Price Trends

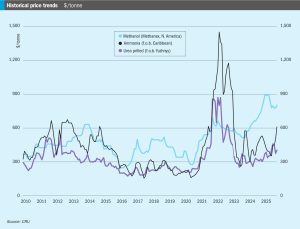

Ammonia sentiment was overtaken this week by the escalating Middle East conflict and the effective closure of the Strait of Hormuz, which left vessels unable to enter or exit the Arabian Gulf. With maritime trade frozen, price indications for prompt Middle East business largely stalled. In normal conditions, the sudden removal of Gulf export flows would point to sharply higher prices, particularly given the already-tight global availability and surging urea values, but participants said the absence of tradable cargoes made it difficult to pin down an indication. The immediate knock-on was felt East of Suez, where the supply shock pulled southeast Asian values back up to around $470-480/t f.o.b. Prevailing length in the market has been reportedly absorbed, with buying interest strongest from east Asia and India.