Nitrogen+Syngas 402 Jul-Aug 2026

13 July 2026

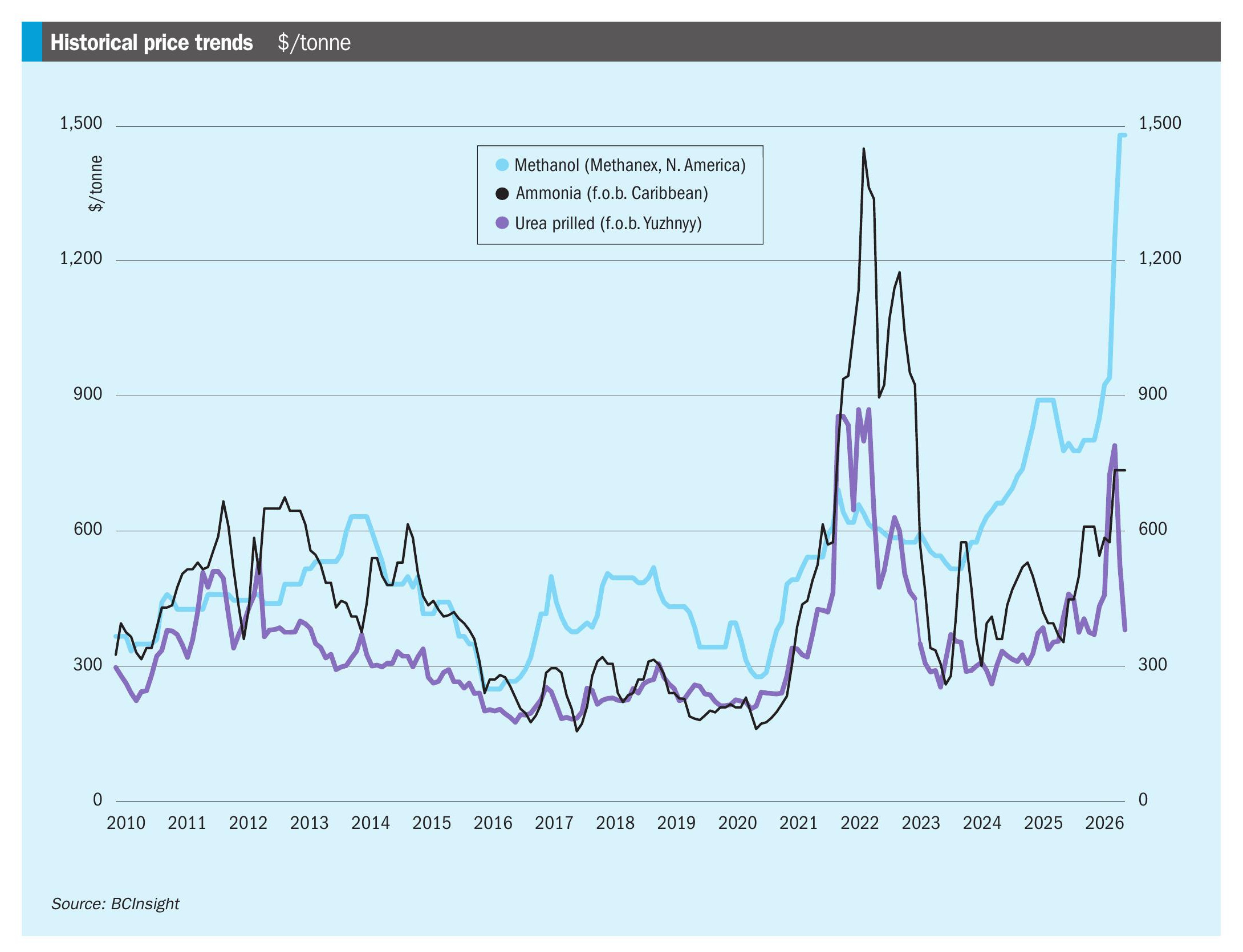

Temporary relief for markets

“There is still considerable distance between the US and Iranian positions…”

The signing of a memorandum of understanding between the United States and Iran on June 17th has provided relief across most markets as both sides agreed to allow ships to transit the Strait of Hormuz, at least in terms of trapped vessels from the Gulf being able to exit.

Relief was most evident in urea markets, where around 820,000 tonnes of urea on 20 vessels has now been able to leave the Gulf in the two weeks (at time of writing) since the agreement, and prices have fallen to ‘normal’ levels for this time of year. Ammonia has taken longer to turn the corner, but all indications at the start of July are that prices are also coming down, with Chinese supply helping to lengthen Asian markets. However, freight rates and war risk premiums continue to limit the pace at which supply can return. It was a different story in phosphate markets, however, where continuing high sulphur prices have kept phosphate and hence ammonium phosphate rates high.

However, it is also evident that there is still considerable distance between the US and Iranian positions over the tentative agreement, and the 60 day deadline that the MoU stipulates to resolve these differences begins to look very ambitious, with agreements over uranium enrichment or ‘downblending’, sanctions relief and the freeing of frozen Iranian funds all still to be hammered out, let alone a cessation of the Israeli conflict in Lebanon. Both sides have also faced domestic pushback on the concessions that they have already agreed. A series of violations of the ceasefire have added to the uncertainty, with a Singaporean container ship being struck by an Iranian drone on June 25th, and a fresh round of US strikes on Iranian targets and Iranian counter-strikes on Bahrain and Kuwait on June 28th. Qatar has suspended all maritime navigation. Nevertheless, talks continue, at least for now, albeit with a break for the official state funeral of Ayatollah Khamenei, killed by US airstrikes on February 28th at the outset of the conflict.

What happens after the MoU expires on August 16th remains very uncertain. Iran has indicated that it will seek to impose some kind of tolling arrangement over transits of the Strait, possibly in conjunction with Oman, via an “administrative charge” or similar. President Trump has bluntly said that he would return to bombing Iran. With global inventories in many commodities, but especially oil now heavily depleted, any renewed disruption has the potential to send energy prices sharply higher again.

All of the talk at the IFA annual meeting in Monaco last week was about the potential for a food crisis if fertilizer markets continue to be disrupted out to the end of the year. August 16th will be the date to watch for an indication of how things will go.