Market Insight

Price trends and market outlook, 7th May 2026.

Price trends and market outlook, 7th May 2026.

• Prices are expected to hold at historically high levels as long as the Strait of Hormuz remains effectively closed. If the situation persists, further price increases are likely, which will only intensify the affordability crisis for global consumers.

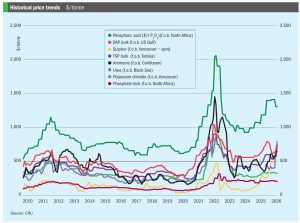

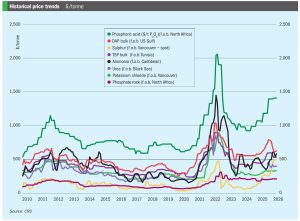

Sulphur continued to break historic records in most key international markets at the start of May as the scarcity of spot supply propelled prices higher, which triggered production cuts at some downstream markets, and increased costs in other industrial sectors. The effective blockade of the Strait of Hormuz, which halted the flow of Middle East supply, has forced desperate buyers to compete for the limited available spot cargoes, primarily from North America. Although fresh transactions were limited, export and delivered prices climbed higher, and market sentiment remained jittery. QatarEnergy hiked its sulphur price to $740/t f.o.b., a new record high for this contract since its inception in August 2013.

• Short-term outlook: Ammonia benchmarks are expected to remain under upward pressure. The PAU turnaround removes a key supply source from an already tight SE Asian market.

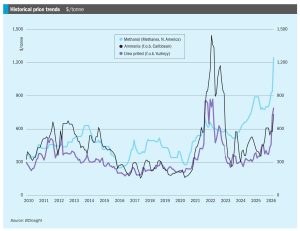

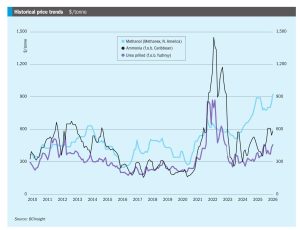

Global ammonia benchmarks pushed to fresh highs in April, with a reported trade from Egypt to NW Europe at $905/t c.fr, marking the highest Atlantic level seen since the Middle East conflict began. The move was driven primarily by tightening North African supply, with Algerian offer levels climbing to $840-850/t f.o.b., and Egyptian availability constrained by EBIC being sold out through June, together with limited prompt tonnage from Abu Qir.

The US and Israel attacks on Iran and the Iranian response have thrown commodity markets into chaos, with sulphur and sulphuric acid particularly affected.

• Market sentiment has shifted decisively from bearish to bullish as the conflict in the Middle East has triggers a significant price rally.

Conflict in the Middle East has halted all vessel traffic through the Strait of Hormuz, effectively paralysing a region that accounts for 48% of global seaborne sulphur trade. As a result, the sulphur spot market has ground to a halt, with prices notionally holding unchanged in the $490-515/t f.o.b. range simply due to a lack of activity. No spot offers were reported out of the Middle East.

Price trends and market outlook, 26th February 2026. (Important note: this Market Insight was published two days before the start of the latest Middle East conflict.)

• Prices are likely to remain on an upward trajectory as long as the Strait of Hormuz remains effectively closed and Middle East export availability is constrained.