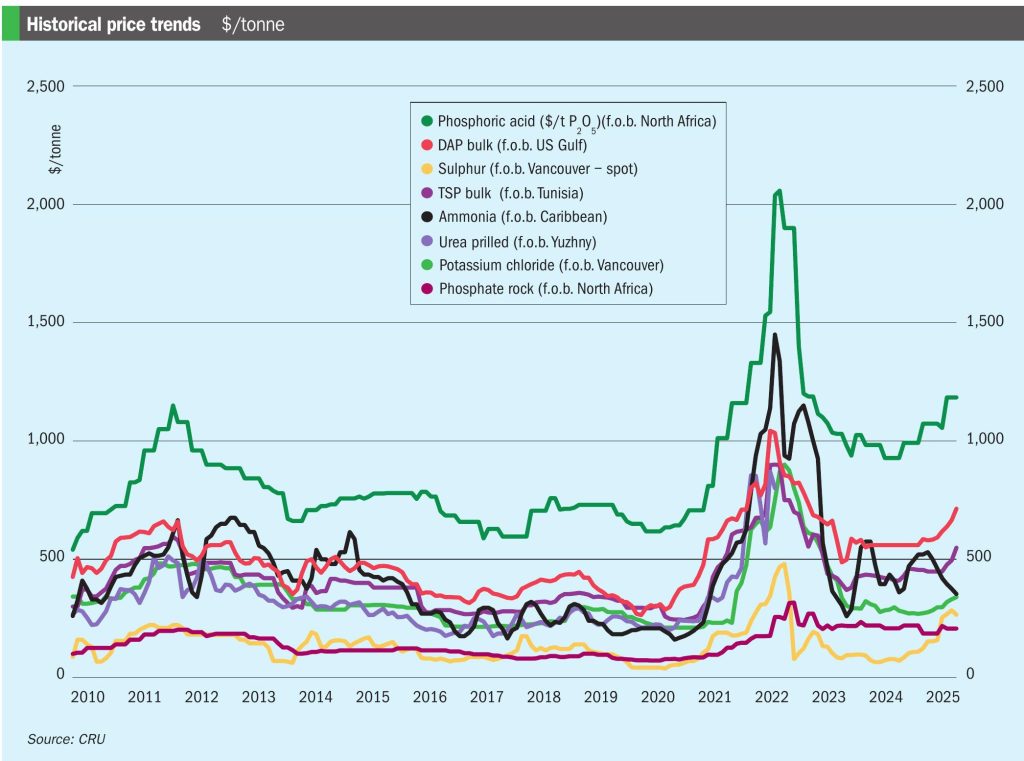

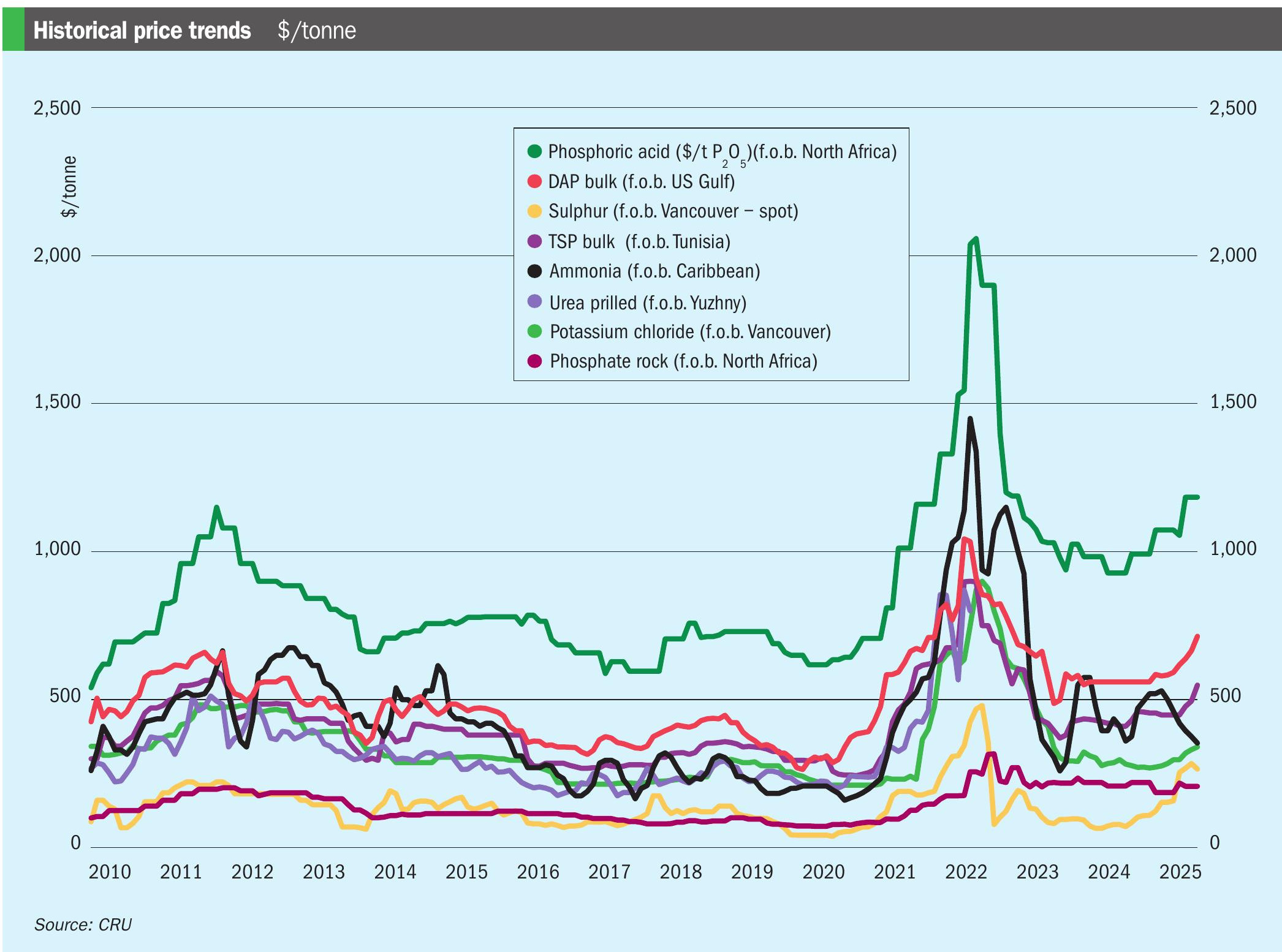

PRICE TRENDS & OUTLOOK

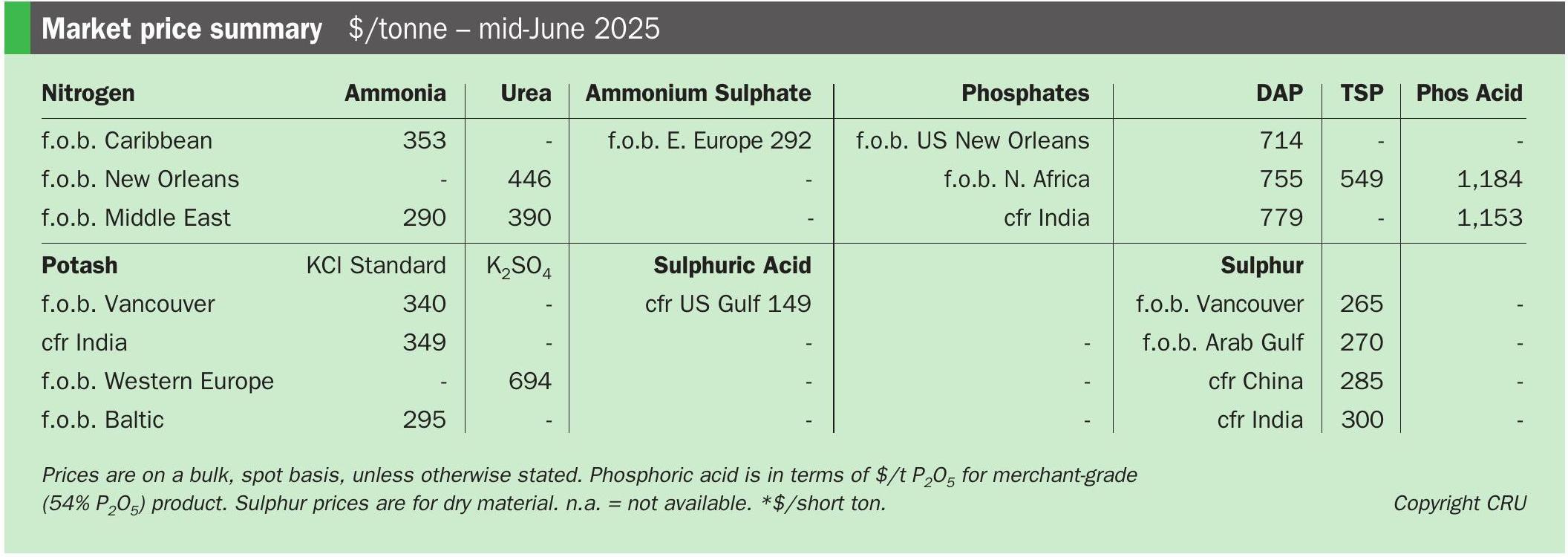

Market snapshot, 19th June 2025

Urea prices escalate as supply tightens.

Global supply has been severely reduced due to the unexpected attack by Israel on Iran in mid-June and the consequent retaliation.

Gas supply from Israel to Egypt was cut on 13th June taking out potential exports as high as 400,00-500,000 tonnes a month. All plants in Iran were taken down on 16th June as a precautionary measure amid news that gas fields feeding the plants had been hit. About 500,000 tonnes/month of Iranian capacity has been taken out of production as a consequence.

Middle East prices made significant gains in the week 13-20th June. Sabic stepped in and sold a cargo for July at $402/t f.o.b., some $12/t higher than secured by Fertiglobe out of Ruwais on 12th June. It then placed another 40,000-45,000 tonne cargo at $450/t f.o.b.

