Nitrogen+Syngas 401 May-Jun 2026

27 May 2026

Convert, compete, or close: European ammonia at the crossroads

EUROPEAN AMMONIA

Convert, compete, or close: European ammonia at the crossroads

VK Arora of Kinetics Process Improvements, Inc. (KPI) looks at how – while carbon border taxes may reshape ammonia trade – the economics of hydrogen and electricity will ultimately determine the long-term competitiveness of European production.

The European Union’s Carbon Border Adjustment Mechanism (CBAM) is reshaping the economics of ammonia trade by embedding carbon compliance costs into imported products. While CBAM aims to equalise carbon exposure between European Union producers and exporters operating in hydrocarbon-advantaged regions, ammonia remains fundamentally an energy-driven commodity.

This article evaluates ammonia competitiveness under CBAM through scenario-based landed-cost modelling, comparing European producers with hydrocarbon-advantaged producers across multiple production pathways, including conventional ammonia, partial carbon capture, and clean ammonia configurations.

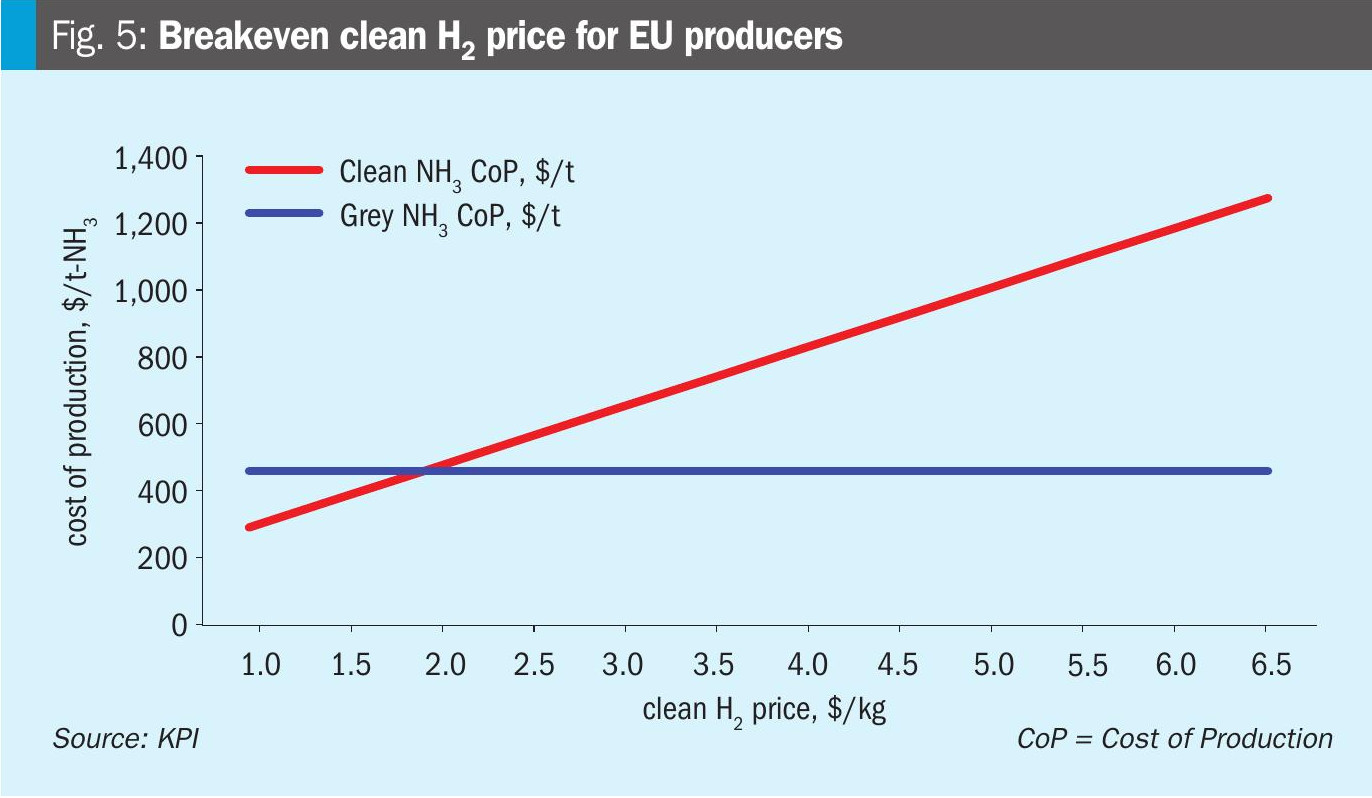

The analysis shows that CBAM narrows, but does not eliminate, the structural cost advantage of hydrocarbon exporters. Clean ammonia production in Europe becomes economically competitive only when low-carbon hydrogen is available at or below $2/kg, which is the estimated breakeven level relative to imported ammonia. Achieving such hydrogen costs is closely linked to the availability of competitively priced electricity. At currently projected hydrogen prices near $5/kg, conversion to clean ammonia is not economically viable. Projected EU ETS carbon compliance costs rise sharply after 2030. At those levels, the capital required for clean ammonia conversion could potentially be recovered within only a few years if breakeven hydrogen pricing becomes available.

A structural turning point

Europe’s ammonia industry is entering a period of structural change driven by three powerful forces: rising carbon costs, persistently high energy prices, and increasing reliance on imports. For decades, European ammonia producers operated competitive plants supported by advanced technology, established infrastructure, and proximity to major fertilizer markets. That balance has shifted significantly over the past decade.

Natural gas prices in Europe remain structurally higher than those in hydrocarbon-advantaged regions such as the United States, North Africa, and parts of the Middle East. Industrial electricity prices are also significantly higher. Because ammonia production is fundamentally a hydrogen production business, these energy price differences translate directly into higher production costs for European plants.

At the same time, carbon pricing under the European Union Emissions Trading System (ETS) has transformed carbon emissions from an environmental metric into a material operating cost. As carbon prices rise and free allowances decline, carbon compliance increasingly affects plant utilisation, operating margins, and long-term investment decisions.

