Sulphur 391 Nov-Dec 2020

30 November 2020

Price Trends

MARKET INSIGHT

Matt Langworthy, Analyst for Argus Media, assesses price trends and the market outlook for sulphur.

SULPHUR

As we approach the end of the year, we have seen fourth quarter sulphur contract prices firm. Contract settlements followed a rally in spot prices towards the end of the third quarter as supply tightens heading into winter. The ongoing pandemic has only exacerbated this tightening as run-rate cuts at refineries, mainly to the west of the Suez, restricts sulphur output. And because of these cuts, supply has been particularly tight in North America, India, the Mediterranean and Western Europe. Many of these regions are now experiencing a second wave of coronavirus infections and re-entering lockdowns, so industry slowdowns and production cuts are expected to persist into early next year. But many consumers have now secured product for the year, leaving little demand in the market for the remainder of 2020, which will leave liquidity thin and lessen the influence of tight supply on pricing.

Middle East fourth quarter contracts have followed the slight increase seen elsewhere. And in the spot market, little availability is expected with product from the region prioritised for contracts, although spot activity is expected to continue the rise seen towards the end of the third quarter as some key off-takers have reduced their deliveries. Yet, with low levels of prompt demand as the year comes to a close, Middle East f.o.b. prices will soften.

After weeks of stagnation in the Chinese import market, we have seen granular prices firm a little to $92-95/t c.fr as demand from the phosphate market remains strong. But as expected, southern Chinese consumers have favoured discounted Iranian shipments, not typically included in price assessments. One buyer reportedly took delivery of 31,000 t of granular product from Bandar Iman Khomeini which settled in the mid-$80s/t c.fr China. In the Chinese molten sulphur market, 2021 supply contract negotiations have begun but in the spot market supply has held tight keeping prices firm at around $60/t c.fr. Import quantities have been low this year as refineries faced production cuts. South Korea’s capacity additions were expected to boost Chinese imports of molten product, however operating rates across South Korean refineries remained low amid strict lockdowns and poor refining margins globally.

China’s sulphur inventories rose to over 3.0 million tonnes at the start of the year as domestic consumers shut down as coronavirus lockdowns took hold across the country. Consumers in the country swiftly recovered into the second-half of the year, but port inventories remained high and were at 2.9 million tonnes at the end of October, up 38% over the same period as in 2019. And because of the influence of the pandemic and high inventory levels, as expected, imports have fallen 23% to 6.6 million tonnes in the first three quarters of this year relative to the same period in 2019. This reduction in imports has set the trend for the long-term trade outlook in China especially as investment into the refining sector across the country will increase sulphur capacity by around 45% as just under 5.0 million tonnes of oil-based sulphur capacity comes online by 2024. As domestic supply increases, and demand growth in the region is expected to remain limited, import volumes are expected to drop below 9.0 million tonnes/a within the next three years. Import volumes at this level have not been seen since the late 2000s. China is forecast to lose its spot as the leading global importer of sulphur in 2022, particularly as Moroccan fertilizer producer OCP’s phosphate operations ramp up sulphur import demand.

In North America, prices have held steady as supply remains tight. Vancouver export prices rallied slightly heading into the start of November, increasing to $66-73/t f.o.b. as demand continues to recover in Asia. But, supply tightness is expected to ease as Heartland Sulphur begins moving new granulated sulphur from its expanded capacity at their Fort Saskatchewan terminal. At the end of October, Heartland successfully began operating its second 2,000 t/d forming unit, doubling forming capacity at the terminal. The terminal now has an estimated forming capacity of 1.4 million t/a.

This is the first of four new Canadian forming projects in the pipeline. Keyera and Enbridge plan to bring 4,400 t/d of forming capacity online at the existing South Cheecham Terminal in 2022, although production has yet to commence. Just a few kilometres to the north-west of South Ceecham, H.J. Baker Sulphur Canada is also planning a 4,000 t/d former. The latter was originally slated for start-up in the fourth quarter of this year but we have yet to see any project updates. Lastly, Sulphur Midstream is planning a 2,000 t/d former in Edmonton. Few details are known about the plant and we consider it to be speculative at this time.

