Sulphur 423 Mar-Apr 2026

23 March 2026

Oil sands sulphur

OIL SANDS

Oil sands sulphur

With the decline of Venezuela’s production, Canada’s oil sands now represent 90% of all oil sands output, and a significant share of North America’s sulphur production.

Proven global oil deposits total around 1.75 trillion barrels. Of this, around one quarter (470 billion barrels) are accounted for by oil sands deposits. Aside from some deposits in Siberia and Kazakhstan, the majority of this is found in two huge areas; the Faja Petrolifera del Orinoco (Orinoco Petroleum Belt) along the Orinoco river in Venezuela, and a long series of deposits on the eastern side of the Rocky Mountains in northern Canada.

While oil sands deposits are extensive, and represent 96% of Canada’s and more than 90% of Venezuela’s proved reserves, they are less easy to extract than conventional oil. The heavy, bituminous oil is trapped in a sandy layer close to the surface, and requires considerable energy to be supplied to liquefy it and make it pumpable, and further processing to break it down into lighter fractions suitable for refinery use. This raises the cost of production and its energy intensity, making it a marginal play at times of low oil prices. Nevertheless, while oil sands production represents only about 4% of world oil output, because it has a high sulphur content (typically around 5%), it represents a correspondingly higher share of global sulphur production.

Venezuela

Venezuela’s oil sands reserves there are estimated at 300 billion barrels, representing 90% of Venezuela’s proven oil reserves and over 15% of all global oil reserves. Production expanded rapidly during the 1990s, the time of what was known as Venezuela’s ‘apertura’ (opening). Much of the exploitation was via western oil majors such as Chevron, BP, Total and Repsol-YPF. However, the accession of populist president Hugo Chavez in 1998 led to an abrupt about-face in policy and part-nationalisation of the Faja, which caused most western countries to back out. Over the next decade and a half, corruption and mismanagement by political appointees and lack of investment in maintenance, coupled with the effect of US sanctions, led to steadily falling oil production, and under Chavez’s successor Nicolas Maduro the decline has been even more marked, as Maduro purged the senior leadership of PDVSA and appointed his own political cronies. AS a result, Venezuelan oil production declined from 3.3 million bbl/d in 2000 to 650,000 bbl/d in 2021, with only 300,000 bbl/d coming from the Faja. Venezuelan sulphur output from oil sands production was estimated at just 30,000 tonnes in 2025.

The removal of Nicolas Maduro by the Trump administration leaves the future of Venezuela’s oil sands in something of a limbo. President Trump has tried to encourage US producers to invest in Venezuela and held out the prospect of a removal of sanctions for a more pliable regime in Caracas, but as yet US oil majors have been somewhat indifferent to the prospect, with easier and safer plays to be found elsewhere.