The Carbon Border Adjustment Mechanism (CBAM) extends carbon pricing to imported products by requiring importers to pay for the embedded emissions associated with production outside Europe. While CBAM reduces carbon leakage risks, it does not eliminate the underlying energy cost differences that shape ammonia competitiveness.

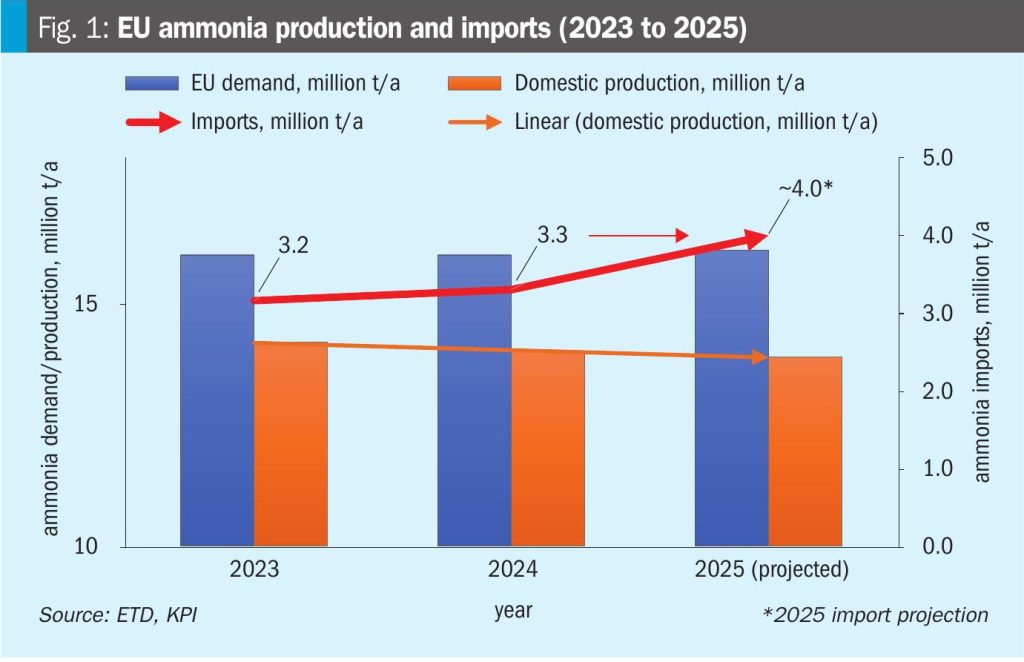

As shown in Figure 1, Europe has become increasingly dependent on imported ammonia as domestic production has declined due to rising energy costs. The economic question facing the industry is therefore not simply how carbon costs affect production, but whether European plants can transition to low-carbon ammonia production while remaining globally competitive.

