Artificial intelligence – the new normal?

Does artificial intelligence (AI) really herald a revolution in fertilizer production and, if so, what are the practical examples of this?

Does artificial intelligence (AI) really herald a revolution in fertilizer production and, if so, what are the practical examples of this?

thyssenkrupp Uhde says that it has successfully commissioned a hydrogen recovery unit (HRU) at the Fertil ammonia-urea plant in Ruwais, owned by Fertiglobe, a global exporter of urea and ammonia. The scope of work included engineering, procurement and site supervision during installation and start-up of the units.

As part of the Japanese government’s Green Transformation scheme, two hydrogen producers have been selected to receive subsidies for low-carbon production projects. Out of the overall $1 trillion GX scheme, $51 billion is earmarked for hydrogen and ammonia investments, with the bulk going towards a long-term programme that subsidises the increased production costs. The first two recipients are a Toyota Tshuho-led consortium (electrolytic hydrogen for steel), and Resonac (hydrogen from used plastics for ammonia). In the programme, production projects are required to have the support of a major hydrogen consumer – in Resonac’s case, this is Japanese chemicals giant Nippon Shokubai, who will offtake the ammonia produced from lower-carbon hydrogen.

The US Department of Energy has agreed a $1.5 billion loan for the Indiana-based Wabash Valley Resources LLC to finance a coal-powered ammonia plant in West Terre Haute. The project will restart and repurpose a coal gasification plant that has been idled since 2016. However, previous plans to include carbon capture and storage in the project, as agreed as recently as May by the US Environmental Protection Agency (EPA), appear to have been abandoned. The loan comes from the Trump administration’s Energy Dominance Financing Program financed via the so-called “big beautiful bill”. It aims to reduce US dependence on foreign sources of fertilizer and to provide domestic sources of consumption for America’s shrinking coal industry. The facility is aiming to produce 500,000 t/a of ammonia using coal from a mine in southern Indiana as well as petroleum coke as feedstock.

Ukrainian drones attacked the Azot chemical plant in Perm Krai on October 3rd, according to regional Governor Dmitry Makhonin. The strike reportedly disrupted production at the facility, one of Russia’s largest nitrogen fertilizer producers, located about 1,700 km from Ukrainian-controlled territory, which produces ammonia, urea, and ammonium nitrate.

Artificial intelligence is beginning to extend into all facets of modern life, and the chemical process industry is no exception. This article looks at where and how AI is being applied in the ammonia and downstream industries, what data and infrastructure are required, and the potential risks.

Ammonia producer CF Industries says that it has shipped its first cargo of low-carbon ammonia from its Donaldsonville, Louisiana facility. The 23,500 tonne shipment was purchased by commodities specialist Trafigura to be used in Antwerp, Belgium by engineering materials firm Envalior in the production of low-carbon caprolactam.

Blue ammonia – ammonia produced from fossil hydrogen with carbon capture and storage (CCS) – offers a cheaper alternative than green ammonia for low carbon supply in the short term, and is more suited to retrofits.

Venkat Pattabathula of SVP Chemical Plant Services, Taylor Archer of Clariant and Seshu Dharmavaram of Air Products, all AIChE Ammonia Safety Committee members, look back at some of the key lessons learned from the Symposium’s 70 year history.

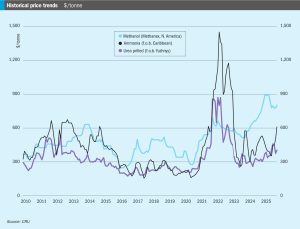

l The market looks very tight through the end of the year, though some expect supply to improve in Q4. Prices are unlikely to ease in the coming weeks. l Woodside’s Beaumont New Ammonia Project is now 97% complete, and the producer expects production from the first train in late 2025. There is no information from Gulf Coast Ammonia on when to expect commercial production. l There was an absence of fresh confirmed business into northwest Europe. Still, producers with ammonia capacity in the region are expected to be maximising output given the favourable economics at current spot natural-gas prices at the Dutch TTF.