Fertilizer International 522 Sept-Oct 2024

30 September 2024

US fertilizer industry update

COUNTRY REPORT

US fertilizer industry update

The US fertilizer industry, ranked fourth globally in terms of total production capacity, has grown and developed alongside an increasingly sophisticated domestic agricultural sector. The Biden administration has earmarked $900 million for investment in fertilizer assets to boost domestic production capacity and reduce input costs to farmers.

$900 million boost to domestic production

The US Department of Agriculture (USDA) announced an investment of $83 million in domestic fertilizer projects across 12 states at the end of May. The government finance will help build new fertilizer production plants, modernise equipment and install new technologies.

The investment is part of the $900 million committed to domestic fertilizer production in 2022 by the Biden administration under the USDA-administered Fertilizer Production Expansion Program (FPEP). This is designed to boost domestic fertilizer production, increase competition and reduce costs to farmers.

The FPEP was originally started in response to the doubling in fertilizer prices in 2021-2022 triggered by the conflict in Ukraine. To date, USDA has invested $251 million in 57 projects across 29 states through the FPEP. The leaves around $649 million of FPEP funding still to be allocated.

The new tranche of investment announced in May includes the following grants:

- A $25 million grant to 4420 Serrano Drive LLC for a food waste upcycling plant in Jurupa Valley, California. The new plant will supply around 90 local customers with a total of 11,400 tons of organic fertilizers annually.

- A $4 million grant for Cog Marketers, which also operates as AgroLiquid, to build and equip a manufacturing plant in Lake City, Florida. This is expected to produce two million gallons of fertilizer components annually and supply around 200 retailers in Alabama, Florida, Louisiana, Mississippi, North Carolina and South Carolina.

- Return LLC will use a $4 million grant to expand its current production plant in Northwood, Iowa.

Other grants were awarded to projects in California, Florida, Hawaii, Iowa, Illinois, Kansas, Kentucky, Minnesota, North Carolina, North Dakota, Oregon and Washington. The opening by Landus of a new slow-release nitrogen (SRN) manufacturing plant in Boone Iowa, has been one notable beneficiary of FPEP funding (see box)

“The Biden-Harris Administration and USDA are committed to bolstering the economy and increasing competition for our nation’s farmers, ranchers and small business owners,” said USDA Secretary Tom Vilsack in May. “The investments announced today will increase domestic fertilizer production and strengthen our supply chain, all while creating good-paying jobs that will benefit everyone.”

USDA originally announced plans for a $250 million grant programme for additional domestic fertilizer production in March 2022. The scale of the investment was then doubled to $500 million six months later in September 2022.

In June last year, USDA allocated an extra $400 million for fertilizer production expansion – taking total FPEP funding to $900 million. This was in response to level of interest in the programme’s first two funding rounds. These were heavily oversubscribed, receiving applications valued at approximately $3 billion from 350 businesses, according to USDA.

The seven initial FPEP grant winners, selected from 21 shortlisted projects, were also announced in June 2023. These included:

- Black’s Valley Ag Supply Inc – who will build a new dry fertilizer production plant and storage unit in Durand, Wisconsin. The production plant will increase the company’s annual fertilizer production by 33 percent.

- Farmer’s Union Oil Company – who will expand a fertilizer processing plant in rural Montana. This project will increase the supply of local and affordable fertilizers within a four-county region, while creating several local jobs.

- Progressive Ag Cooperative – who will construct a dry fertilizer plant that serves cooperative members from northern Iowa and southern Minnesota.

US industry overview

The United States is the world’s fourth-largest fertilizer consuming region, being responsible for around nine percent of global consumption and ranked behind only China, India and Brazil globally (Figure 1). On an individual nutrient basis, the country is also the world third largest nitrogen and potash consumer and fourth largest consumer of phosphates (Figures 2-4).

The United States has developed a large-scale and responsive domestic fertilizer industry to satisfy the high demand generated by its equally sizeable and sophisticated farming sector. By capacity, the country is the world’s third and fourth largest phosphate and nitrogen fertilizer producer, respectively (Figures 5-6), as well as being the ninth largest potash producing nation globally.