Carbon pricing and CBAM exposure

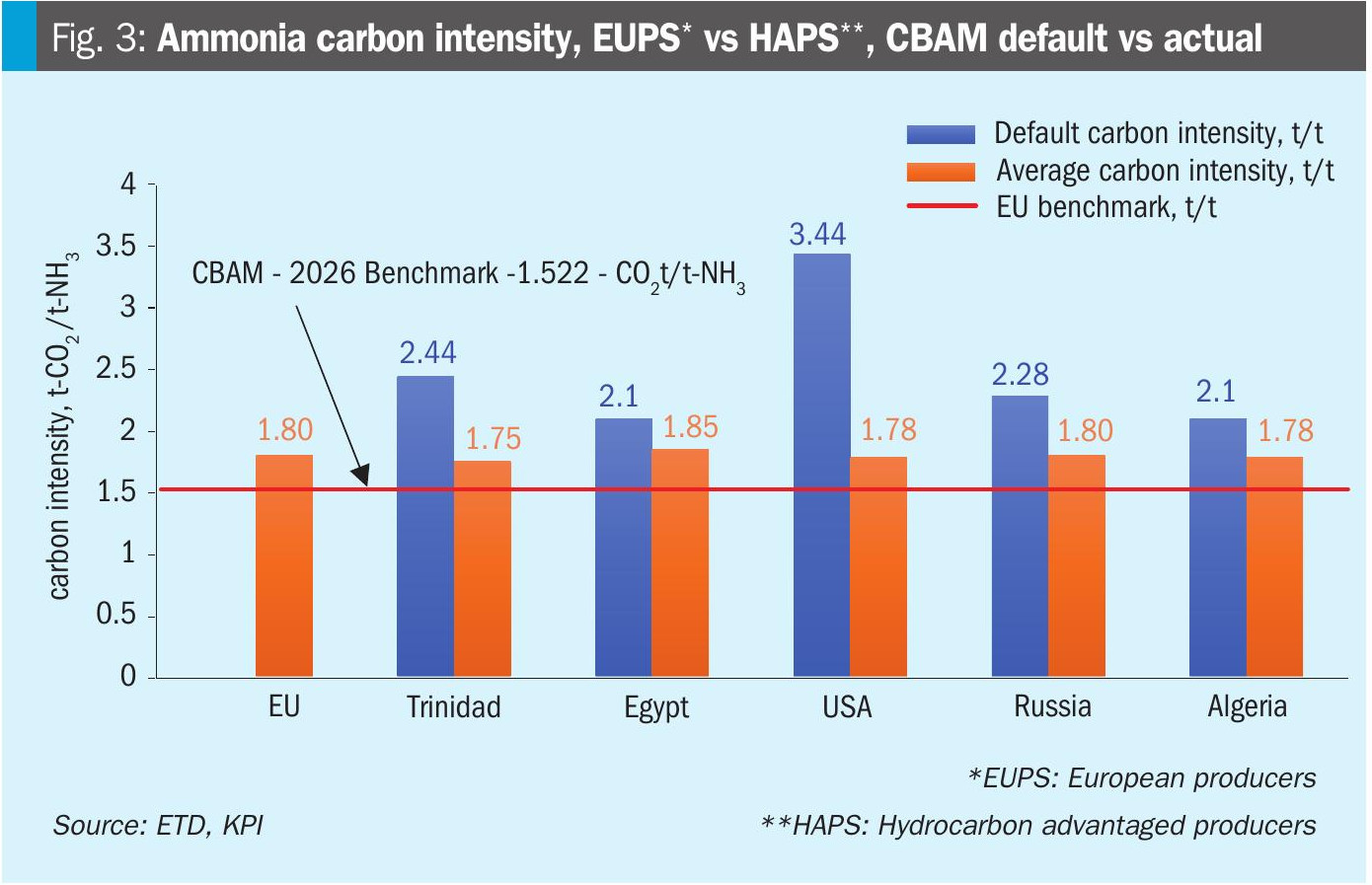

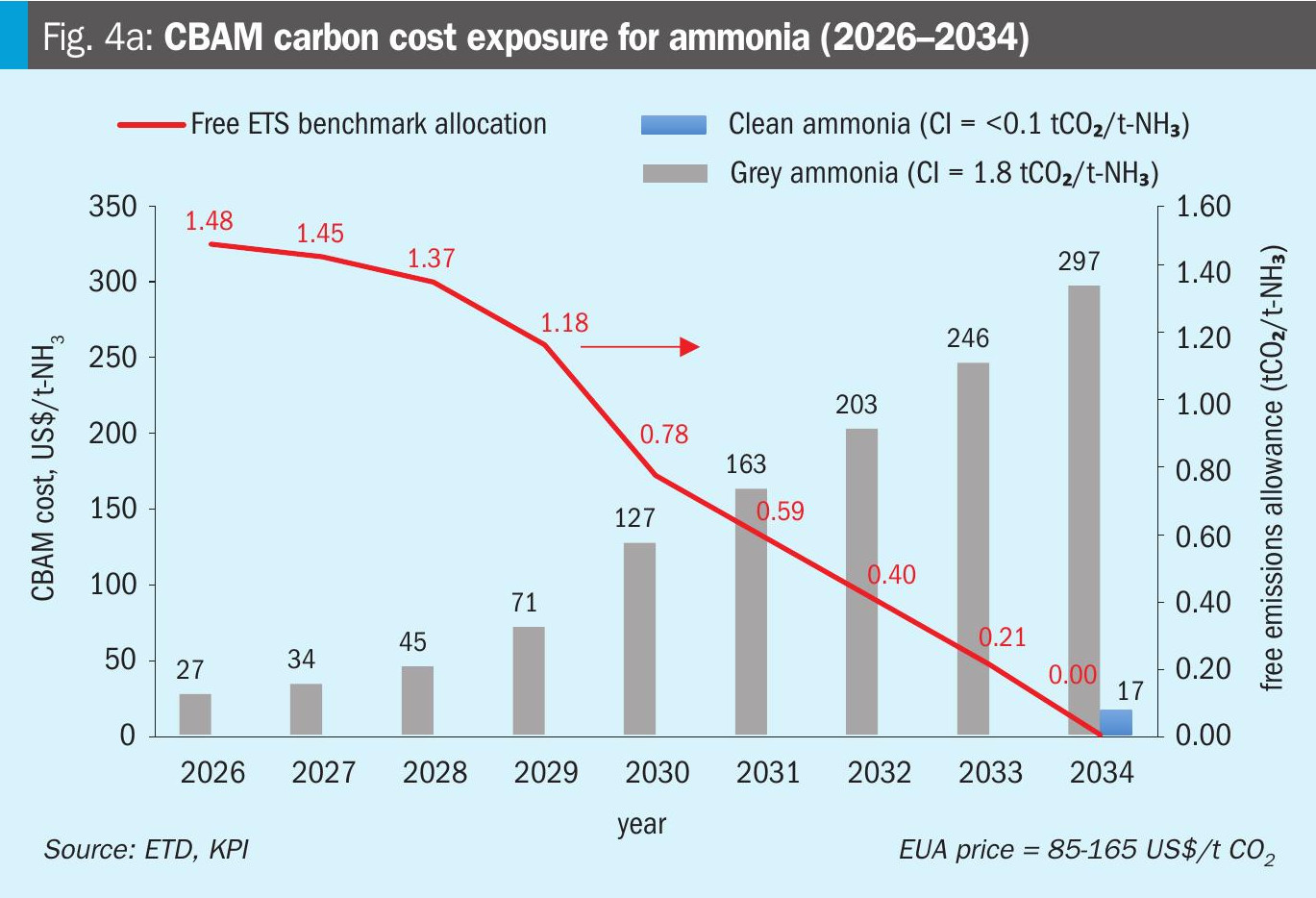

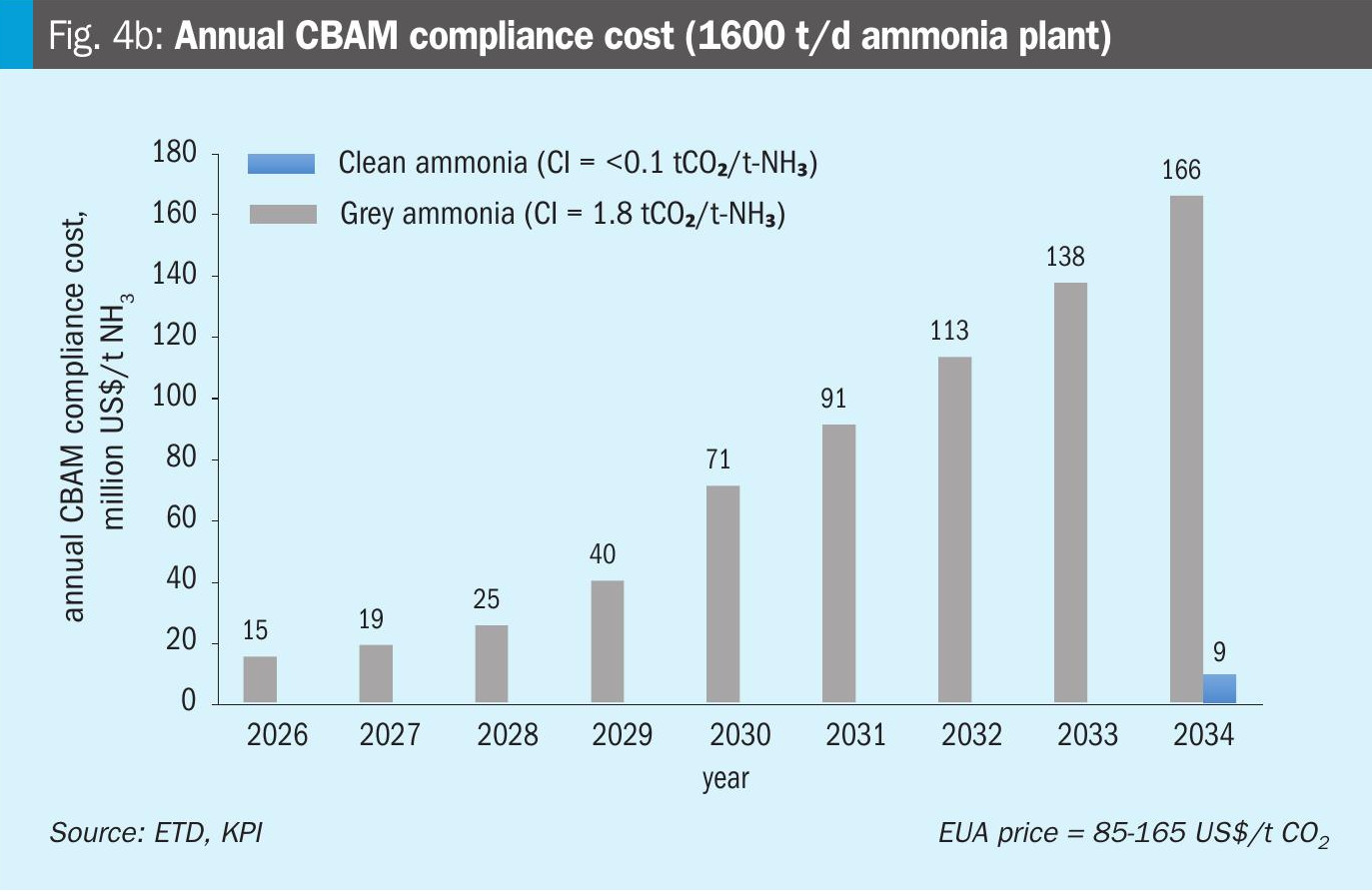

Carbon pricing is rapidly becoming a major economic driver for European ammonia producers. Conventional ammonia plants typically emit around 1.8 tonnes CO2 per tonne of ammonia, creating significant compliance costs under the EU ETS. As illustrated in Figures 4A and 4B, carbon costs rise sharply as free allowances decline and carbon prices increase. For a typical 1,600 t/d ammonia plant, annual compliance costs could reach very substantial levels by the early 2030s. At this point, carbon costs become comparable to major operating cost components of ammonia production. Carbon exposure, therefore, shifts from a regulatory issue to a central financial factor affecting plant competitiveness and long-term asset value.

The rapid escalation of carbon costs also changes the economics of decarbonization. If low-carbon hydrogen becomes available near the estimated breakeven level of approximately $2/ kg, the capital required to convert existing ammonia plants to clean production could potentially be recovered within only a few years through avoided carbon compliance costs. However, current hydrogen price expectations near $5/ kg make such conversions uneconomic. Under these conditions, conventional production combined with carbon compliance remains the least-cost operating strategy in the near term.

CBAM partially reduces the competitiveness gap by applying equivalent carbon costs to imported ammonia. Nevertheless, the mechanism cannot eliminate the structural advantage enjoyed by producers located in regions with significantly lower energy costs.

Scenario framework and methodology

To evaluate how carbon policy interacts with energy economics, a series of scenarios was analysed comparing European Union Producers (EUPS) with Hydrocarbon-Advantaged Producers (HAPS).

The analysis focuses on the landed cost of ammonia delivered to European ports, allowing a direct comparison between domestic production and imported ammonia.