Algerian prices also escalated immediately. A sale of 20,000-25,000 tonnes was reported from AOA at $417/t f.o.b. Arzew on 13th June. AOA kept selling with prices reported around $443-450/t, culminating in August tonnes trading at $471/t f.o.b. Sorfert then sold some smaller lots at $475/t and $500/t, peaking with the sale of 10,000 tonnes at $520/t f.o.b. on 19th June.

In India, NFL’s 1.5 million tonnes import tender suffered from very unfortunate timing. Sellers were unwilling to commit as the market surged, although they now have until 23rd June to decide.

Russia also pulled back to assess the market – having agreed urea sales of $350/t f.o.b. for prills and $360/t f.o.b. for granular product prior to the conflict. Rises in prices of up to $400/t f.o.b. prills and $430-440/t f.o.b. granular were subsequently reported.

Brazil, meanwhile, has traded at $430/t cfr, largely due to Chinese availability.

The short-term urea outlook is firm. The market is on tenterhooks waiting for the next move in this conflict. Further price escalation is possible – if production is not resumed quickly.

Middle East instability puts ammonia buyers on alert

For the most part, ammonia prices have remained stable, at least for now, with supply-demand dynamics still largely balanced – despite heightened tensions in the Middle East and subsequent impacts to regional supply.

Prices east of Suez registered only marginal movements, despite ongoing regional turbulence, with the Middle Eastern supply picture supported by the news that Ma’aden will export another 150,000 tonnes in July.

Talk of a $430/t f.o.b. sale out of Algeria reflected the overall bullish mood. If confirmed, the business would likely fetch at least $470-480/t cfr in NW Europe.

