Plant Manager+

In an ideal natural draft urea prilling tower, molten droplets fall, cool air rises, and prills solidify – but what happens when airflow at the tower base is disturbed? Small adjustments can have big consequences.

In an ideal natural draft urea prilling tower, molten droplets fall, cool air rises, and prills solidify – but what happens when airflow at the tower base is disturbed? Small adjustments can have big consequences.

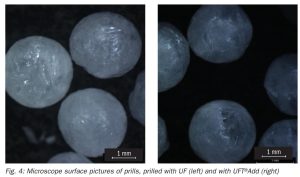

thyssenkrupp Uhde Fertilizer Technology) has developed a series of formaldehyde-free additives, UFT®Add, which keeps solid urea free-flowing during transport and storage, enabling compliant automotive grade urea production.

SABIC Agri-Nutrients Company says that it has received approval from the Saudi Ministry of Energy to allocate feedstock required for the construction of its seventh plant in Jubail Industrial City. The new facility will produce approximately 1.2 million t/a of ammonia and 2.6 million t/a of urea, increasing the company’s urea production capacity from 4.8 million t/a to 7.4 million t/a; a 54% increase. This is expected to strengthen its position as one of the world’s largest producers and exporters of nitrogen-based nutrients, in line with its 2040 growth strategy.

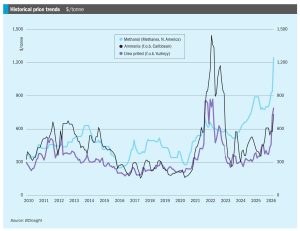

The start of May saw urea prices start to decline from the yearly highs seen in mid-April, as buyers from India, the US, and Europe stayed away from the markets. India is not expected to return with another tender before late May or early June at the earliest, after booking 2.5 million tonnes for shipment through mid-June, covering immediate requirements, and with domestic production having improved and stocks at a healthy level of over 7 million tonnes. In the US, earlier concerns over May shipments have eased, with net import figures not as low as initially feared, and even some re-export of cargoes to Latin America where higher prices can be earned. With the potential for China to return to export sales towards the end of May and start of June, there was at least a hope that the worst of the current price spike may be over.

• Short-term outlook: Ammonia benchmarks are expected to remain under upward pressure. The PAU turnaround removes a key supply source from an already tight SE Asian market.

Global ammonia benchmarks pushed to fresh highs in April, with a reported trade from Egypt to NW Europe at $905/t c.fr, marking the highest Atlantic level seen since the Middle East conflict began. The move was driven primarily by tightening North African supply, with Algerian offer levels climbing to $840-850/t f.o.b., and Egyptian availability constrained by EBIC being sold out through June, together with limited prompt tonnage from Abu Qir.

Bahrain’s Gulf Petrochemical Industries Company (GPIC) says that its ammonia, urea and methanol plants remain offline following an Iranian drone attack and subsequent fire at the site. No injuries were reported from the incident.

Saipem has been awarded a new urea license agreement by Mitsubishi Heavy Industries Ltd (MHI) for a new fertilizer plant in Turkmenistan. The contract entails the license for the use of Saipem’s proprietary Snamprogetti™ urea technology as well as related engineering services. The urea plant will have a capacity of 3,500 t/d. The new project follows the Garabogazkarbamid plant, commissioned in 2018 in Garabogaz, Turkmenistan, developed with the participation of Mitsubishi and Gap Insaat Yatirim ve Dis Ticaret AS, for which Saipem supplied the urea technology under a contract awarded in 2014 by MHI.

India’s urea industry was running at approximately half capacity after force majeure declarations disrupted LNG flows through the Strait of Hormuz amid escalating Middle East tensions, according to local press reports. Petronet LNG Ltd, which operates India’s largest liquefied natural gas receiving terminal, declared force majeure after upstream suppliers cited their inability to deliver contracted volumes amid disruptions to cargoes transiting the Strait. The move triggered supply curtailments by state-owned gas distributors GAIL (India) Ltd, Indian Oil Corporation Ltd (IOC) and Bharat Petroleum Corporation Ltd (BPCL), which supply gas under RasGas contracts to fertiliser units across the country.

Kazakhstan’s KazMunayGas (KMG) and China National Petroleum Corporation (CNPC) have commenced the development of a urea project planned for construction in the country’s Aktobe region, Interfax reported 31 March.