For imported ammonia, the landed cost includes production cost at the exporting facility, marine transport, insurance and logistics charges, and CBAM compliance cost. For European producers, the cost includes production costs (variable and fixed costs) and carbon compliance costs under the EU ETS. Freight and logistics values used in the analysis represent indicative estimates based on publicly available market information and are intended for comparative analysis rather than precise transactional pricing.

The study evaluates a base case representing pre-CBAM market conditions, followed by six post-CBAM scenarios reflecting different production and decarbonisation pathways. In this analysis, clean ammonia refers to ammonia produced using low-carbon hydrogen supplied through the planned European Hydrogen Backbone (EHB) or equivalent infrastructure. Competitiveness assumes hydrogen availability near $2/kg, the estimated breakeven level required for European production to approach parity with imported ammonia. The resulting cost differentials are illustrated in Figures 6–11, while Figure 12 summarises the comparison across the base case and all post-CBAM scenarios.

Base case

The base case represents the ammonia market’s competitiveness before CBAM implementation, when imported and domestic ammonia were subject to fundamentally different carbon cost regimes and no carbon border adjustments were applied. Under these conditions, both European Union Producers (EUPS) and Hydrocarbon-Advantaged Producers (HAPS) operate conventional grey ammonia plants based on natural-gas reforming and hydrogen production.

Production economics are therefore primarily determined by natural gas prices and plant operating efficiency. Producers located in hydrocarbon-advantaged regions benefit from structurally lower natural gas costs, which translate directly into lower hydrogen and ammonia production costs.

Transportation, insurance, and logistics costs represent a relatively small portion of the total delivered ammonia cost compared with feedstock economics. Consequently, exporters from low-gas-cost regions retain a clear economic advantage in supplying ammonia to European markets.

The resulting cost differential between European production and imported ammonia before the CBAM is illustrated in Figure 12, which serves as the reference point for evaluating the post-CBAM scenarios discussed below.

