Nitrogen+Syngas 388 Mar-Apr 2024

31 March 2024

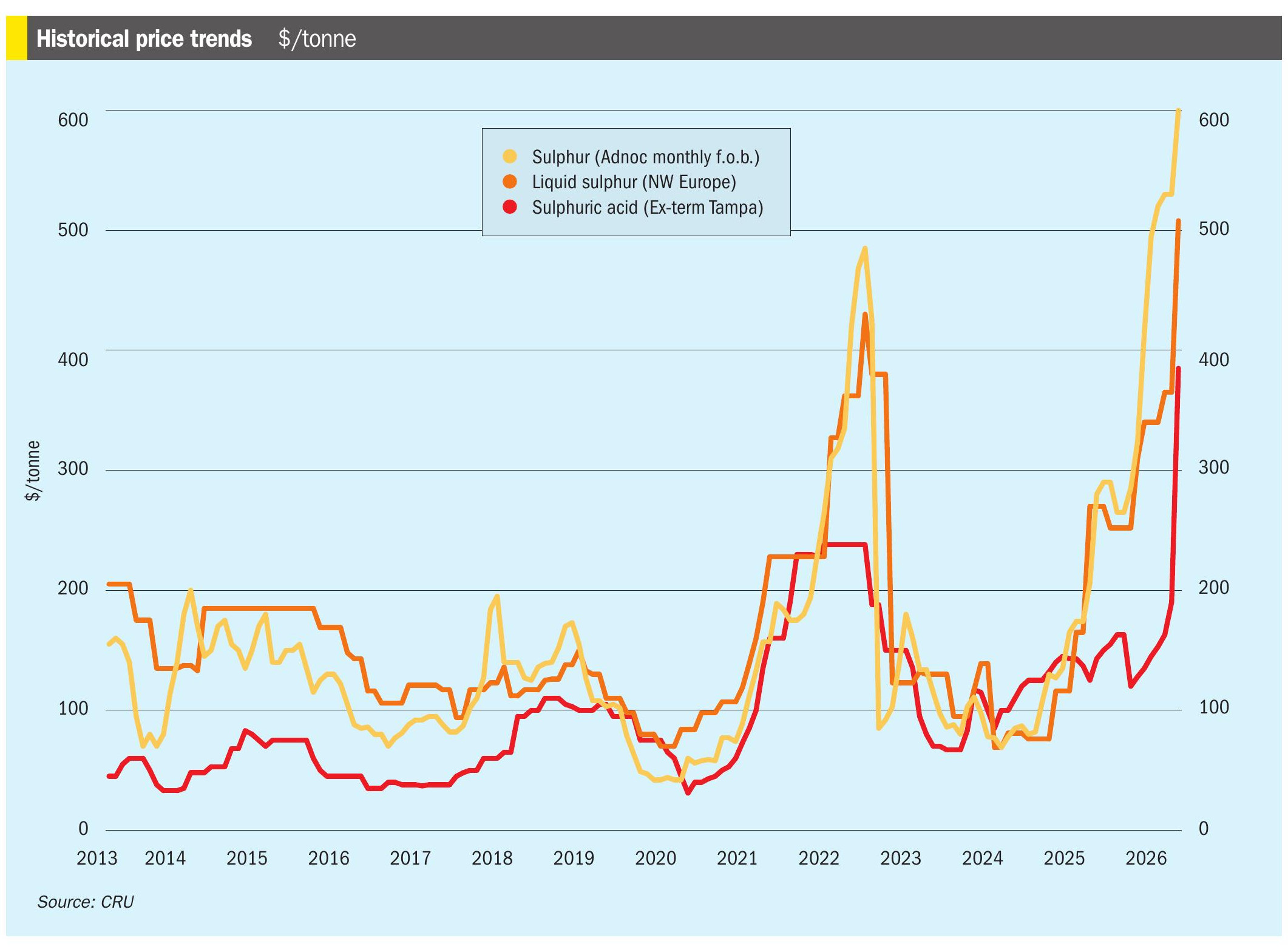

Price Trends

Price Trends

Ammonia pricing in the US Mid-West stood at $625/st f.o.b. in February, with applications to field continuing to ramp up. Prices in the US Gulf remain pegged in the low-to-mid$400s/t f.o.b. Recent production outages in the region have largely subsided, though an unexpectedly early uptick in seasonal demand from local buyers is likely to provide a degree of price support moving forward. The Tampa ammonia settlement for March has been settled by Yara and Mosaic at a $445/t c.fr rollover, largely in line with market expectations. The North American market remains detached from the considerably more oversupplied global ammonia scene.