In the US Gulf, there is still little news on the next exports from the Gulf Coast Ammonia (GCA) complex in Texas. Further along the coast, CF is continuing to load at least three cargoes from Louisiana for export.

In the short term, prices may well have found a floor with both Iranian and Egyptian production offline, as of 19th June, with rising natural-gas prices also likely to support sentiment going forward.

India drives bullish phosphates momentum. Global DAP/MAP prices continued to increase in mid-June. A range of benchmarks were assessed higher with India’s DAP market remaining the main driver of bullish momentum.Spot DAP prices in India were assessed at $775-782/t cfr, with at least one sale to a trader concluded above $800/t cfr. The current price mid-point is at its highest level since September 2022, being up from $636/t cfr in mid-March and $695/t cfr at the start of May.

OCP says it has sold 55,000 tonnes of DAP for July loading to India at $800-805/t cfr. The buyer is understood to be a trader.

MAP spot sales to Brazil were also assessed up at $740-750/t cfr.

DAP demand from Ethiopia has further tightened the market. EABC received a range of offers from traders for an additional 171,000 tonnes of DAP, with all offers for supply from China. The importer has issued a wave of DAP tenders over the past several months, soaking up DAP supply as it pivots away from NPS.

Phosphate prices are expected to increase further over the short term, as demand picks up while supply remains exceptionally tight. While affordability concerns persist, buyers have limited options. Any reversal in market direction now seems unlikely until at least the third quarter.

MOP market sees price gains

Potash prices have risen across Southeast Asia, Northwest Europe, China and the US, following recent contract settlements, as the market closely monitors the Israel-Iran conflict for potential supply disruptions.

So far, production in Israel and neighbouring Jordan remains unaffected, despite Jordan’s gas supply being cut off. The two countries each accounted for around 5% of global potash exports in 2024.

Despite the off-season, China’s domestic market has seen a rise in potash buying inquiries and transactions due to market uncertainty following China’s contract settlement at $346/t cfr on 12th June. January-May imports totalled 5.7 million tonnes, according to China Customs data.

Potash prices in Southeast Asia rose in mid-June despite seasonally slow demand. Standard MOP prices reached $345–360/t cfr, with July offers as high as $370/t cfr.

Indian importers have moved quickly with ongoing tenders from NFL and FACT after settling their potash contract at $349/t cfr on 5th June. Import volumes are expected to rise in coming weeks to replenish supplies and meet increased Rabi season demand.

Brazilian spot prices have remained flat at around $363/t cfr for the last six weeks. In the US, meanwhile, Nutrien announced its long-awaited summer fill prices for MOP, setting Midwest prices slightly above expectations at $390/st f.o.b.

Looking ahead, potash prices are expected to continue to adjust upwards in the coming weeks, although concerns over Brazil’s price outlook are emerging, with some believing the market is nearing its ceiling.

Middle East tensions limit sulphur declines

Global sulphur prices remained mostly stable, with the recent downward trend halted by the Israel-Iran conflict. The mutual attacks – while introducing uncertainty to Middle East pricing and its future direction – have yet to directly affect the market. Import demand in both China and Indonesia remains subdued, as buyers are sufficiently covered through June and July.

Several unsold Middle Eastern and Canadian sulphur cargoes destined for China were reported to have changed hands in mid-June. Domestic prices in China surged to RMB2,450-2,460/t FCA, in the aftermath of the Israel-Iran conflict, implying a delivered price near $292-294/t cfr.

Prices in the Mediterranean decreased amid a lack of activity and weakened regional demand. The latest transaction into Brazil also left prices unchanged in mid-June. Canada, meanwhile, saw stable Vancouver f.o.b. prices with limited activity taking place in the way of fresh exports.

Global sulphur prices are expected to experience a period of stability in the short-term, as the market adjusts to the Iran-Israel conflict. Buyers in Asia also remain covered throughout June and July. Only limited activity is therefore likely in coming weeks.