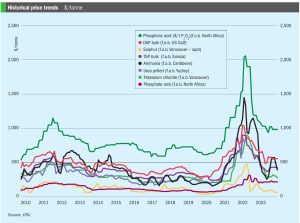

Market Insight

Market as of 20th June 2024. Urea: Prices remain stable while the market awaits clear price direction on whether to hold current f.o.b. levels or to push higher.

Market as of 20th June 2024. Urea: Prices remain stable while the market awaits clear price direction on whether to hold current f.o.b. levels or to push higher.

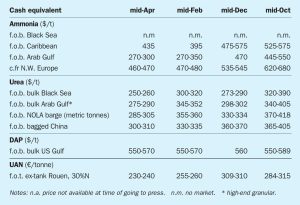

Urea: Prices continued their global decline in mid-April, including at New Orleans. The notable exception was Brazil where prices firmed due to buyer interest in the market for May and beyond.

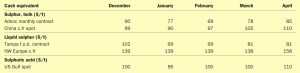

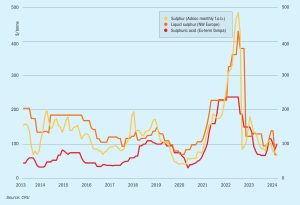

Sulphur benchmarks firmed around the globe in April. Although availability remains ample, downstream production is expected to rise in the weeks ahead and further upside for prices is expected, at least in the short term. Prices increased the Middle East, Indonesia, India, Brazil, and the Mediterranean. The Middle East spot price was assessed up an average $3/t at $83-88/t f.o.b. The previous low end of the range was no longer considered achievable. The price has climbed 27% since mid-February this year. The benchmark is down 53% from early December 2022, but had climbed 47% from the end of July 2023 to its mid-October average of $110/t f.o.b. before declines set in once again. Chinese buyers returned to the international spot market in late April following weeks of inactivity, lifting c.fr prices.

Downstream phosphate production is expected to climb, with further sulphur price recovery expected. Overall, global demand remains lacklustre as downstream demand has yet to increase substantially in key markets and sulphur availability from most origins is ample.

The ammonia market reverted to recent norms at the end of April, with prices more or less unchanged in the east, and several benchmarks west of Suez moving downward in line with May’s Tampa settlement. Following a trio of high-priced c.fr spot deals many wondered whether such business would be replicated in Asia, but the hype did not live up to the expectation, with the majority of tonnes continuing to move on a contract basis into the likes of South Korea and Taiwan, China. The $430/t c.fr concluded into China has been attributed to both supply uncertainty and an uptick in domestic demand, though several inland prices declined this week, rendering price direction difficult.

Although it has been a major exporter of urea, increasing Chinese government restrictions have restricted the seasonal window for exports.

Prices in the West are unlikely to garner much support moving into the latter stages of Q2. The May Tampa ammonia settlement was settled by Yara and Mosaic at $450/t c.fr, down $25/t on the $475/t c.fr agreed for April. With seasonal domestic demand in the US drawing to a close 2H April, many had anticipated that either a rollover or a slight decline would be agreed.

Sulphur prices reached a low point in mid-February, with buyers looking to the tender from Muntajat as well as the return of Chinese buyers following the Lunar New Year holiday for the direction that the market would turn. CMOC’s 5 February tender for 40,000 tonnes of sulphur for early-April arrival was indicated awarded in the upper $90s/t c.fr on supply from the FSU, though details were not confirmed.

CRU expects sulphur prices to be supressed in early 2024 by high port inventory and limited phosphate export business. However, affordability continues to support raw materials purchases and leaves room for price increases, especially if downstream production picks up as expected and sulphur stock drawdown slows.

Urea. As February ended, urea prices found support in the US and Brazil while Europe remained subdued and Egypt struggled to find buyers. New Orleans was the one bright spot in the urea market – with NOLA prices benefitting from the meeting of suppliers and buyers at the TFI’s domestic conference. With positive sentiment all round, prices moved up $30/st, peaking at $390/st f.o.b. for March.