Canada

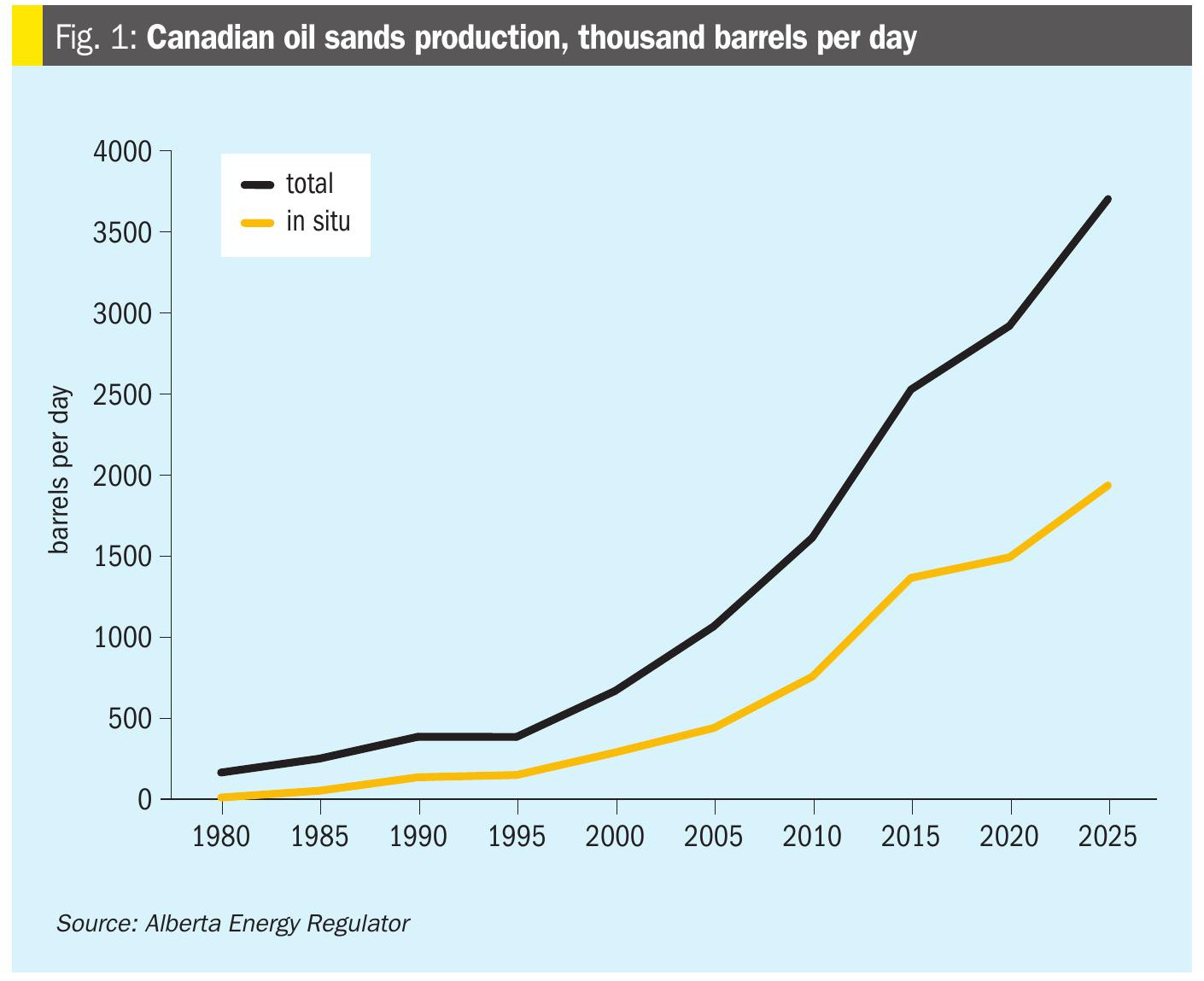

The story in Canada has been very different. Like Venezuela, Canada’s oil sands are in a remote and relatively inaccessible part of the country – in this case northern Alberta rather than the jungles of the Orinoco. The reserves are also of a similar size. However, Canada’s oil sands exploitation has a longer and happier history than Venezuela’s, and hence of the 5.3 million bbl/d of oil that Canada produced in 2025, about 4.1 million bbl/d or 75% was from oil sands production.

There are three major producing basins in Alberta: Peace River, in the northwest of the province, and Athabasca and Cold Lake, which run along the eastern border with Saskatchewan. Production is split between conventional, open pit mines, and ‘in-situ’ production, the latter of which pumps steam down into underground deposits to melt the bitumen and then draws it back out. This so-called steam assisted gravity drainage (SAGD) method is increasingly popular as it is not only cheaper but uses less water and avoids the large-scale scarring of the landscape of open pit mining, which must then be remediated once extraction is complete. The mined deposits cluster in the north of the Athabascan deposit, around Fort McMurray, where the deposits are less than 75m below the surface, with the SAGD projects running in a line south to Cold Lake.

The bitumen recovered is usually then either upgraded to produce synthetic crude oil (‘syncrude’), or diluted with lighter fractions such as naphtha to produce a ‘dilbit’ (dilute bitumen) or with syncrude to create a ‘synbit’. These are light enough to be pumped, and so can be exported by pipeline or rail. There are three major upgraders at Scotford, Redwater and Mildred Lake, with a total capacity of just over 1 million bbl/d. According to the Alberta Energy Regulator, roughly 25% of extracted bitumen is upgraded.