Overall, the US fertilizer industry, is ranked fourth globally, in terms of total production capacity (22.7 million nutrient tonnes), exceeded only by China (81.0 million nutrient tonnes), Russia (31.5 million nutrient tonnes) and its northern neighbour Canada (27.1million nutrient tonnes)1 .

US fertilizer production is stable but in relative decline – with the country’s capacity for phosphate and nitrogen fertilizers being overtaken by Morocco and India, respectively, in recent years.

Urea production

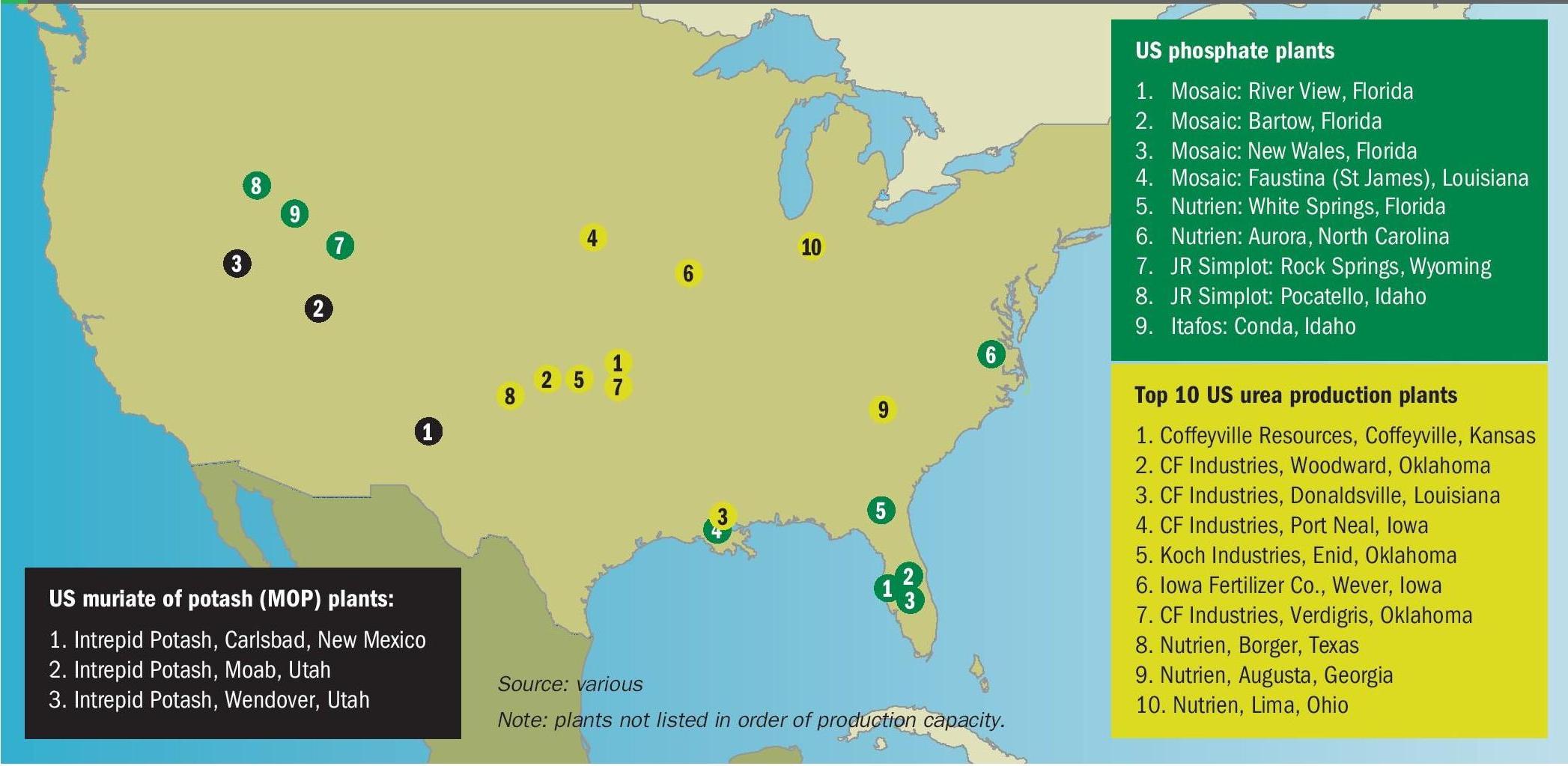

The US operates 12.2 million tonnes of urea production capacity. This is mainly in the hands of CF Industries, Nutrien and Koch industries, with these three companies combined owning 82 percent of domestic urea capacity (Figure 7). Collectively, these leading producers also operates eight of the 10 largest urea plants in the US (Figures 8 & 9). Illinois-headquartered CF industries is the largest US nitrogen fertilizer producer by far, with almost half (48 percent) of domestic urea capacity and operating at around three times the scale of its closest rivals Nutrien and Koch.

The US can draw on 9.3 million tonnes of domestic production capacity for diammonium phosphate and monoammonium phosphate (DAP and MAP). Following several decades of consolidation, phosphate industry ownership is highly concentrated (Fertilizer International 496, p40) with just four companies – Mosaic, Nutrien, JR Simplot and Itafos – operating nine DAP/MAP production sites across Florida, Idaho, Louisiana, North Carolina and Wyoming (Figure 9).

