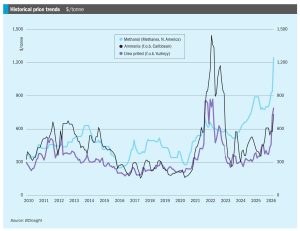

The start of May saw urea prices start to decline from the yearly highs seen in mid-April, as buyers from India, the US, and Europe stayed away from the markets. India is not expected to return with another tender before late May or early June at the earliest, after booking 2.5 million tonnes for shipment through mid-June, covering immediate requirements, and with domestic production having improved and stocks at a healthy level of over 7 million tonnes. In the US, earlier concerns over May shipments have eased, with net import figures not as low as initially feared, and even some re-export of cargoes to Latin America where higher prices can be earned. With the potential for China to return to export sales towards the end of May and start of June, there was at least a hope that the worst of the current price spike may be over.