Asia

27 May 2026

China’s sulphuric acid export halt tightens global supply

Written by Natalie Noor-Drugan

China’s sulphuric acid exports fell 49% year on year to 666,808 t in the first four months of 2026 as Beijing moved from quota controls to a full export halt from May, removing a key supplier from the seaborne market at a time of already tight balances. CRU analysis of Global Trade Tracker (GTT) data shows that January–April shipments were capped by a 700,000 t export quota designed to protect domestic supply, ahead of a policy shift that has now “halted all exports from the beginning of May through to the end of 2026”, effectively turning China into a “no market” in CRU’s weekly assessments since early May.

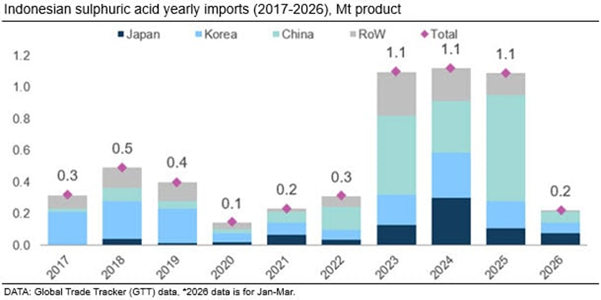

The export mix in the first four months underlines how broad the disruption will be for international buyers. Indonesia was the largest outlet over January–April with 163,119 t, down 22% year on year, followed by Chile at 119,890 t, a 75% drop, and Saudi Arabia at 103,039 t, down 37%. In contrast, India increased purchases by 20% to 102,488 t and the Philippines by 68% to 63,929 t, as importers scrambled to secure tonnes ahead of the expected shutdown. In April alone, exports totalled 138,447 t, led by Indonesia (59,699 t), Chile (30,000 t), Saudi Arabia (19,039 t) and Vietnam (18,733 t), leaving little room under the 700,000 t cap and signalling that volumes would fall to zero from May.

CRU notes that the export ban has now been in force long enough for China’s sulphuric acid export market to be assessed as “no market” for two consecutive weeks, with no confirmed spot business and prices therefore derived notionally from netbacks. On this basis, the notional FOB range is unchanged at $300‑390/t, calculated from recent CFR business into India at $350‑400/t, Indonesia at $380‑400/t and Chile at $490‑510/t. Inside China, market participants are already debating how long the policy will last, particularly as demand from the downstream phosphate sector softens and the risk of a domestic surplus grows. Some sources speculate that Beijing could relax the restrictions later this year, but CRU stresses that there has been no official indication of any change and that such talk remains purely speculative.

Globally, the loss of Chinese tonnes is significant and immediate. China exported around 3.3 Mt of sulphuric acid over May–December 2025; removing that volume for the same period in 2026 creates a supply gap that “no other region can fill”, according to CRU. Import‑dependent regions such as Latin America and Southeast Asia will have to compete harder for alternative supplies from Japan, Korea, the Middle East and Europe, at a time when many smelters and sulphur burners are already constrained by maintenance, feedstock and environmental factors. CRU expects the market to remain structurally short through the rest of 2026, supporting firm prices in key export basins and reinforcing bullish sentiment in both term and spot negotiations.