Florida-headquartered Mosaic is the dominant US phosphates market player (Figure 10). It operates around 6.6 million tonnes of DAP/MAP capacity from four sites in Florida and Louisiana. This includes New Wales, the country’s largest phosphates production complex (Figure 11).

Potash

Intrepid Potash is the sole US supplier of muriate of potash (MOP, KCl). The company has the capacity to produce around 365,00 tonnes of potash annually via solar evaporation from three mining sites (Figures 9 and 12):

- The HB solution mine in Carlsbad, New Mexico

- The Moab solution mine in Utah

- The brine recovery operation in Wendover, Utah.

Imports and exports

Due to its limited domestic production capabilities – versus the scale of agricultural demand – the US is the world’s third largest potash importing country, after Brazil and China. The country imported 7.2 million tonnes of MOP in 2022 – albeit down from 10.2 million tonnes in 2021 – sourcing much of this from neighbouring Canada as well as Russia and Israel.

The US produced around 10.6 million tonnes of urea in 2022 supplemented by imports of 5.4 million tonnes. Indeed, the country is a major urea import market, being ranked the third largest globally. The country’s top three urea suppliers in 2022 were Qatar, Saudi Arabia and Russia. US urea exports, meanwhile, around 1.4 million tonnes in 2022, place it outside the global top 10 of urea exporting nations.

