Urea technology showcases

Casale, Saipem, Stamicarbon & Toyo Engineering Corporation showcase a selection of innovative technologies that have recently been brought to the market.

Casale, Saipem, Stamicarbon & Toyo Engineering Corporation showcase a selection of innovative technologies that have recently been brought to the market.

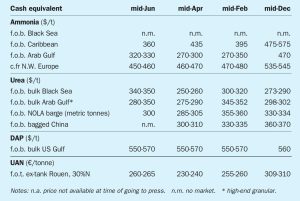

Ammonia markets were quiet in June, though both CF Industries and Grupa Azoty were reported to be looking for July tonnes and the enquiry will test how tight the market is going forward. Algeria has traded in the $400-405/t f.o.b. range, suggesting c.fr values in Europe might be slightly higher at $450-460/t c.fr. Supply from Algeria has been and continues to be somewhat restricted because of constraints caused by the hot weather. Gas supply however is easing in Egypt and further ammonia exports should emerge shortly.

Prices in the Eastern Hemisphere, whilst still flat-to-firm, do not appear as supported as they have been over the past month, whilst indexes. There are still no signs of softening in the Far East although demand remains underwhelming and supply improving. While production in Indonesia is said to be back up and running, traders do not expect any spot cargo to emerge in July other than possibly some small part cargoes. August could see spot offers.

The reliability of primary reformers is a key issue for syngas plants. Quest Integrity describes the damage mechanisms and material limitations that impact the reliability of reformer outlet systems and the improvements that may be implemented.

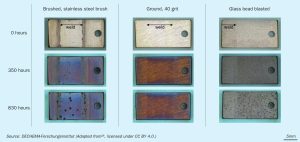

Industrial plants using synthesis gas at elevated temperatures risk metal dusting attack on the equipment, which are typically made of steels or Ni-based alloys. Parameters which impact the metal dusting risk are discussed and factors affecting the material selection and processing are described. One important focus is surface preparation, showing that grinding (40 grit) improves the metal dusting resistance compared to glass bead blasting and brushing. The surface treatment outweighs the impact of welds or the manufacturing route.

A review of the current slate of plans for green and blue ammonia production.

Although global ammonia supply is set to increase this year, there is a shortage of new merchant capacity after 2024 which may lead to rising prices in the medium term.

Large-scale ammonia cracking technology and catalysts will enable the full potential of ammonia to be realised as industries transition towards low carbon energy. In this feature we report on the current status of ammonia cracking processes and catalysts.

The ammonia market reverted to recent norms at the end of April, with prices more or less unchanged in the east, and several benchmarks west of Suez moving downward in line with May’s Tampa settlement. Following a trio of high-priced c.fr spot deals many wondered whether such business would be replicated in Asia, but the hype did not live up to the expectation, with the majority of tonnes continuing to move on a contract basis into the likes of South Korea and Taiwan, China. The $430/t c.fr concluded into China has been attributed to both supply uncertainty and an uptick in domestic demand, though several inland prices declined this week, rendering price direction difficult.

Low emissions hydrogen is expected to play an increasing role in the syngasbased chemicals industry, but cost and technical challenges remain.