Fertilizer International 527 Jul-Aug 2025

7 July 2025

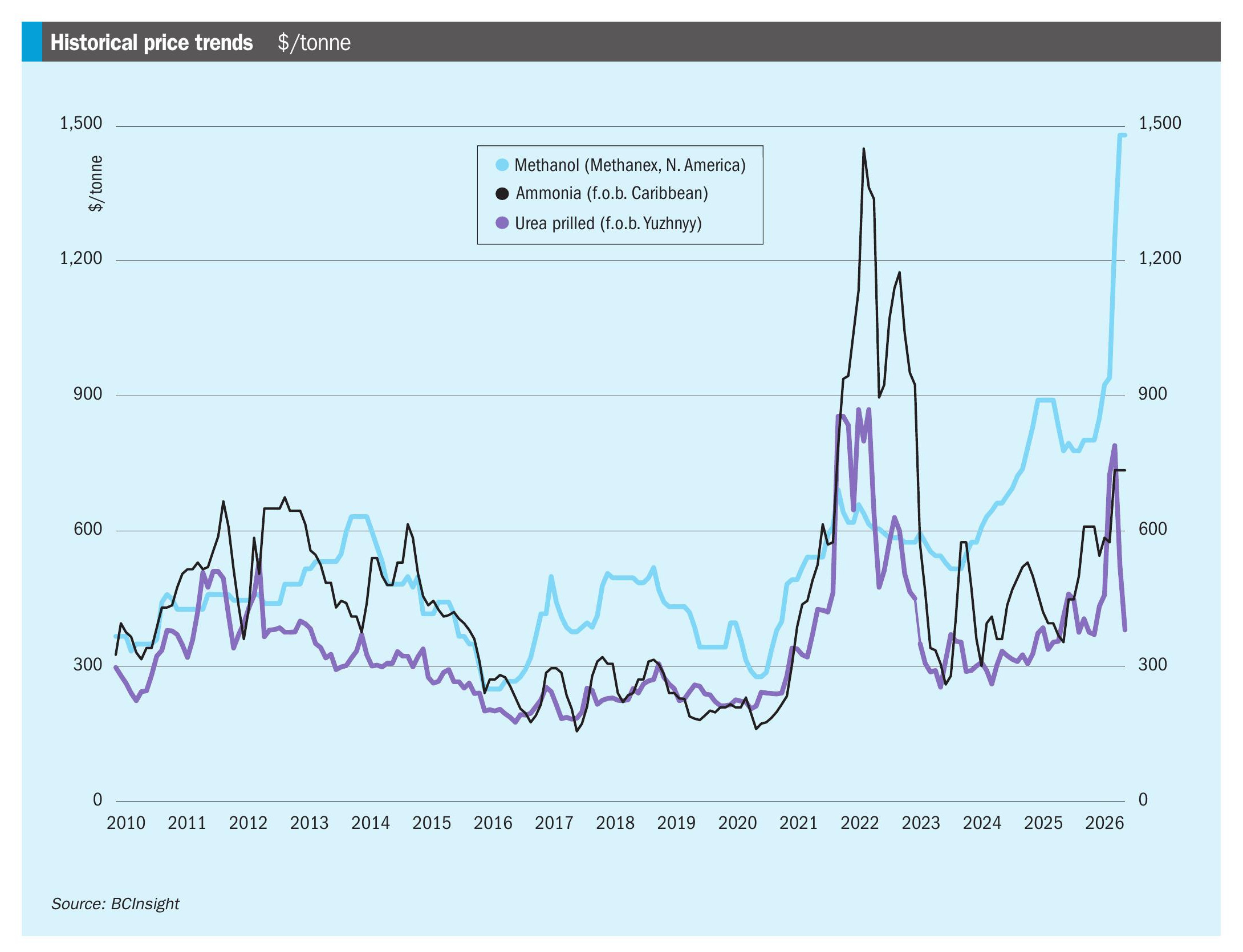

Urea market on edge

The 12-day Iran-Israel conflict in mid-June placed the urea market on edge. Having experienced price volatility throughout the year, the market faced the prospect of a global supply crunch prior to a ceasefire agreement.

