Fertilizer International 527 Jul-Aug 2025

7 July 2025

The long-term SOP outlook – a hot topic

POTASSIUM FERTILIZER OPTIONS

The long-term SOP outlook – a hot topic

In this CRU Insight, Wahome Muya and Willis Thomas of CRU Consulting take a deep dive into the long-term prospects for the potassium sulphate (SOP) market. In particular, they ask what impact could export controls in China have on SOP market dynamics over the next 25 years?

Introduction

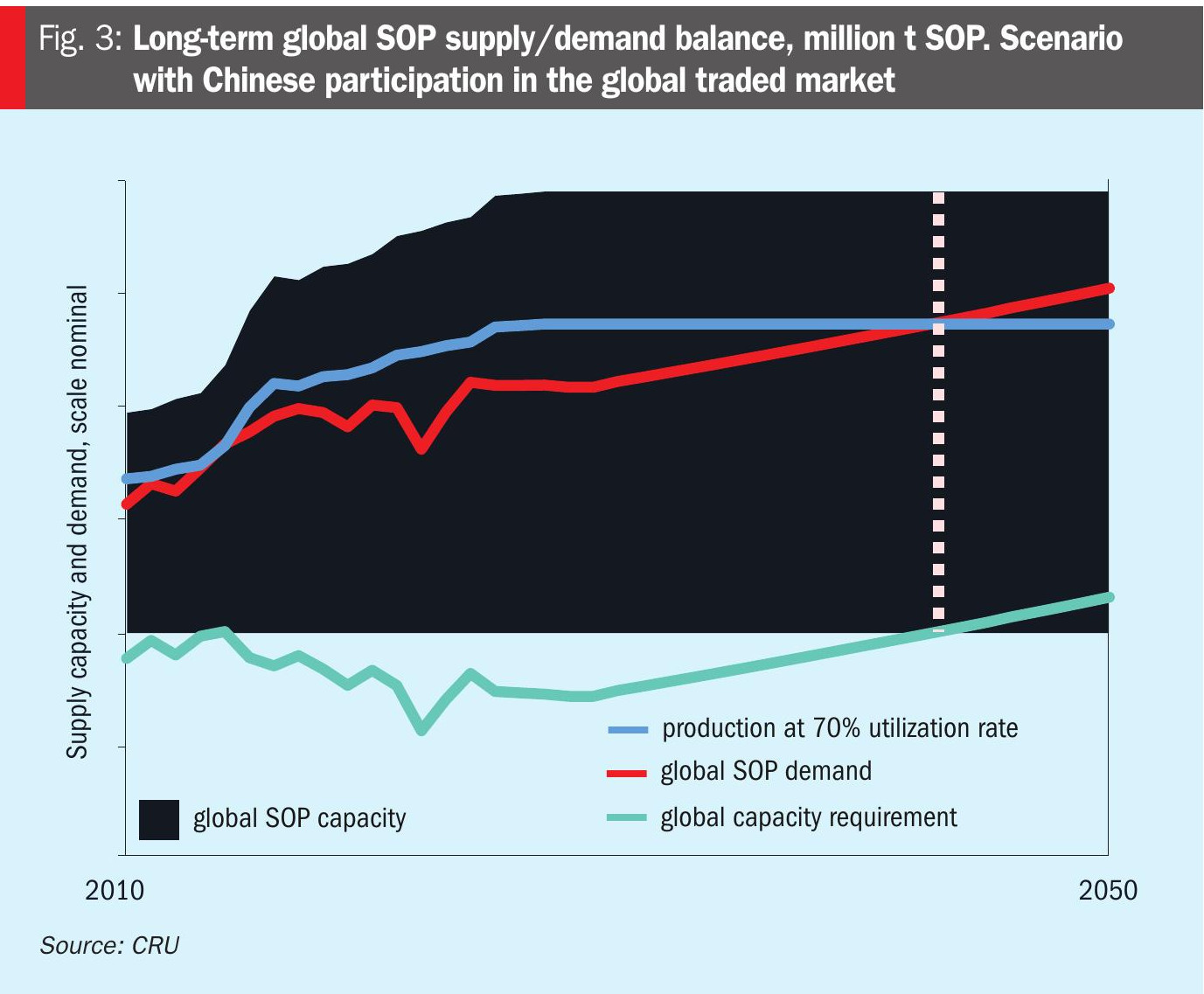

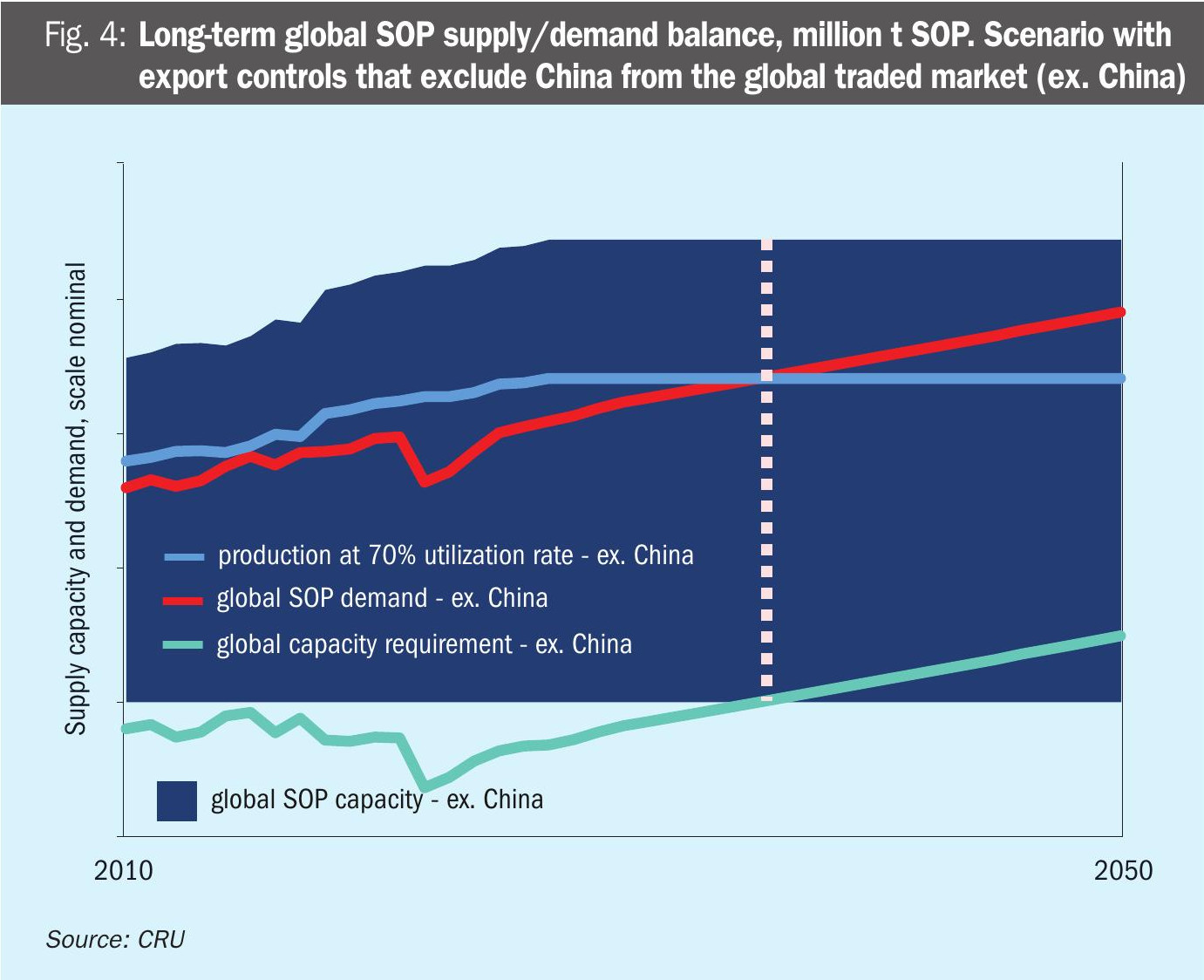

In CRU’s recently produced Potassium Sulphates Long Term Special Report, we show global potassium sulphate (SOP) supply/demand balances under two scenarios – both with and without Chinese capacity and demand being accounted for in the global picture.

This includes analysis of the specific years in which the global SOP market is set to balance, with and without Chinese participation, and the accompanying long-term price forecasts associated with each scenario. Our analysis is underpinned by an overview of long-term demand drivers, key demand-related risk factors, and an evaluation of regional SOP demand dynamics.

CRU Consulting’s special report answers the following key questions:

• What are the key drivers underlying long-term growth in SOP demand, and in what regions are they most prevalent?

• What are the key agricultural, policy, and tech-related risks to long-term SOP demand growth?

• At what point in time do we expect a capacity requirement to emerge in the global SOP industry, and how does Chinese export policy affect that timeline?

• What is the long-term outlook for SOP market prices, and how are they determined?