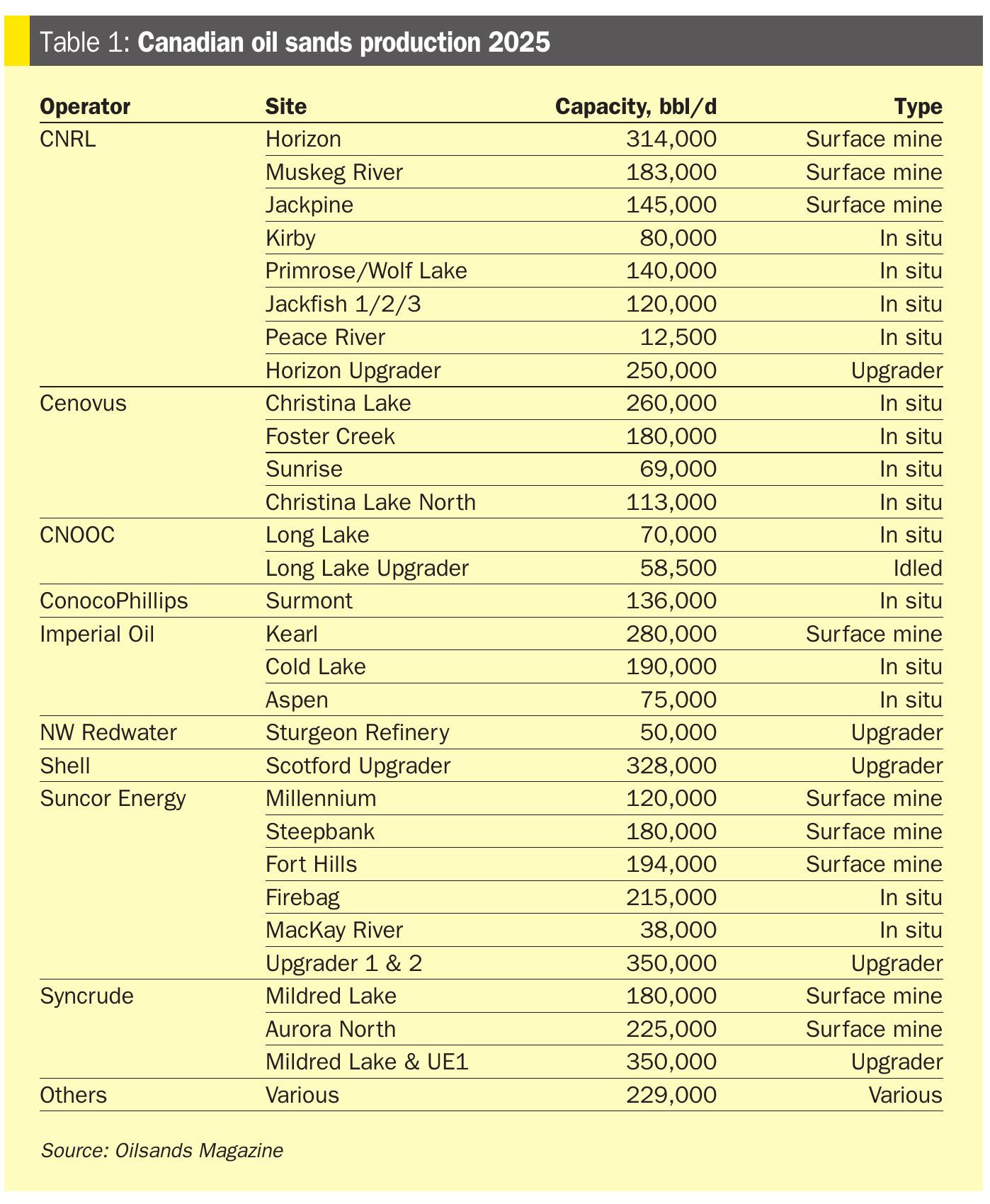

Table 1 shows current Alberta oil sands operations. The major operators are now Suncor, Cenovus, Canadian Natural Resources Ltd (CNRL), Syncrude and Imperial Oil. Some of the major oil companies such as Shell have moved out of oil sands production over the past decade (Shell retains only its Scotford upgrader) after a period of low oil prices in the late 2010s. Even so, production has continued to increase, as Figure 1 shows.