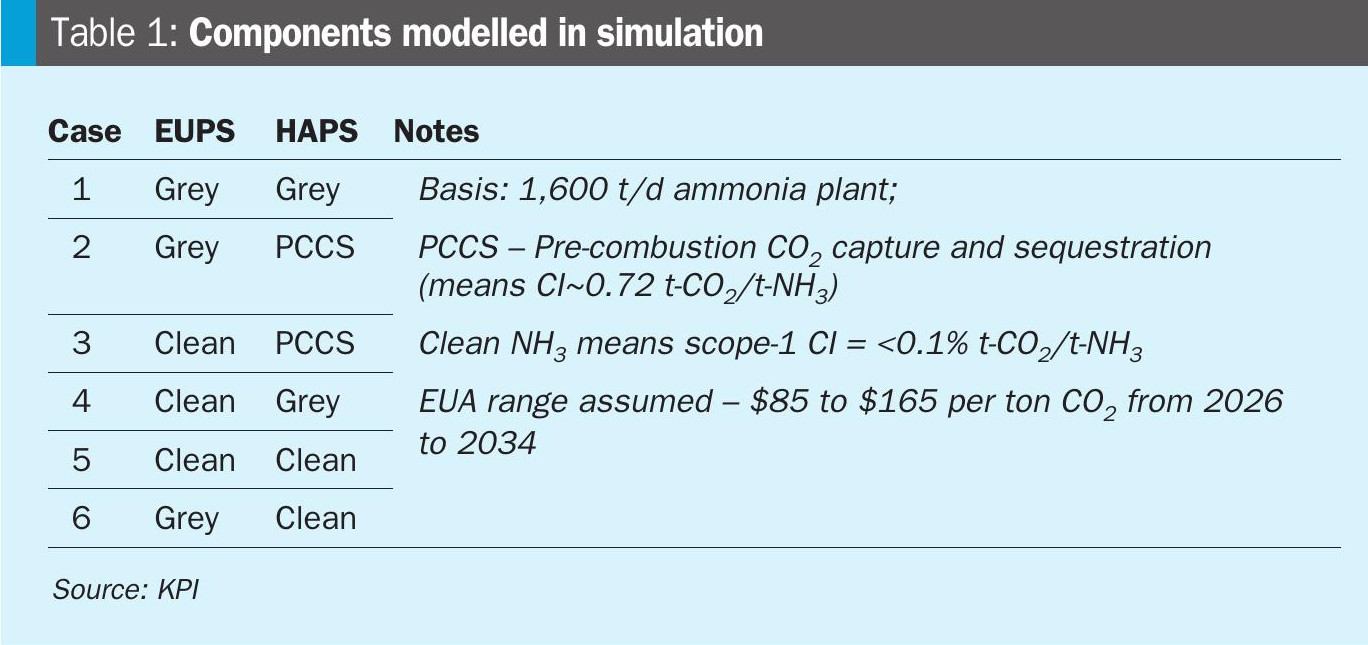

Post-CBAM scenarios evaluated

Six scenarios were evaluated to assess how carbon pricing and technology choices influence ammonia competitiveness following the implementation of the CBAM. Scenario definitions are summarized in Table 1, while the resulting cost differentials are presented in Figures 6–11.

In this analysis, clean ammonia refers to ammonia produced using low-carbon hydrogen supplied through the planned European Hydrogen Backbone (EHB) or equivalent hydrogen infrastructure. Competitiveness assumes hydrogen availability near $2/kg, the estimated breakeven level relative to imported ammonia.

Pre-combustion carbon capture (PCCS) refers to the capture of CO2 from process syngas streams. Several ammonia producers in the United States have already implemented such configurations, including CO2 capture, compression, and pipeline transport for geological sequestration, demonstrating the technical feasibility of this approach.

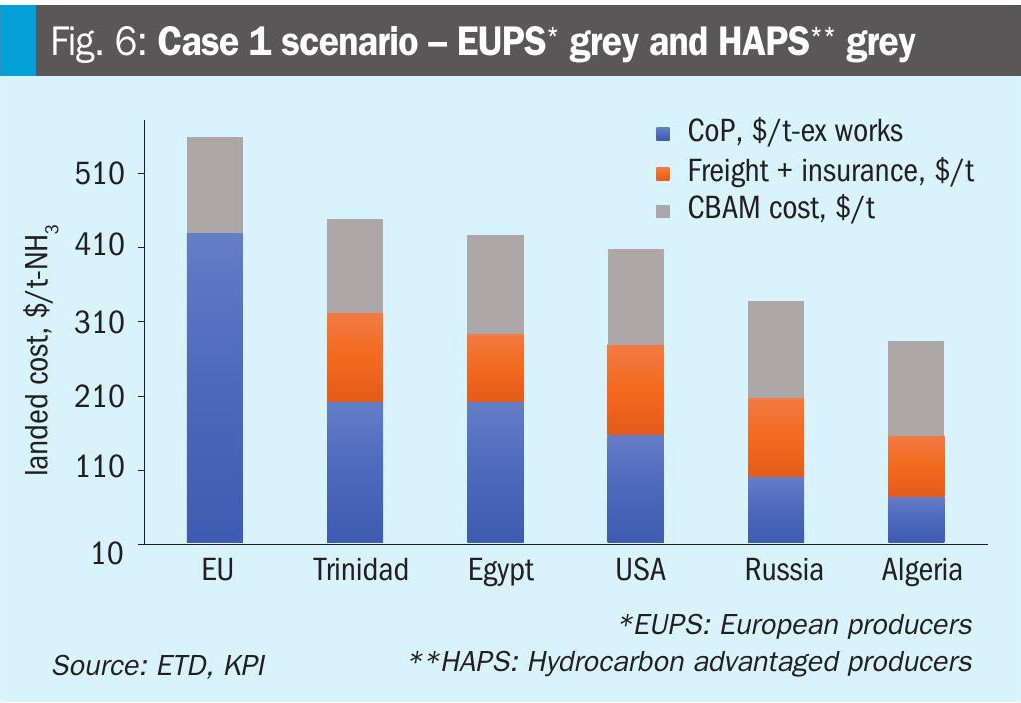

Case 1 – Grey EUPS vs grey HAPS (Fig. 6)

Both regions operate conventional ammonia plants; CBAM adds carbon costs, but exporters retain a strong feedstock advantage.