Being comprehensive in scope, the report provides:

1. An overview of long-term drivers behind fertilizer demand, and contrasts these with short- and medium-term drivers.

2. Analysis of key long-term demand risks, including resource constraints, climate change, and policy.

3. Long-term global K2 O nutrient and SOP demand forecasts.

4. Overview of regional SOP demand dynamics, and underlying SOP demand drivers.

5. Global SOP supply/demand balances for two different China-based scenarios.

6. Long-term SOP price forecasts to 2045.

SOP – a popular alternative

Although potassium chloride (MOP) will remain the primary source of K2 O for nutrient consumption over the long term, SOP is the principal alternative potassium-based fertilizer consumed by farmers today. The popularity of SOP is mainly due to its low chloride levels – versus high chloride MOP – combined with its ability to provide sulphur as a crop nutrient, plus the ample availability of the product in water-soluble form.

Most crops have some degree of sensitivity to chloride, which can have detrimental effects on the quality (size, weight, colour, shape, taste, etc.) of some ‘premium’ crop categories, such as fruits, vegetables, tree nuts and tobacco, these being highly chloride sensitive. Approximately 20% of the world’s harvested area is used to cultivate such chloride-intolerant crops, and chloride sensitivity can be a particular issue in regions with little rainfall and/or poor drainage, as chloride can accumulate in the soil.

Additionally, although sulphur has historically had little value as a crop nutrient, demand for sulphur-containing fertilizers has risen notably over the last 20 years. This has been necessary in response to a decline in atmospheric deposition of sulphur to soils (via industrial SO2 emissions), as well as increasing levels of agronomic education and soil testing in the emerging agricultural economies.

