Nitrogen+Syngas 400 Mar-Apr 2026

17 March 2026

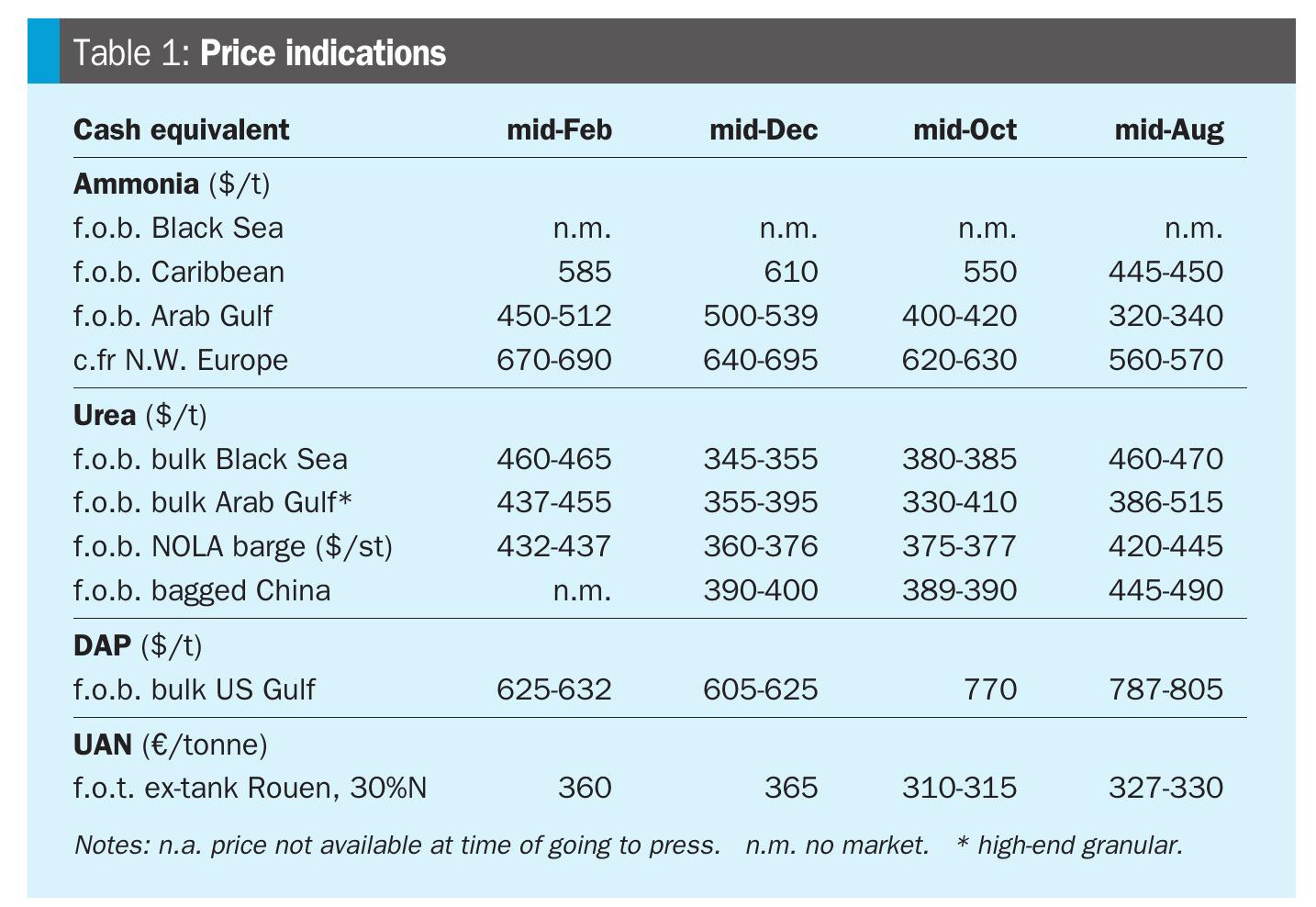

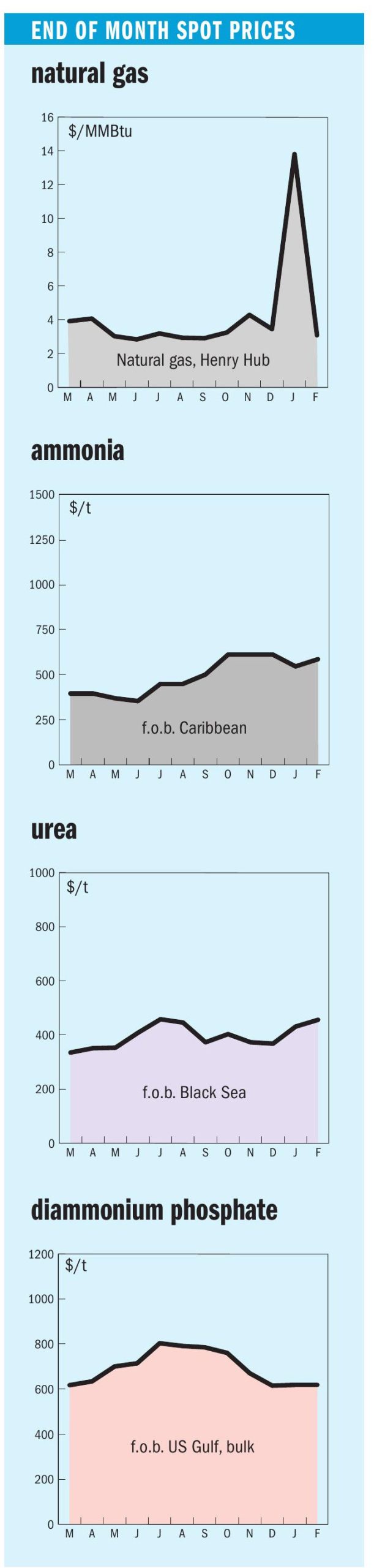

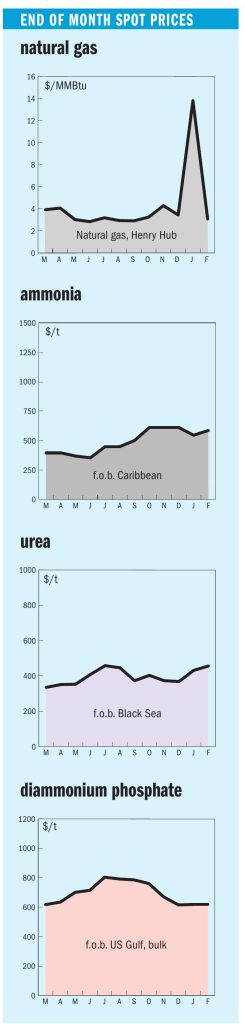

Price Trends

Price Trends

Ammonia sentiment was overtaken this week by the escalating Middle East conflict and the effective closure of the Strait of Hormuz, which left vessels unable to enter or exit the Arabian Gulf. With maritime trade frozen, price indications for prompt Middle East business largely stalled. In normal conditions, the sudden removal of Gulf export flows would point to sharply higher prices, particularly given the already-tight global availability and surging urea values, but participants said the absence of tradable cargoes made it difficult to pin down an indication. The immediate knock-on was felt East of Suez, where the supply shock pulled southeast Asian values back up to around $470-480/t f.o.b. The prevailing length in the market has been reportedly absorbed, with buying interest strongest from east Asia and India.

India is notably exposed to Middle East and Iranian supply. While demand is currently muted as turnaround period persists, a prolonged disruption would leave importers with few prompt alternatives once demand returns.

West of Suez was already facing tight supply and the tightness was further exacerbated by the conflict in the Middle East. Fertiglobe reported a 15,000 t sale at $750/t c.fr for mid-March delivery, $70/t higher from last week’s assessed average. LAT Nitrogen reported it would reduce ammonia operating rates at sites in France and Austria, presumably linked to the sharp rise in European energy costs; Dutch TTF hub prices have surged to a three-year high.

