Market Insight

Market Insight courtesy of Argus Media

Market Insight courtesy of Argus Media

Market Insight courtesy of Argus Media

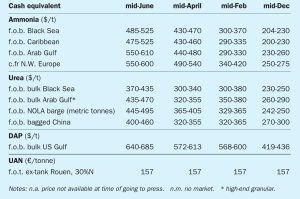

Ammonia markets continue to be dominated by unplanned outages in Saudi Arabia (where the SAFCO 4 and one of the Ma’aden ammonia plants are both down, removing 2.3 million t/a of merchant ammonia from the market). This comes on top of other shutdowns earlier in the year on Trinidad, in the US and Australia.

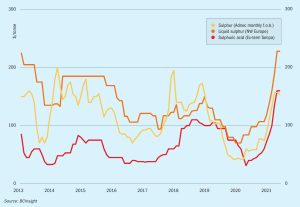

Meena Chauhan , Head of Sulphur and Sulphuric Acid Research, Argus Media, assesses price trends and the market outlook for sulphur.

With demand for conventional fuels projected to peak and fall over the next decade, some refiners are looking to petrochemical production as a way of diversifying their product slate.

Commodity markets are often volatile, and sulphur and sulphuric acid can be more so than most, with much of their supply coming from involuntary production, and sulphur supply in particular often dependent on the timing of large scale oil and gas projects. Even so, this year’s price rises, in some cases tripling in just over a year, have been especially eye-catching.

Significant capacity additions in the Middle East are still awaited. The more positive outlook for fuel demand is providing support to seeing these projects ramp up in the coming months. New supply is expected from Saudi Arabia following the commissioning of a gas project in 2020, sulphur availability is likely to improve from the country through the second half of 2021 and into 2022 as a result.

More than 560 delegates participated in CRU’s Phosphates 2021 Virtual Conference, 23-25 March 2021. To highlight this successful event, we report on keynote and selected commercial and technical presentations.

Market Insight courtesy of Argus Media

February saw ammonia prices jump due to a series of plant outages, including EBIC in Egypt, and several plants in North America, including two on Trinidad; the 760,000 t/a Nutrien 4 plant and 500,000 t/a Tringen 2 plant, both due to gas shortages, as well as Yara and BASF’s 750,000 t/a unit at Freeport, Texas.