Increased forming capacity will likely see Vancouver exports rise in the midterm although molten exports to the US are expected to hold firm whilst demand remains strong and pricing attractive. Inventories in the US have been depleted as Covid-19 related refinery production cuts have contracted sulphur output. According to USGS data, sulphur production from January to August this year fell 350,000 t on the same period in 2019, corresponding to 6% reduction. Whilst higher production cuts were expected based on the decline in refinery utilisation rates, the increased use of imported heavy Saudi crude feedstock this year has mitigated some of the decline in production this year.

Fourth quarter prices in the US settled slightly up on the previous quarter, although very little, if any product is expected to ship. US Gulf export prices are remaining steady at $62-73/t as spot market activity remains very limited. Further refinery production cuts from Hurricane Laura in August compounded tight supply already present from the coronavirus pandemic. But, as capacity begins to be reintroduced to the market, we are expecting export volumes from the Gulf to increase towards the end of the year. Citgo had been operating its 425,000 bbl/d refinery in Lake Charles at a reduced rate since it sustained damage from the hurricane but confirmed at the end of October normal operating rates have resumed.

New sulphur capacity in North America is limited to CNRL’s oil sands expansions at Horizon in Canada. The expansion is expected to complete next year, increasing Horizon’s capacity by 280,000 t/a since works began in 2015. Despite this, North American production is anticipated to decline in the long-term as Canadian gas reserves dwindle and US production is forecast to remain stable. Also, the country’s tendency to favour sweeter crudes in recent years is expected to continue.

Already, this shift to lower sulphur-containing feedstock has seen sulphur production fall to 66% of oil-based capacity over the past five years – a level expected to hold steady into the long-term. At the time of writing, the results of the US election were uncertain, but a Biden administration could likely impact future production with the potential incumbent less supportive of the oil and gas sector.

SULPHURIC ACID

The East/West price divide which peaked early this year is still present with export prices in north-east Asia remaining in negative territory. Ample supply from Asian markets and demand still dampened by the coronavirus has slowed a price recovery in the region. But northwest Europe prices firmed quicker and climbed back into positive territory as we entered the third quarter. Fourth quarter contracts are progressing although sentiment from the industrial demand-side remains uncertain with ongoing lockdown restrictions.

In Morocco, OCP suspended berthing operations at Jorf Lasfar at the end of October as bad weather moved into the region but the fertilizer producer is expected to increase acid imports by just under 9% this year. OCP typically produces most of its sulphuric acid requirements from sulphur burners, however it has been and will continue to capitalise on cheap acid imports. Looking further ahead, Moroccan sulphuric acid demand is expected to grow 46% from 2019 to 2025 but imports are expected to hold steady over this period at around 1.6 million t/a – slightly under the 1.7 million t/a of imports we expect this year. Much of the demand growth will be met by increased sulphur burner capacity. With no domestic sulphur production, OCP relies entirely on the import market for its sulphur needs.

Indian demand is continuing to increase as phosphate fertilizer producers seek tonnes. Vedanta’s ongoing battle with the Tamil Nadu state to restart their Tuticorin smelter continues to place uncertainty on the long-term acid outlook for the country especially as with years of no maintenance, a restart is beginning to look less certain. Vedanta appears to be exploring alternative options with plans to construct a new zinc smelter in Gujarat. Few details are known at this time but a post-2022 start-up is most likely considering the early stage of the project.

In China, export prices are remaining firm in the negative $8/t to negative $1/t f.o.b. range. Sellers are targeting positive f.o.b. prices although these remain well above workable c.fr prices. Netbacks from the domestic market are proving to be favourable with prices steadily rising over the past few weeks. Prices in Guizhou rose to Rmb 260-300/t delivered whilst prices remained steady at Rmb 310-340/t delivered in Yunnan. In the first nine months of the year, acid exports from China have fallen 12% to 1.4 million tonnes on the year. This fall came after the semi-withdrawal of the 2.3 million t/a capacity Two Lions burner in Zhangjiagang and a major decrease in demand from Chile as the copper industry contracted. We expect total acid production in China to decline to 93.7 million tonnes this year – a 2.9 million t/a drop on 2019. With a major portion of this loss attributed to burner capacity, smelter-based capacity is expected to become the leading source of acid production this year. Looking ahead, Chinese acid production will increase as new smelter projects come online. Notable additions include Houman North Copper in Shanzi which will enter production in 2023, adding 1.3 million t/a of capacity.