The urea market attention has also been dominated by the fallout from US intervention in Iran and the subsequent regional conflict that has sent prices soaring and severely disrupted trade flows from the Middle East. In Iran, market visibility was lacking following an internet blackout, with no fresh transactions heard and the operational status of its producers unclear. The wider Middle East saw activity draw to a halt as Iranian threats to shipping effectively closed the Strait of Hormuz. This disruption was highlighted by QatarEnergy’s decision to halt all urea production at its Mesaieed complex following strikes on its facilities, leaving several loaded vessels for destinations including India and Brazil stranded within the Arab Gulf. West of Suez, the supply shock from the Middle East sent prices spiralling upwards as traders scrambled to secure alternative tonnage. In Algeria, at least 150,000 t granular urea was sold, with AOA eventually concluding business for April loading at $680/t f.o.b., a level not seen since October 2022. Egyptian producers capped a similarly relentless week of business with Mopco eventually placing granular at $665/t f.o.b. for March shipment to Europe, a level also not seen since 2022 Q4. The bullish sentiment was mirrored in Nigeria, where Dangote sold 30,000 tonnes granular at $665/t f.o.b. for April, a jump of $210/t on business concluded in early February.

In the Americas, the NOLA market experienced a volatile week of trading. Strong demand for the upcoming spring season, coupled with global supply fears, pushed March barges to a new high of $620/st f.o.b., before easing slightly.