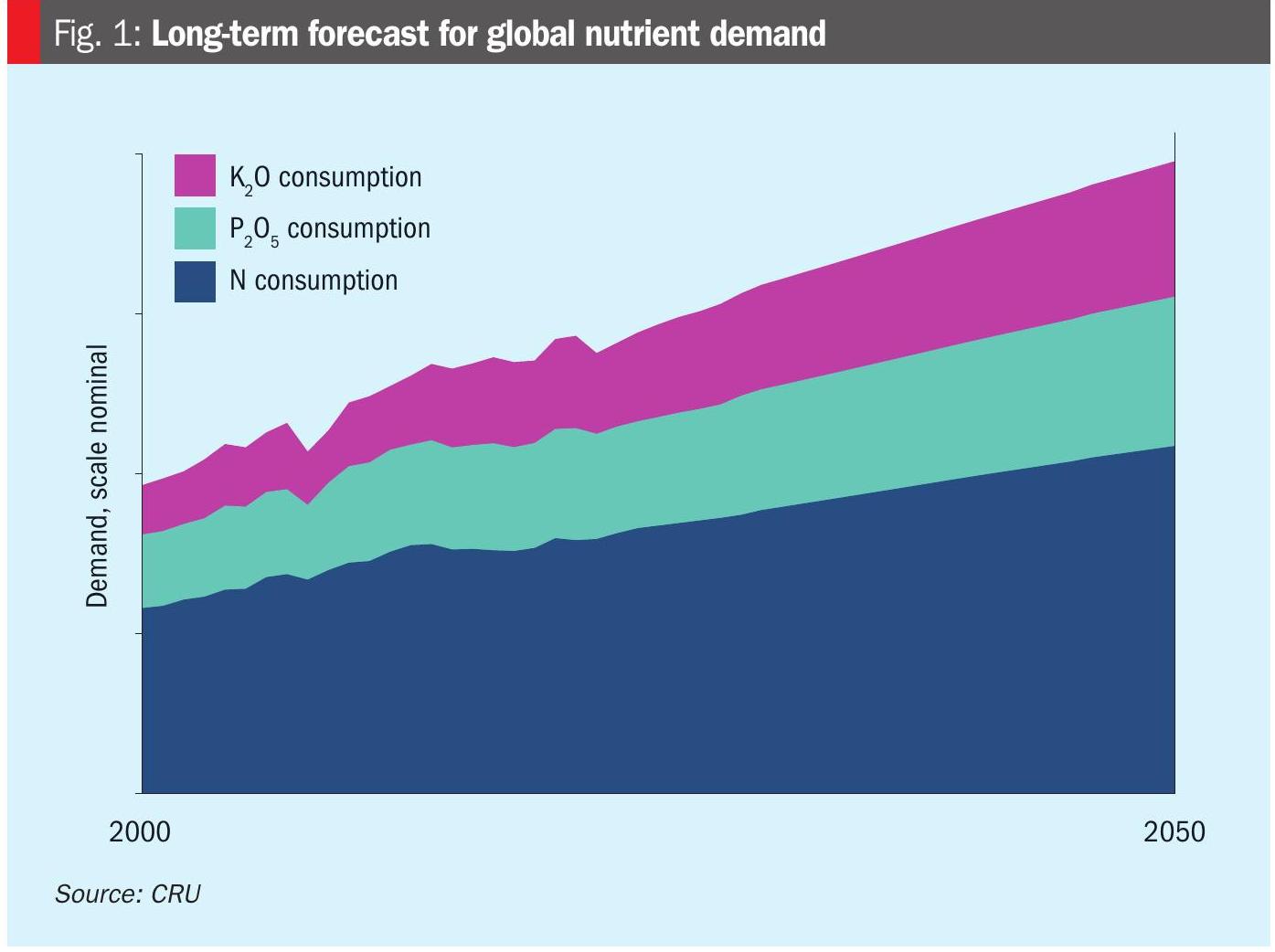

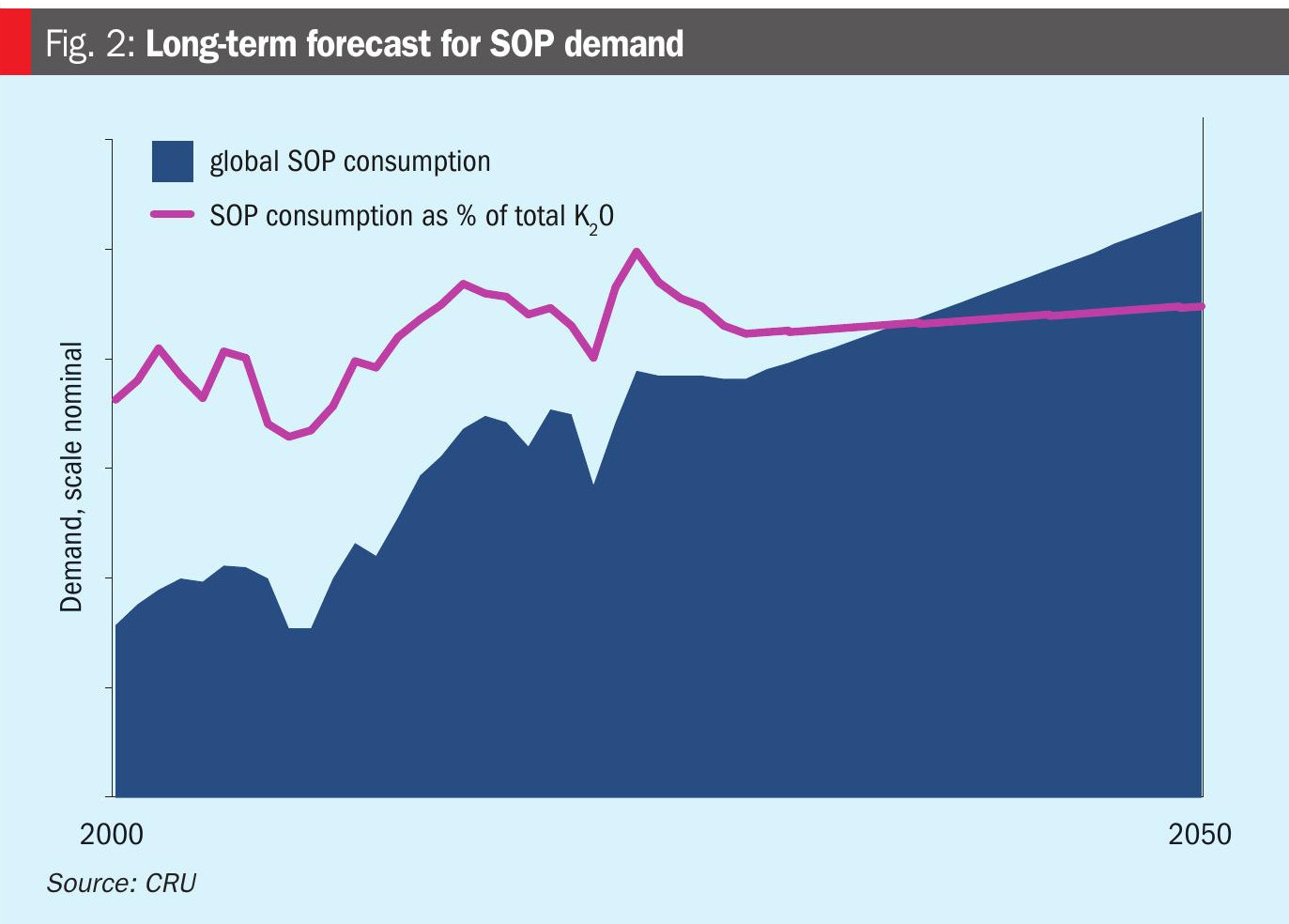

With global agricultural demand for potassium set to increase (forecast at 1.8% CAGR from 2023-50) – driven by a rebalancing of nutrient consumption ratios away from nitrogen in key fertilizer-consuming countries such as China – we expect the share of K2 O consumption accounted for by SOP to at least maintain its historical average of 8-9%.