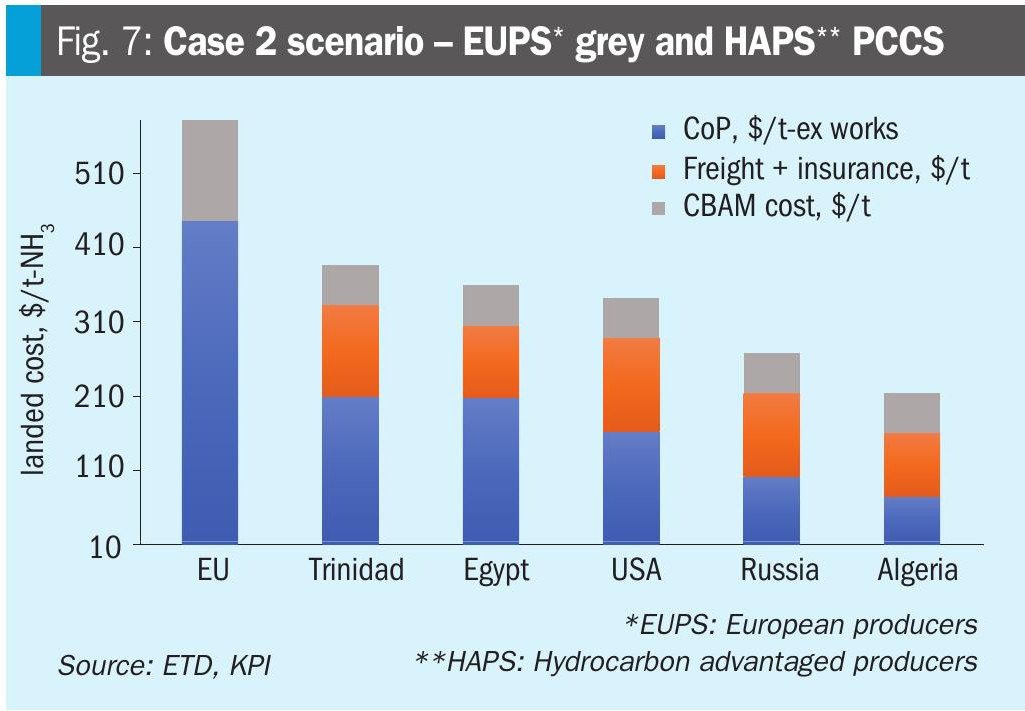

Case 2 – Grey EUPS vs HAPS with PCCS (Fig. 7)

Exporters implement pre-combustion CO2 capture from syngas streams with compression and geological sequestration (PCCS).

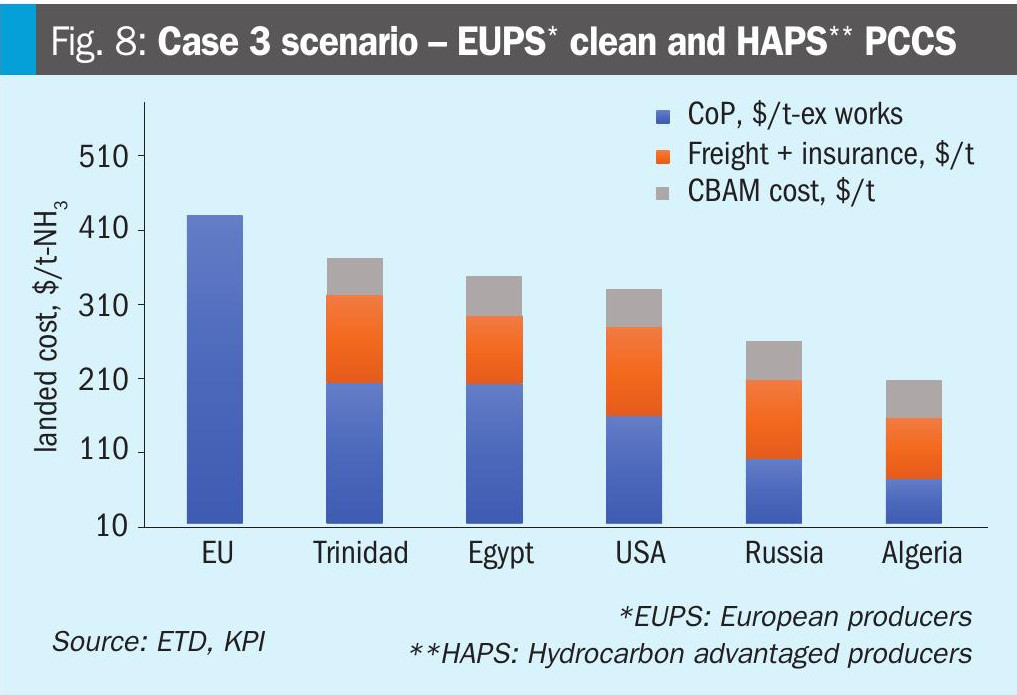

Case 3 – Clean EUPS vs HAPS with PCCS (Fig. 8)

European plants convert to clean ammonia using low-carbon hydrogen while exporters apply partial carbon capture.**

