Market Outlook

• Global sulphur prices are expected to stay relatively stable as purchases in Asia slow down due to the closing of the purchasing window for the Chinese spring fertilizer application season.

• Global sulphur prices are expected to stay relatively stable as purchases in Asia slow down due to the closing of the purchasing window for the Chinese spring fertilizer application season.

CRU’s World Copper Conference was run at the start of April 2025 in Santiago, Chile, with the industry facing a crossroads. The Americas account for nearly half of the world’s mined copper, with South America producing 38% and North America contributing 10%. However, North American copper mines face cash costs 51% above the global average and 79% higher than those of their South American neighbours, positioning the region as one of the most expensive copper-producing areas globally. These high costs create a significant challenge, especially as securing a reliable copper supply has emerged as a geopolitical priority.

• Continuing oversupply means that ammonia prices should continue to come under pressure moving into 2H April, though it remains to be seen just how much further values in Asia can decline before producers begin to shutter output.

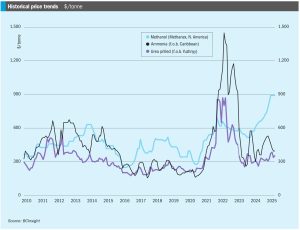

In mid-April, Ammonia prices both east and west of Suez remained firmly oriented to the downside, with supply still heavily outweighing demand and suppliers scrambling to place excess tonnage. Bearish market sentiment was exemplified by a Trammo sale to OCP at $415/t c.fr Morocco, $20/t short of Tampa’s c.fr settlement for April and around $44/t down on February.

Urea markets are well supplied at present in spite of Chinese export restrictions, but face volatility due to a number of trade barriers and other non-market pressures.

Wi th future demand for both low carbon methanol and ammonia depending to a considerable extent on their take-up as low carbon shipping fuels, recent developments in the EU and IMO may help accelerate that process, as detailed in CRU’s most recent Low Carbon Hydrogen and Ammonia Outlook.

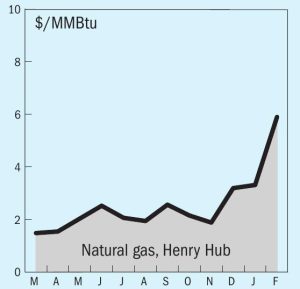

Global gas demand has returned to growth after the supply shock of 2022-23, but geopolitical tensions and short supply in LNG markets.

Mark Brouwer of UreaKnowHow.com reviews the main production options for incorporating sulphur into urea

We compare and contrast the 2024 financial performance of selected major fertilizer producers following the publication of fourth quarter results.

While green hydrogen and green ammonia promise to be important clean energy carriers in future, there are significant challenges to be overcome not only in production storage and transport, but also financially realising the project. Innovate technology from thyssenkrupp Uhde, embodied in standardised, pre-integrated, modularised plant can deliver low cost of ownership and de-risks execution.