High analysis MOP will remain the agricultural mainstay for potassium fertilization of crops. Although the relative abundance and lower cost of MOP supply will support its growing consumption over the long term (Figure 1), the expansion of fruit and vegetable crop areas in key markets such as China – together with improved farmer agronomic knowledge in emerging agricultural centres such as Africa – should enable SOP to maintain its share of potassium nutrient demand (Figure 2).

Future SOP capacity – when and how much?

CRU uses supply gap analysis to forecast the long-term global capacity requirement in the SOP industry. This is defined as the gap between our long-term global SOP demand forecast, and global SOP capacity at the end of the medium-term forecast in 2029. We are able to predict – up until this point – the timings and production volumes associated with individual projects in our pipeline.

A key area of uncertainty over the long term is the extent to which Chinese SOP supply should be considered in a global market balance. On the one hand, Chinese SOP exports peaked at nearly 400,000 tonnes in 2020 – at the time, making China the joint second largest SOP exporter in the world. Since mid-2021, however, China has put in place SOP export controls due to concerns about food security and high domestic prices. These controls were then intensified, firstly in October 2021 and again in January this year. Consequently, Chinese SOP exports for 2025 are expected to total only ~75,000 tonnes.

Chinese participation holds the key

Essentially, there is significant uncertainty surrounding the long-term future of Chinese SOP export restrictions, in terms of both their duration and severity. Although Chinese export restrictions seem unlikely to be lifted in the short-medium term, for a 25-year forecast horizon this becomes impossible to predict.

As a result, our long-term view of the SOP industry needs to take into account both scenarios – one with Chinese participation in the global traded market and the increased SOP supply availability that results from this (Figure 3), and another where the duration and severity of SOP export controls in China do not subside, and the country virtually functions as a separate, self-contained market (Figure 4).

In the report, we show the specific years in which the global market is set to balance, with and without Chinese participation, and the accompanying long-term price forecasts associated with both scenarios.

The long-term SOP outlook – a hot topic

The outlook for SOP over the longer term has become something of an industry hot topic for several reasons:

Firstly, Chinese participation in the global traded market is a major point of uncertainty. One of the key questions explored in the report is the potential impact that Chinese export restrictions may have on long-term supply/demand balances in the SOP industry. The maintenance of export restrictions into the long-term could significantly tighten the global market balance, but a resumption of Chinese seaborne supply would exacerbate global oversupply.

Secondly, the demand potential associated with chloride-sensitive crops in key markets. The long-term growth prospects associated with SOP are linked to its use in the application of chloride-sensitive crops such as fruits, vegetables, tree nuts, and tobacco, where use of SOP is much more suitable than application of MOP. While SOP demand stemming from these crop categories is significant in markets such as China, other major producers of these crops such as India have a very nascent SOP market currently.

Thirdly, questions remain in relation to the long-term industry marginal producers. Over the past 10-15 years, we have seen significant efforts by project developers in regions such as Western Australia and Eastern Africa to advance primary SOP projects. However, these nascent industries have hit problems since 2021 in raising capital and navigating political instability. Meanwhile, established secondary SOP producers in regions such as NW Europe and East Asia continue to represent relatively stable, important sources of supply to the global traded market, and will likely continue to do so in the long term. The choice of long-run industry marginal producers forms the basis of our long-term price forecasts.

Find out more

We look forward to exploring how CRU Consulting can help you deepen your understanding of SOP industry dynamics, supply/demand balances under different China-related scenarios, and implications for long-term pricing.

You can find out more about CRU’s long-term outlook for the SOP industry in the CRU Potassium Sulphates Long Term Special Report. If you are interested in this report, please reach out and contact us below.

About the authors

Wahome Muya is CRU’s Senior Consultant, CRU Consulting wahome.muya@crugroup.com Tel: +44 20 7903 2145

Willis Thomas is CRU’s Principal Consultant, CRU Consulting willis.thomas@crugroup.com Tel: +44 20 7076 0280