Exports

Canadian oil production from all sources ran at about 5.3 million barrels per day in 2025. Set against that, consumption totalled around 2.3 million barrels per day. The balance of 3.0 million bbl/d was exported, and by far the largest slice of this goes south across the border to the United States. After meeting domestic refining needs in Western Canada, Ontario and Quebec, roughly 95% of Canadian crude oil exports are to the US, due to proximity and Canada’s limited access to alternative trade partners, and an integrated oil infrastructure built over decades. This is a net figure – Canada actually exported 4.5 million bbl/d of oil to the US last year, mostly in the west from Alberta, with US oil flowing north to feed Canadian refineries in the east of the country.

Most of the exports (85%) are via pipeline. After some years of environmental opposition, many of the major transborder pipelines such as Keystone are now completed, and transport infrastructure also includes the Aurora, Enbridge Mainline, Express, Milk River, and Trans Mountain pipelines.

Carbon content

One of the major criticisms of oil sands production is its environmental footprint. The surface mines are unsightly, though companies perform remediation work once the area is mined out. But of increasing concern is the carbon footprint of oil sands crude, due to the heat that must go into melting the bitumen and the carbon cost of the hydrogen required to break the large molecules up into smaller, more desirable ones during upgrading. Oil sands extraction and processing is about 50% more carbon intensive than that for more conventional grades of oil, almost comparable to coal, and represents around 10% of Canada’s total carbon dioxide emissions, according to figures submitted to the UN.

The oil sands industry has pledged to make its onsite operations carbon neutral by 2050. Some modifications to existing operations can reduce carbon intensity by around 25%, including using solvent rather than steam for SAGD operations, and processing to dry tailings rather than using tailings ponds which may emit methane. Partial upgrading of bitumen and dilbit can also reduce emissions through more efficient conversion of bitumen and use of diluent. A number of facilities are also looking at carbon capture and sequestration or use. The government of Alberta is also targeting a C$30/tonne carbon price to be applied to oil sands facilities in order to drive towards reduced emissions and carbon competitiveness.

Sulphur from oil sands

Canada was the world’s sixth largest producer of sulphur in 2025, at 4.7 million t/a. More importantly, it was the third largest exporter, behind only the UAE and Saudi Arabia, with a total of 4.57 million t/a of sulphur exported. In spite of falling volumes being recovered from declining sour gas fields, increased recovery from oil sands production have so far by and large balanced this. Oil sands sulphur production within Canada totalled 3.0 million t/a in 2025, representing 63% of Canadian sulphur output.