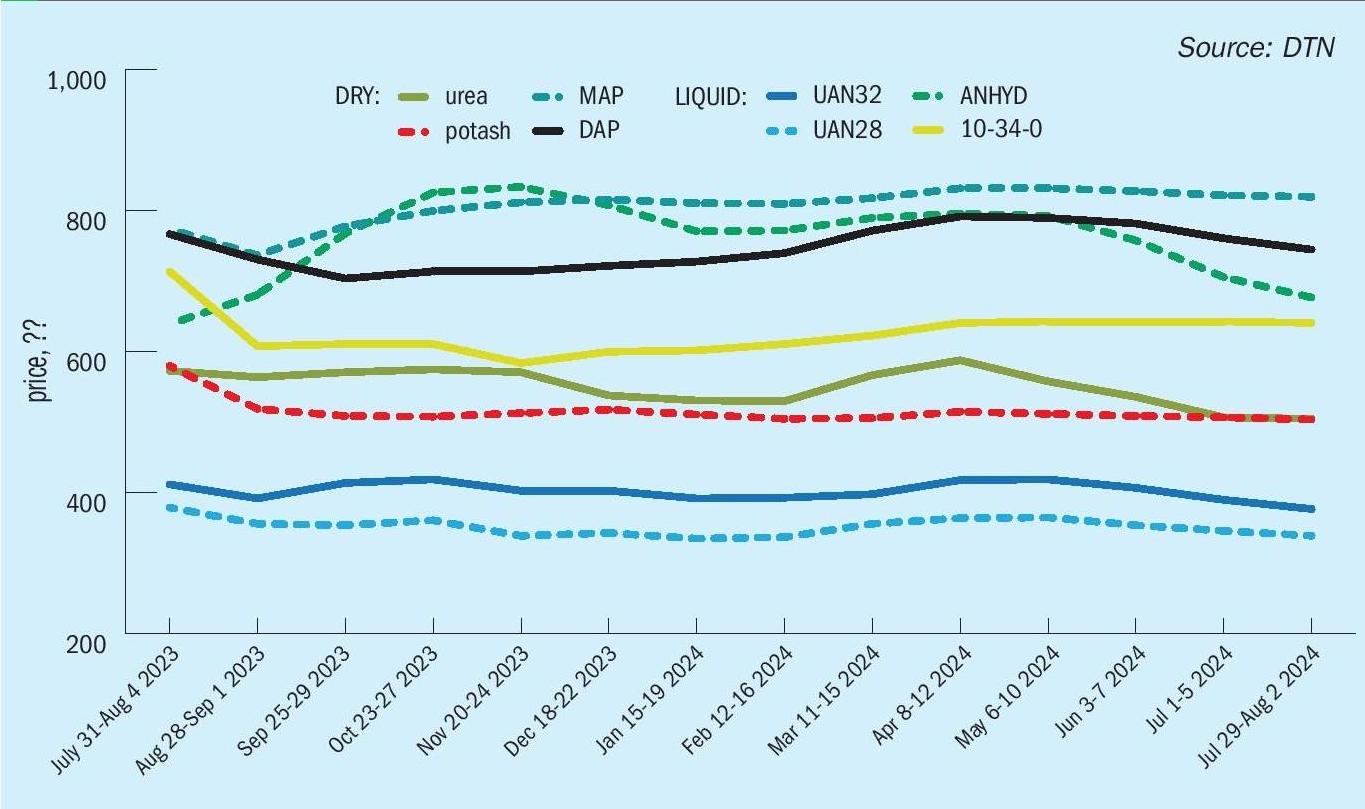

“US ag retailers have generally reported slight year-on-year declines in the prices of both solid and liquid fertilizers so far in 2024″

The US produced 5.4 million tonnes of DAP/MAP in 2022 and is the world’s fifth largest DAP/MAP exporter (2.8 million tonnes). Major destinations include Canada, Brazil and Argentina. While remaining a next exporter, the country was also ranked as the six largest DAP/MAP importing nation globally in 2022 (1.3 million tonnes), sourcing products from Saudi Arabia, Russia and Australia.

Slight price falls

In general, average US weekly retail fertilizer prices have fallen slightly, according to the DTN Fertilizer Index, a longstanding price indicator based on a basket of four solid and four liquid products.

Six out of the eight products monitored by DTN have fallen in price over the last 12 months (Figure 13).

US ag retailers have typically reported year-on-year (y-o-y) declines in both solid and liquid fertilizers to DTN. For example, as of early August 2024:

- Potash is 13 percent lower

- Urea is 12 percent lower

- Diammonium phosphate (DAP) is three percent lower

- 10-34-0 is 10 percent lower

- Urea ammonium nitrate (UAN 28) is 11 percent lower

- Urea ammonium nitrate (UAN 32) is nine percent lower.

Monoammonium phosphate (MAP) and anhydrous ammonia were the exceptions with their prices both six percent higher y-o-y.

Sharp price falls in the first half of 2023 improved fertilizer affordability in the US, ending a trend of rising prices in 2021 and elevated prices in 2022.

References