Sulphur + Sulphuric Acid 2025

CRU’s annual Sulphur+Sulphuric Acid Expoconference was held from November 3rd to 5th, at The Woodlands, Texas.

CRU’s annual Sulphur+Sulphuric Acid Expoconference was held from November 3rd to 5th, at The Woodlands, Texas.

The deficit in the sulphur market has led to a new focus on melting down and selling stockpiles of sulphur around the world. From Kazakhstan to Canada, stocks of sulphur have been shrinking.

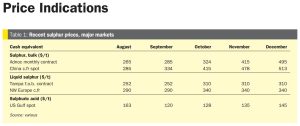

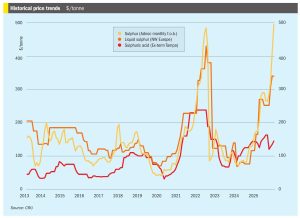

The global sulphur market’s bullish momentum from late 2025 has firmly carried over into the New Year, with prices pushing forward across most key regions despite a slow return to spot trading after the holiday break. With spot prices now past their 2022 highs and testing levels not seen since the 2008 peak, affordability has become the market’s central theme. The market remains divergent, with some buyers forced to accept the rally due to tight supply, while others, particularly in China, are showing clear signs of demand destruction.

Sulphur prices have risen rapidly in recent months as the market moves into a period of deficit which is likely to last until 2028.

The Chinese ammonium sulphate industry continues to see rapid growth, with exports rising to record levels, against increasing demand coming from Brazil and India.

• CRU’s latest global sulphur forecast is for a January price peak before a decline, with the key downside risk being a sharper correction if the supply deficit closes faster than expected. The global sulphur market’s upward momentum has been slowing, with attention shifting to geopolitical risks in Iran. Despite limited physical disruption being reported, the upside risk to prices could be substantial. Following the US bombing of an Iranian nuclear facility back in June, supply from Iran became bottlenecked, despite good production levels, as vessel owners became unwilling to call at ports like Bandar Abbas due to the increased risk.

The switch towards battery technologies like lithium iron phosphate (LFP) is leading to major growth in demand for sulphur and sulphuric acid.

The start of the new year has shown that 2026 is already proving to be a very eventful one, beginning with the US abduction of Venezuela’s president Nicolas Maduro, which has prompted questions over production at the country’s ailing nitrogen assets, as well as the potential for a future boost to gas supplies to Trinidad. Meanwhile the Iranian government faces its most sustained public challenge since the 1979 revolution, and possible US military intervention, threatening continued exports from the country. In Europe, the future of fertilizers’ inclusion in the Carbon Border Adjustment Mechanism (CBAM) has been thrown into doubt barely a week after the new regulations came into force, as France and Italy pushed for an exemption for crop nutrient imports.

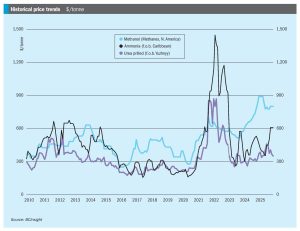

Ammonia values in the Middle East, Far East and Southeast Asia edged higher at the start of January, while other major benchmarks were largely unchanged amid a subdued market. Conditions at the start of the year mirror late2025, with prices supported by persistent supply tightness from the continued absence of Ma’aden’s MPC facility, which removes an estimated 300– 400,000 tonnes from the market. The unit is expected to return in midtolate January.

• Ammonia prices are expected to ease through January as new supply comes online. Woodside’s Beaumont facility produced its first ammonia at the end of December and is poised to start commercial production in early 2026, and there is also new supply from Gulf Coast Ammonia (GCA). In Saudi Arabia, the expectation is that both Ma’aden and Sabic will return to the market mid-to-late January.