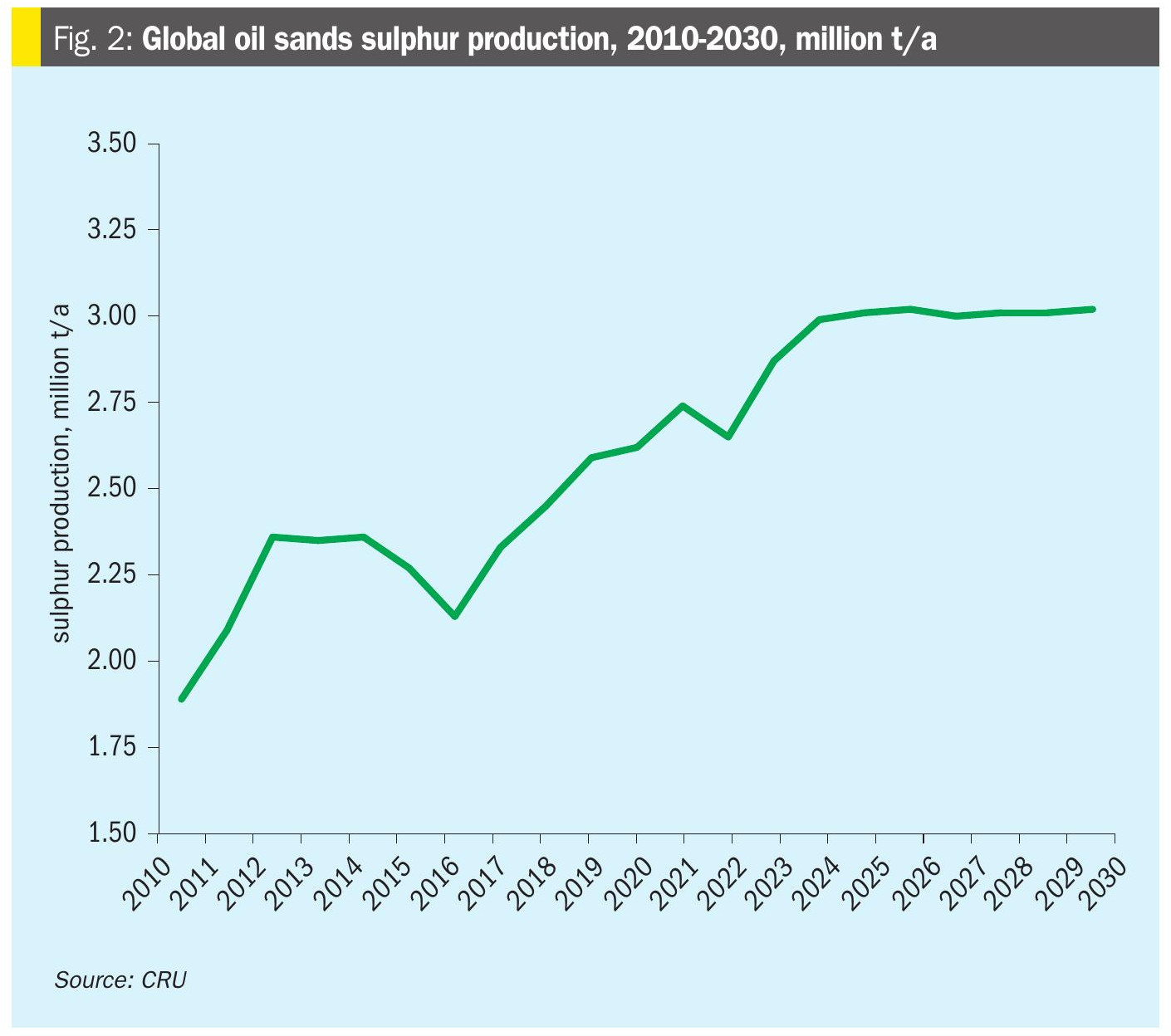

Canada continues to represent the lion’s share of all sulphur produced from oil sands, almost 98%, so the future of Canadian oil sands production is closely tied to how much sulphur is produced. Figure 2 shows world oil sands sulphur production over a 20 year period. Having grown slowly but steadily with Canadian oil sands output, there is at present no prospect of any major increase in this in the short term, although a period of sustained higher oil prices may encourage new investment back into Canada, and Venezuela remains a wild card in the longer term, depending on future relations with the US. Overall, oil sands-based sulphur production is expected to stabilise at around 3.0 million t/a from 2025 to 2030.

There is one additional corollary of this – if 3.7 million barrels per day of oil sands bitumen is being extracted, at an average sulphur content of 5%, that represents in theory a total of 8.3 million t/a of encapsulated sulphur that is being extracted. However, only the bitumen that is processed or upgraded in Alberta shows up in the Canadian figures of 3.0 million t/a of sulphur produced. The remaining sulphur will be extracted where the syncrude is delivered and processed, mainly on the Gulf Coast of the US. A shift to more processing within Canada could therefore increase domestic sulphur production while US refineries might need to source sour crude elsewhere.

Sulphur storage

The other factor in Canadian oil sands production is stocks of sulphur. The logistics of moving sulphur from northern Alberta to the port of Vancouver has been difficult and relatively expensive, meaning that in the early days of oil sands operations much sulphur was poured to long term storage in blocks. Since there has been a sustained run of higher sulphur prices, there are signs that some of this is now being recovered and remelted. Canadian sulphur inventory declined throughout 2025, prompted by a high price environment, and this trend is expected to continue into 2026. There plans to increase re-melting capabilities in Canada with new capacity commissioning by the end of 2026. A net figure of around 1.5 million tonnes of Canadian sulphur is expected to be remelted and sold in the period 2025-2030.