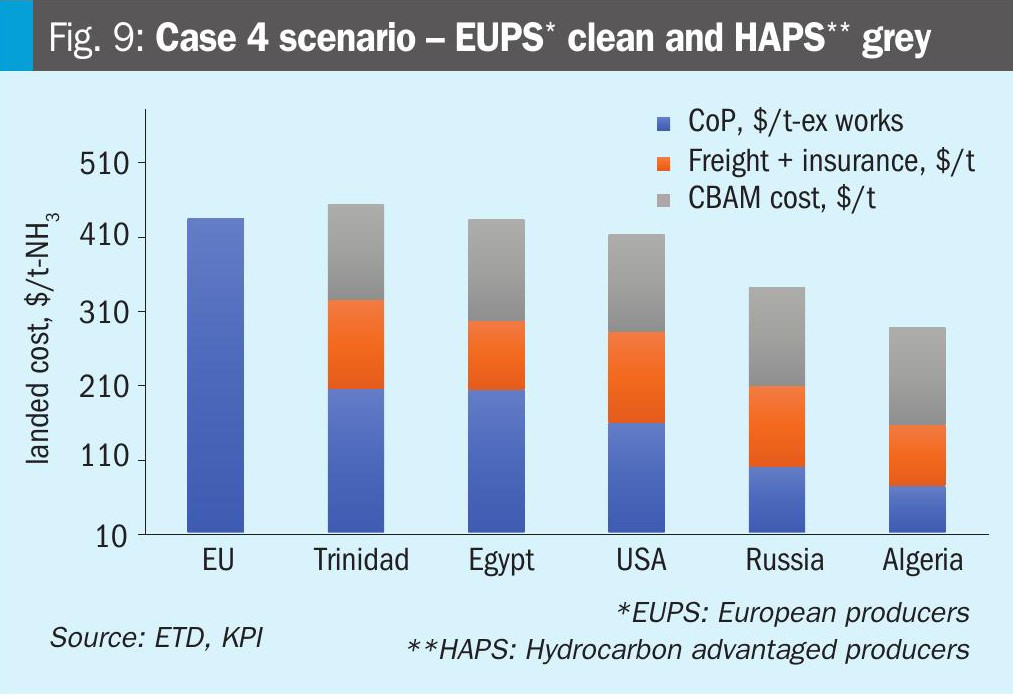

Case 4 – Clean EUPS vs grey HAPS (Fig. 9)

Europe transitions to clean ammonia production while exporters remain conventional and incur higher CBAM exposure.

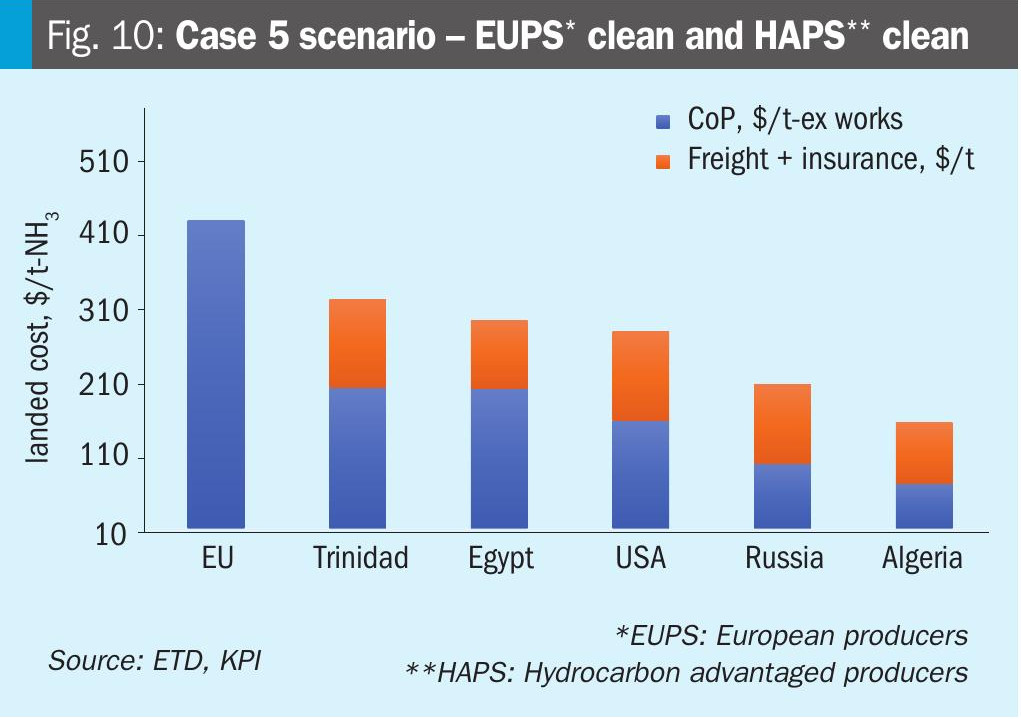

Case 5 – Clean EUPS vs clean HAPS (Fig. 10)

Both regions adopt clean ammonia production; competitiveness is determined mainly by hydrogen and electricity pricing.

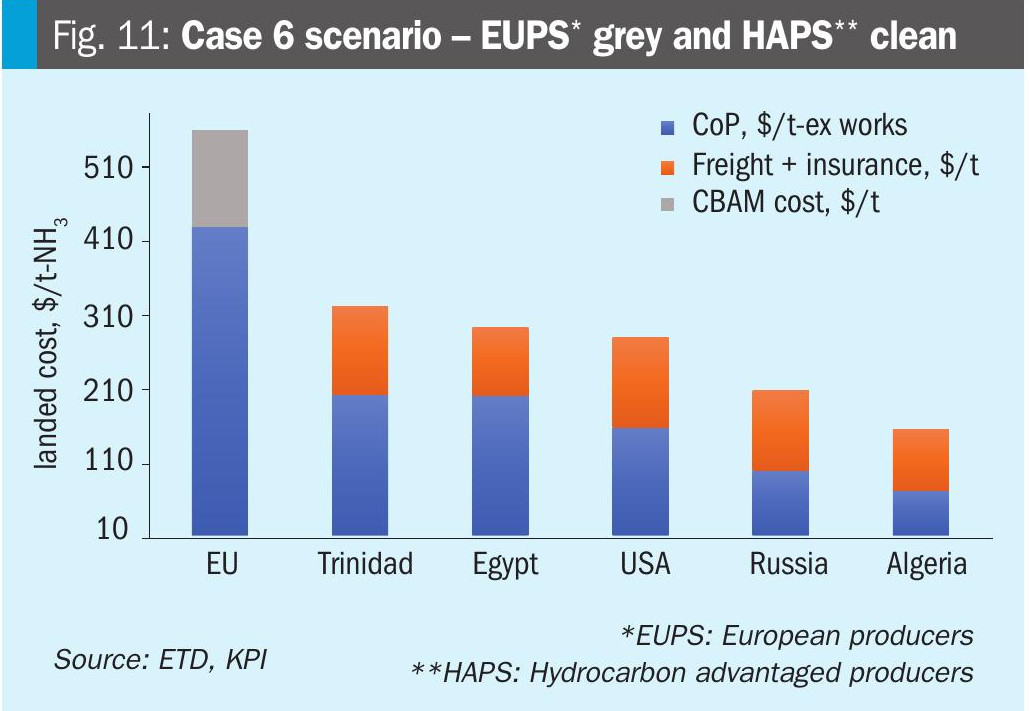

Case 6 – Grey EUPS vs clean HAPS (Fig. 11)

Exporters convert to clean ammonia while European plants remain grey, strengthening import competitiveness.