Prices in Chile have recovered from their lows in June to rise to $40/t c.fr on a spot basis in recent weeks. Talk of annual contracts settling in the mid-$50s/t c.fr is the current market sentiment but prices above and below this are also possible.

In Australia, First Quantum’s Ravensthorpe nickel mine continues to operate after a successful restart earlier this year. The associated HPAL plant consumes acid produced from an onsite burner. Nickel-based demand across the Asia-Pacific region is expected to rise with several new HPAL projects due to come online in Indonesia. The series of new projects come as nickel demand from the battery sector is expected to surge over the next decade. We expect 2.3 million t/a of new nickel-based consumption from Indonesia by 2024 – the majority of which will be met by burner capacity as opposed to acid imports.

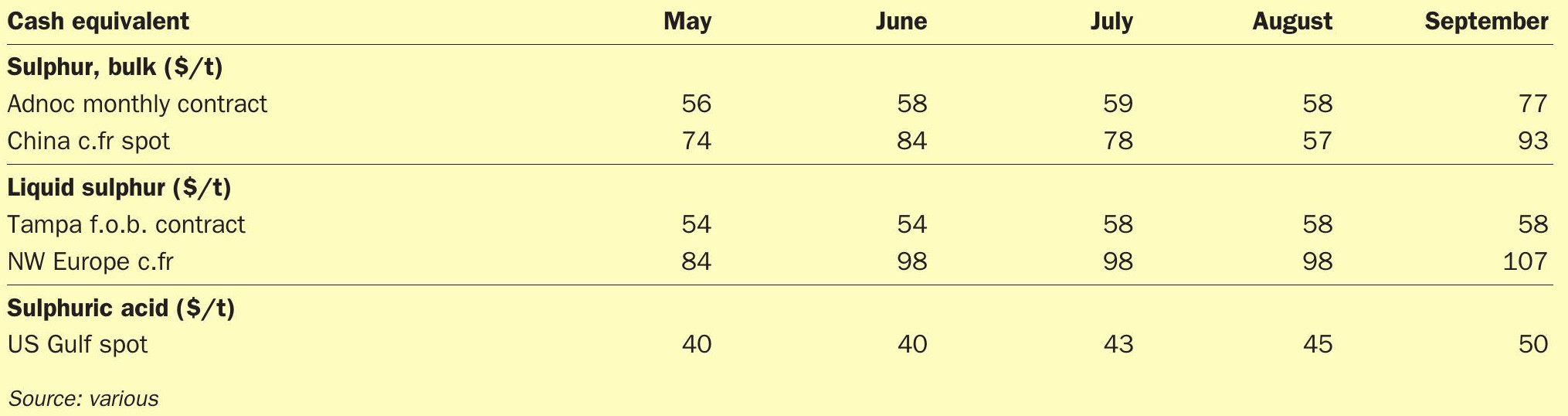

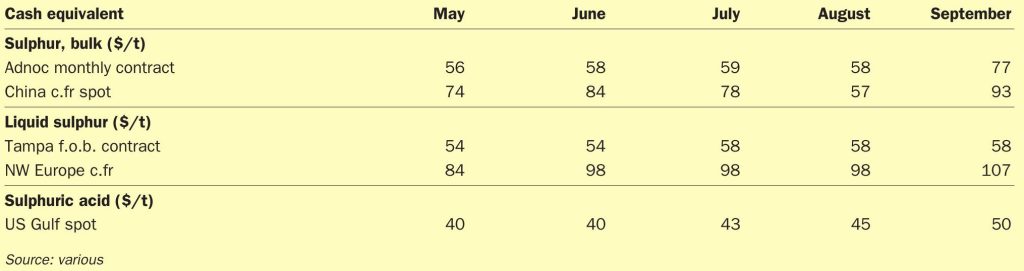

PRICE INDICATIONS