Asia

27 May 2026

Hormuz conflict triggers fertilizer support wave

Written by Natalie Noor-Drugan

Strait of Hormuz disruptions linked to the Iran war have choked off fertilizer shipments from the Middle East and pushed prices sharply higher, prompting a wave of emergency support and trade measures as governments try to shield farmers ahead of key planting seasons.

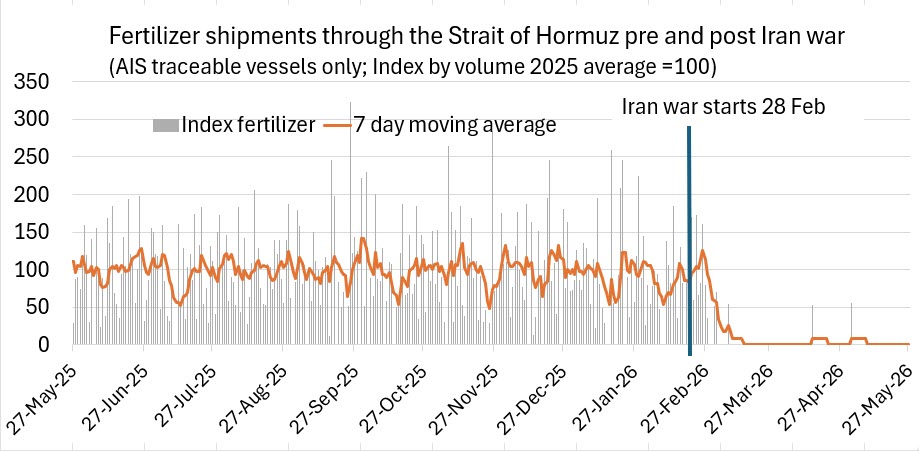

A chart based on analysis of vessel traffic through the Strait shows fertilizer-related sailings falling to a fraction of pre-conflict levels, with only sporadic movements since early March. The Strait of Hormuz is a critical corridor for Middle Eastern nitrogen and sulphur exports, so even a short-lived interruption has immediate repercussions for fertilizer markets and farm input costs.

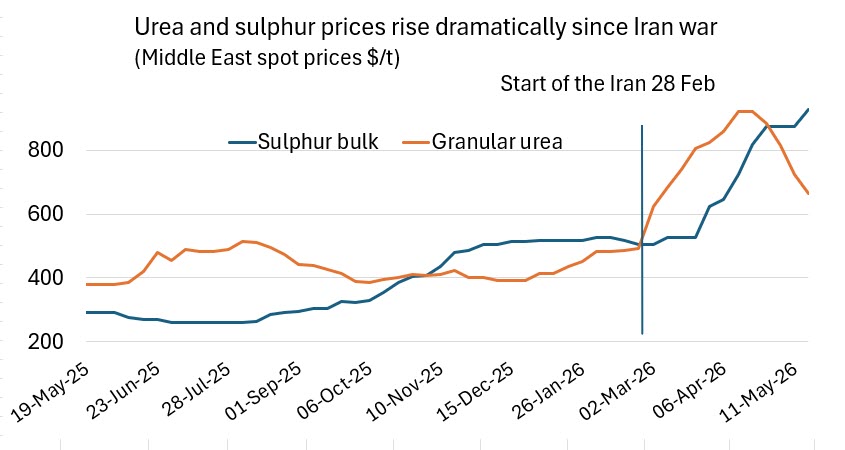

Price data underline the scale of the shock. Bulk sulphur spot prices have more than tripled over the past year, rising from around $293/t fob Middle East in mid-May 2025 to $928/t by 18 May 2026. Granular urea has followed a similar path: from $379/t on 19 May 2025 it climbed steadily, reaching $920/t in late April 2026 before easing back to $665/t by 18 May. The combination of disrupted flows through Hormuz and higher feedstock and freight costs is tightening margins across the fertilizer value chain and squeezing farmer affordability.

Industry warns on affordability and food security

Producers warn that while physical shortages remain localised, the affordability shock is already undermining fertilizer use and, by extension, crop yields.

“The Middle East plays a critical role in global fertilizer and energy markets, and the situation is putting significant pressure on the global food system, with knock-on effects across the value chain, including increasing challenges to farmer affordability,” said Hanna Opsahl-Ben Ammar, Executive Vice President at Yara.

“Fertilizers are fundamental to global food production – roughly half of global food production depends on them. Stable, affordable access is critical for farmers to produce the food the world needs. In most parts of the world, the issue is not physical availability, but affordability. Higher prices disproportionately affect those least able to absorb them, with direct consequences for farmers and food security.”

India leans on higher subsidies

India has chosen to absorb much of the increase in international prices through its long-standing subsidy system. On 8 April, the government increased Nutrient-Based Subsidy rates for phosphatic and potassic fertilizers for the 2026 Kharif season, with a total budget allocation of INR415.3 billion ($5.0 billion), up INR43.2 billion ($520 million) from 2025.

By holding domestic prices relatively steady, policymakers are aiming to cushion farmers from the sharp rise in imported nutrient costs at a politically sensitive point in the crop cycle.

Europe broadens support

In the European Union, the main short-term response has come via a temporary state-aid framework for sectors hit by the Middle East crisis, alongside wider efforts to improve fertilizer resilience. The framework allows member states to compensate farmers for up to 70% of additional fuel and fertilizer costs linked to the crisis, with simplified support of up to €50,000 per beneficiary, and runs until 31 December 2026.

Brussels has also adopted a broader Fertiliser Action Plan, which uses CAP tools, the agricultural reserve and more flexible advance payments to improve liquidity and help farmers manage elevated nutrient costs. It also aims to reduce import dependence over time by encouraging better nutrient management and the wider use of organic, bio-based and recycled fertilizers.

France has layered national measures on top of EU instruments. In early April, the government announced “flash fuel loans” of up to €50,000 for small and medium-sized firms in sectors such as agriculture, transport and fisheries that are heavily exposed to fuel costs, alongside other relief on charges and taxes.

In the UK, there has been no crisis‑specific fertilizer subsidy on the scale seen in the EU or India. Support has instead focused on longer‑term measures that reduce dependence on manufactured nutrients – such as slurry‑infrastructure grants and Sustainable Farming Incentive options linked to nutrient management – and on modernising the regulatory framework. In March 2026, the UK government and devolved administrations opened an eight‑week consultation on new UK Fertilising Product Regulations, aimed at widening access to innovative, lower‑impact fertilizing products and strengthening resilience to global market shocks

US farm-aid package takes shape

In the United States, lawmakers are discussing using an Iran-related supplemental spending bill to carry a farm-aid package of roughly $15 billion. While details are still being negotiated, the expectation is that some of the support would help farmers dealing with high production costs, including fertilizers and fuel, although no dedicated fertilizer package has yet been formally announced.

China nudges the market, not dominates it

China has largely stepped back from the international sulphur market this year as buyers have been priced out by record-high import costs, while at the same time reopening urea exports under a tightly controlled quota system with high floor prices. Together, these moves show Beijing limiting its exposure to elevated sulphur prices while carefully managing how its nitrogen tonnes reach the global market.

With Strait of Hormuz flows still constrained, sulphur and urea prices elevated compared with a year ago, and the conflict’s duration uncertain, governments may have to extend or deepen support schemes as the 2026–27 planting cycle approaches. For now, the policy response remains a patchwork of national and regional measures, but the common thread is clear: keeping fertilizers within reach of farmers has become a front-line food-security priority.