Taken together, these scenarios illustrate how carbon pricing, hydrogen economics, and technology pathways interact to shape the evolving competitiveness of European and imported ammonia.

Scenario results

The scenario results illustrate how carbon pricing, hydrogen economics, and technology choices influence ammonia competitiveness under CBAM.

In Case 1 (Figure 6), where both regions operate conventional ammonia plants, CBAM introduces additional carbon costs but does not eliminate the structural cost advantage of hydrocarbon-advantaged producers. Lower natural gas prices continue to dominate ammonia economics, allowing exporters to maintain a cost advantage in supplying the European market.

In Case 2 (Figure 7), exporters implement pre-combustion carbon capture (PCCS). Capturing CO2 from process syngas streams and compressing it for sequestration lowers the carbon intensity of ammonia production and reduces CBAM exposure. Because the underlying natural gas advantage remains unchanged, imports remain competitive.

In Case 3 (Figure 8), European producers convert to clean ammonia using low-carbon hydrogen while exporters apply partial carbon capture. Carbon exposure for European plants is significantly reduced, but competitiveness remains strongly dependent on hydrogen and electricity pricing.

In Case 4 (Figure 9), Europe transitions to clean ammonia while exporters remain conventional producers. CBAM increases the cost of imported ammonia due to higher carbon exposure, narrowing the cost differential between imports and domestic production.

In Case 5 (Figure 10), both regions transition to clean ammonia production. Carbon costs largely disappear from the comparison, and competitiveness shifts primarily to the economics of hydrogen and electricity.

In Case 6 (Figure 11), exporters adopt clean ammonia production while European plants remain conventional. In this configuration, exporters benefit from both lower energy costs and reduced carbon exposure, reinforcing the competitiveness of imported ammonia.

The overall comparison shown in Figure 12 highlights a central conclusion: CBAM narrows the cost differential between imported and domestic ammonia but does not eliminate the structural energy advantage of hydrocarbon-advantaged producers.

This becomes increasingly important as carbon compliance costs escalate, as illustrated in Figures 4A and 4B. As EU ETS prices rise and free allowances decline after 2030, carbon costs for conventional ammonia production increase sharply. If low-carbon hydrogen becomes available near the estimated breakeven level of approximately $2/kg, avoided carbon costs could allow the capital required for clean ammonia conversion to be recovered within only a few years.

However, at currently projected hydrogen prices near $5/kg, clean ammonia conversion remains economically unattractive. The analysis, therefore, confirms that while carbon policy influences competitiveness, the decisive factors remain the cost of hydrogen and the electricity required to produce it.

Hydrogen economics and clean ammonia conversion

Hydrogen pricing ultimately determines whether clean ammonia production in Europe can compete with imports. However, the cost of hydrogen is largely determined by the cost of electricity used to produce it via electrolysis.

Current projections for low-carbon hydrogen produced from renewable electrolysis remain near $5/kg or higher, reflecting both electrolyser capital costs and the high price of electricity in many European markets. At this price level, clean ammonia production becomes significantly more expensive than conventional ammonia production in hydrocarbon-advantaged regions.

The analysis in this paper, therefore, evaluates clean ammonia conversion assuming hydrogen availability near $2/kg, representing the estimated breakeven level required for European production to approach competitiveness with imported ammonia under CBAM. Achieving hydrogen costs at this level would require substantially lower electricity prices than those currently observed in many European markets.

At this breakeven level, the economics change significantly. As illustrated by the carbon cost escalation in Figures 4A and 4B, carbon compliance costs for conventional ammonia production increase rapidly after 2030. Avoided carbon costs could therefore offset a significant portion of the capital investment required to convert existing ammonia plants to clean production.

Engineering and economic studies conducted by Kinetics Process Improvements (KPI)—including full conversion design for a 1,600 t/d European ammonia plant, CCS system design, and blue/green hydrogen integration studies—confirm that such transitions are technically feasible but economically dependent on the availability of competitively priced hydrogen and electricity. Nitrogen cost remains relatively minor in the economics of ammonia production. Hydrogen and electricity costs together dominate the economic viability of clean ammonia production.

Conclusions

The introduction of CBAM represents one of the most significant policy interventions affecting global ammonia trade. By extending carbon pricing to imported products, the mechanism reduces carbon leakage and partially narrows the competitive gap between European producers and exporters.

However, the analysis presented in this study demonstrates that carbon pricing alone cannot overcome structural differences in energy costs. Producers located in hydrocarbon-advantaged regions continue to benefit from lower feedstock costs, which remain the dominant driver of ammonia production economics.

Clean ammonia production in Europe becomes economically viable only when low-carbon hydrogen is available at or below $2/ kg, the approximate breakeven level relative to imports. Achieving this level depends strongly on the availability of competitively priced electricity for hydrogen production. At currently projected hydrogen prices near $5/ kg or higher, conversion to clean ammonia remains economically unattractive.

At the same time, carbon compliance costs rise sharply after 2030, as illustrated in Figures 4A and 4B. If hydrogen and electricity costs decline sufficiently to reach breakeven conditions, the avoided carbon costs could allow the capital required for clean ammonia conversion to be recovered within only a few years.

Engineering and economic studies conducted by Kinetics Process Improvements (KPI) – including full conversion design for a 1,600 t/d European ammonia plant, CCS system engineering, and blue/green hydrogen integration assessments – confirm that such transitions are technically feasible but economically dependent on hydrogen and electricity prices.

The strategic choices facing European ammonia producers are therefore becoming increasingly clear: invest in clean ammonia production where competitive hydrogen and electricity become available, maintain efficiency under rising carbon costs, or exit production where economics become unsustainable. In practical terms, the future of Europe’s ammonia industry can be summarized in three words: convert, compete, or close.

References

1. VK Arora, “Challenges in Conversion to Clean Ammonia,” Nitrogen+Syngas Conference, Barcelona, February 2026.