Generally, urea prices this year have remained elevated compared to 2024, with Middle East prices, for example, averaging around $55/t higher in the year to date. The market has been on a rollercoaster too. Factors such as on/off US tariffs (Fertilizer International 526, p7) and the proposed imposition of EU tariffs on Russia (Fertilizer International 525, p7), alongside production outages, hand-to-mouth buying, as well as the lack of clarity on Chinese exports, have all contributed to urea price volatility.

Amid early signs of global price easing, Israel’s surprise attack on Iran on 13th June upended urea market sentiment and spurred buying activity. Urea prices in Middle East, Algeria, Brazil and NOLA all jumped by $50-110/t in a week – with prices in Algeria hitting $520/t f.o.b.

In this 19th June CRU Insight, Pranshi Goyal and Charlie Stephen address three key questions – what is the status of the global urea market, what supply sources are at risk and how could their absence affect short-term urea pricing?

Supply disruptions could be severe

Iran operates 8.7 million tonnes of annual capacity from seven urea plants located in the west of the country. The country shut all its urea-ammonia production facilities on 16th June, following Iranian government safety guidance issued in the face of ongoing attacks by Israel, this translating to a loss of around 700,000 tonnes of monthly production. The complete shutdown, although said to be unrelated, came after the attack by Israel on Iranian natural-gas facilities on 14th June.

While the destinations for Iranian urea are limited, Iran remains an important supplier for both Brazil and Turkey. The country exported close to three million tonnes of urea in the second half of last year – volumes that are now at risk depending on the duration of the conflict.

Gas cuts hit Egypt’s output

Production in Egypt has been facing challenges during summer months as gas is drawn away from fertilizer producers to meet domestic requirements for cooling. Mirroring the events in 20232024, Egyptian producers were forced to curtail urea production for a few weeks in May this year. Having just resumed operations in early June, the escalation of the conflict halted gas supply from Israel to Egypt on 13th June, triggering a fresh a wave of plant shutdowns.

Egypt’s urea production amounts to approximately 7.7 million tonnes annually, predominantly serving the European and Turkish markets. Consequently, a disruption resulting in the loss of around 600,000 tonnes of monthly production from Egypt would precipitate an immediate supply shortfall across the region.

Two Russian sites hit by Ukraine

Unrelated to the ongoing Middle East tensions, recent drone attacks by Ukrainian forces on the EuroChem-operated Novomoskovsk Azot (1.6 million t/a of urea capacity) and Nevinnomyssky Azot (1.0 million t/a of urea capacity) production complexes – in Russia’s Tula region and the Stavropol Territory, respectively – are expected to significantly impact urea and nitrates availability from Russia. While the full extent of the damage is still under assessment, both sites collectively represent 20% of Russia’s total production capacity and are understood to be offline currently. This development coincides with the period of limited Russian supply due to summer maintenance turnarounds, resulting in an additional reduction of roughly 200,000 tonnes of monthly urea production.

In summary, the 12-day Iran-Israel conflict affected global supply dynamics for urea, and risked export losses of around:

• 600,000 tonnes from Iran,

• 450,000 tonnes from Egypt,

• 200,000 tonnes from Russia.

While this offered China a burgeoning opportunity to ramp up exports and plug the gap, the Chinese government’s restrictive export policy and the exclusion of exports to India made this unlikely, in CRU’s view.

Impact of supply shock on demand

India is currently the key driver in the market and is set to enter the seasonal Kharif demand period (July–September) and undertake a significant stock replenishment. A recent tender by NFL was scheduled to close on 16th June 2025, unfortunately coinciding with the escalation of the Middle Eastern conflict. Despite seeking 1.5 million tonnes of urea for West Coast India, a swift run up in urea prices meant NFL was unable to garner any acceptances except for 229,000 tonnes at an offer of $399/t cfr.

Any disruption to Middle Eastern supply is particularly concerning for India as the region is one of the subcontinent’s top urea suppliers, supplying three-quarters of total imports in 2024, a situation that is further pressured by limits on Russian product availability (17% share of total imports). India will need to import approximately four million tonnes of urea through tenders during the second half of 2025 to meet domestic demand while maintaining year-end closing stocks.

Ceasefire?

With characteristic showmanship, the Middle East woke on 24th June to an overnight social media announcement of an Israel-Iran ceasefire by US President Trump. The term of this truce, exactly how it had been brokered and its likely permanency were all unclear as Fertilizer International went to press.