Spot prices in NW Europe fell to around $465-470/t c.fr. With month-ahead natural-gas prices at the Dutch TTF hub trading as low as $8/MMBtu, theoretical ammonia costs of production continue to fall, to the low-to-mid-$300s/t region, well below latest import prices.

In North Africa, phosphate major OCP continued to source ammonia via a variety of spot and contract shipments. Jordanian phosphate producer JPMC was also in the market for a March ammonia cargo. Middle East ammonia activity was constrained, with producers largely focusing on contractual commitments. In Saudi Arabia, Ma’aden reported netbacks on its latest contractual shipments around the $295/t f.o.b mark.

Far East markets were quiet, with contract prices remain pegged at $300-350/t c.fr, though Chinese imports could soon begin to pick up to feed downstream fertilizer production.

CRU’s crop price index has declined to 120, its lowest level since September 2020, as strong supply continues to outweigh lackluster demand. The latest round of US and European Union (EU) sanctions on Russia do not include measures against the agricultural sector, despite concern this week among many in the industry that new measures against Russian fertilizers would be implemented as part of the package. Nitrogen production costs have been volatile over the past three years. The cost curve dramatically steepened in 2021 and 2022 as European gas prices ballooned. But markets have since stabilised.

In the US, granular urea barge prices kept climbing with rumours of shortages for the spring spurring buyers despite corn prices taking a turn for the worse. Sentiment remained positive with good volume and early spring weather in the north also supporting the market.

Baltic prices were stable with support coming from increases seen in granular markets such as Brazil and the US. Prices are suggested at around $300-310/t f.o.b. Granular demand is also fairly thin with northern Europe quiet, Brazil picking up just small quantities and Mexican interest for forward shipments yet to translate into firm enquiries/sales.

In China, unlike phosphates, there is no clear indication when urea exports will resume. The market is not expecting exports to restart before 1 May. Because of the adverse weather across the country, urea demand has been limited. Prices declined in mid February, but rebounded slightly from 27 February.

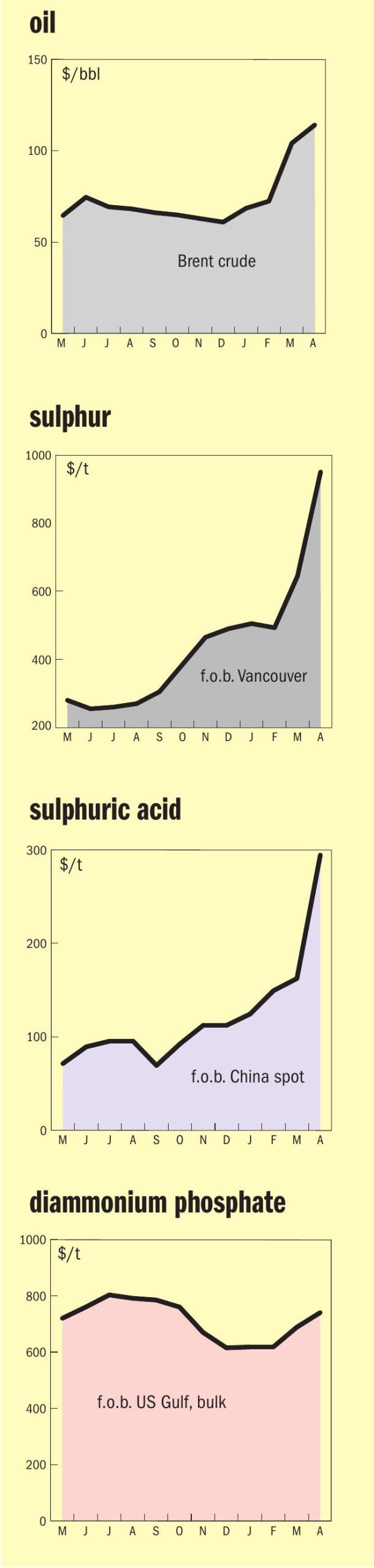

END OF MONTH SPOT PRICES

natural gas

ammonia

urea

diammonium phosphate