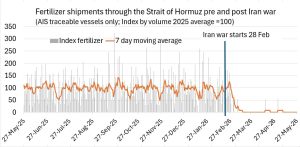

Uncharted waters

The fragile ceasefire between the United States and Iran broke down at the start of July, just three weeks after the signing of the June memorandum of understanding, after Iran fired at several vessels who had failed to notify them of their transit of the Strait of Hormuz, and the US retaliated with a missile barrage. While the two month negotiation period it had specified to solve all of the outstanding issues between the two parties had always seemed over-ambitious, market participants had at least expected to have that grace period to arrange for new cargoes and tranship them through the Strait. Now that the ceasefire has ended early, markets are truly entering uncharted waters.