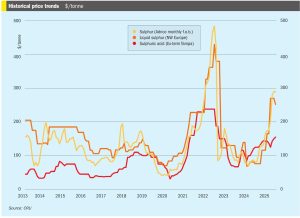

The Iran war and sulphur markets

The US and Israel attacks on Iran and the Iranian response have thrown commodity markets into chaos, with sulphur and sulphuric acid particularly affected.

The US and Israel attacks on Iran and the Iranian response have thrown commodity markets into chaos, with sulphur and sulphuric acid particularly affected.

• Market sentiment has shifted decisively from bearish to bullish as the conflict in the Middle East has triggers a significant price rally.

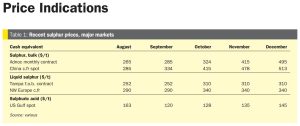

Conflict in the Middle East has halted all vessel traffic through the Strait of Hormuz, effectively paralysing a region that accounts for 48% of global seaborne sulphur trade. As a result, the sulphur spot market has ground to a halt, with prices notionally holding unchanged in the $490-515/t f.o.b. range simply due to a lack of activity. No spot offers were reported out of the Middle East.

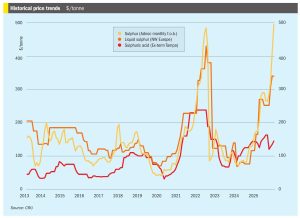

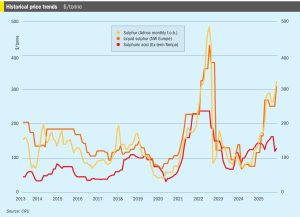

The global sulphur market’s bullish momentum from late 2025 has firmly carried over into the New Year, with prices pushing forward across most key regions despite a slow return to spot trading after the holiday break. With spot prices now past their 2022 highs and testing levels not seen since the 2008 peak, affordability has become the market’s central theme. The market remains divergent, with some buyers forced to accept the rally due to tight supply, while others, particularly in China, are showing clear signs of demand destruction.

• CRU’s latest global sulphur forecast is for a January price peak before a decline, with the key downside risk being a sharper correction if the supply deficit closes faster than expected. The global sulphur market’s upward momentum has been slowing, with attention shifting to geopolitical risks in Iran. Despite limited physical disruption being reported, the upside risk to prices could be substantial. Following the US bombing of an Iranian nuclear facility back in June, supply from Iran became bottlenecked, despite good production levels, as vessel owners became unwilling to call at ports like Bandar Abbas due to the increased risk.

Sulphur prices advanced further in October, more than expected, supported by the supply towards the end of summer becoming restricted, with a number of non-mainstream sources facing logistical constraints.

• Russia is set to impose a temporary ban on sulphur exports, covering liquid, granulated, and lump material, to ensure domestic supply. The measure will be in effect until 31 December 2025. CRU expects Russia to return to the export market in 2026 Q1. On the other hand, exports from Iranian ports are set to come back not only for Iranian production but also for Turkmenistan.

The global sulphur market registered price increases during August as a result of demand in Asia and North Africa, while supply has tightened due to limited supply from the FSU and Saudi Arabia, as well as logistical constraints in both Iranian ports and railway capacity to Black Sea ports.

• Global sulphur prices are expected to experience decreases over the next few weeks. Buyers in Asia report that they are covered for contracted supply throughout July, and domestic prices in China are likely to decrease further, putting downward pressure on sulphur prices.

The end of June saw declines in sulphur prices in many regions amid subdued global demand across regions. Most import markets are sufficiently covered through July at least, resulting in limited activity while supply increases. These conditions have exerted downward pressure on prices as bearish sentiment spread across regions.