Fertilizer International 531 Mar-Apr 2026

20 March 2026

Sulphur deficiency drives structural shift to ammonium sulphate

Ammonium sulphate has emerged as one of the fastest-growing segments of the global nitrogen market. Chinese exports reached record highs in 2025, driven by surging demand from Brazil and India. In this CRU Insight, Arina Syrdybayeva looks at the dynamics underpinning this high growth market.

Growers of cash crops such as soybean (shown) value the sulphur present in ammonium sulphate for yield improvement and soil conditioning.

Ammonium sulphate (AS) is a fertilizer containing 21% nitrogen (N) and 24% sulphur (S). Global production reached 35.78 million tonnes in 2025, with 36.72 million tonnes forecast for 2026. It remains the second most widely used nitrogen fertilizer globally, after urea, and the largest sulphur fertilizer by volume.

China dominates supply, accounting for 59% of worldwide production. Chinese output is primarily by-product-based, being derived from caprolactam (CPL) manufacturing for nylon fibres, methyl methacrylate (MMA), and methionine production. Lithium iron phosphate (LFP) battery production is also expected to add 2.0 million tonnes of AS capacity by 2029.

This production surge has reshaped global trade. Chinese material is forecast to account for 76% of the globally traded AS market by 2029, up from 70% in 2022, as European production has struggled with closures and weak operating rates, while high costs have made European AS uncompetitive in most markets except the United States.

Despite its origin as a by-product, AS has captured an increasing share of global nitrogen consumption, particularly in the Americas and Southeast Asia, where the crop mix and recognition of sulphur’s agronomic value have driven adoption. Brazil exemplifies this trend, with AS demand growing significantly faster than the broader nitrogen market as it substitutes for urea and ammonium nitrate.

This increase in popularity is underpinned by both agronomics and economics. Persistent sulphur deficiency in soils favours AS as a dual-nutrient solution. Its agronomic advantages, lower volatility in hot and wet conditions, longer storage stability, and suitability for sulphur-responsive crops have all supported uptake. While urea prices have remained elevated, AS has also offered a cost-effective alternative, on a per-unit nitrogen basis, despite being logistically less efficient due to its lower nutrient density (21% N for AS versus 46% N for urea). China’s exclusion of AS from export policy controls has also accelerated international adoption by allowing unrestricted trade.

Production – China secures market dominance

Global AS capacity growth this year will be driven primarily by by-product routes, with CPL and LFP production accounting for the majority of incremental additions. Approximately 70% of global AS capacity is by-product-based, although this proportion does vary by region: 83% in China, 73% in North America and 90% in Europe.

CPL-based supply is the largest growth engine, contributing approximately half of global capacity expansions. LFP-based capacity, critical to China’s electric vehicle battery manufacturing, surged in 2023 and added 0.5 million tonnes of AS capacity in 2025 alone. By 2030, China’s total AS capacity is forecast to reach 29 million tonnes, nearly double its 2020 level, with CPL-based capacity contributing 41% and LFP-based production 21%.

Underpinning both routes, sulphur and sulphuric acid serve as critical raw materials. In CPL manufacturing, approximately one tonne of sulphur produces three tonnes of sulphuric acid, which in turn yields 0.4 tonnes of sulphur content per tonne of caprolactam. Similarly, sulphuric acid serves as a key feedstock in tMAP (technical monoammonium phosphate) production for LFP batteries.

While high sulphuric acid prices indirectly impact AS production economics, the by-product nature of this fertilizer means its supply is driven by the output decisions of industries producing something else entirely. Elevated sulphuric acid costs in 2025, driven by tight sulphur supply and strong phosphate fertilizer demand, supported AS floor prices but did not fully offset the sheer volume of AS being produced as a by-product globally.

Coke oven gas-based ammonium sulphate (COG-based AS), meanwhile, faces structural headwinds. Although it accounts for roughly 20% of global production, COG-based AS output – also called steel-grade AS – is forecast to decline as China curbs its coke production to align with steel operating restrictions and environmental regulations. COG-based AS also suffers from impurities and darker colouration, limiting market acceptance. Chinese producers increasingly compact COG-grade and CPL-grade material into granular forms to meet export requirements, particularly for Brazil.

These capacity additions, combined with limited domestic consumption and AS’s exclusion from China’s restrictive fertilizer export policy, have triggered a sharp rise in traded volumes. China has secured market dominance by tailoring exports to consumer specifications and developing new markets in Africa and Myanmar, positioning itself to control 76% of globally traded AS by 2029.

Sulphur deficiency helps drive demand

AS consumption is virtually all fertilizer-based (95%), with its sulphur content becoming increasingly relevant as soil deficiencies intensify. Demand is more widely distributed than production, with the strongest markets in Asia, excluding China, and Latin America, particularly Brazil. AS accounts for approximately 50% of sulphur-containing fertilizer demand.

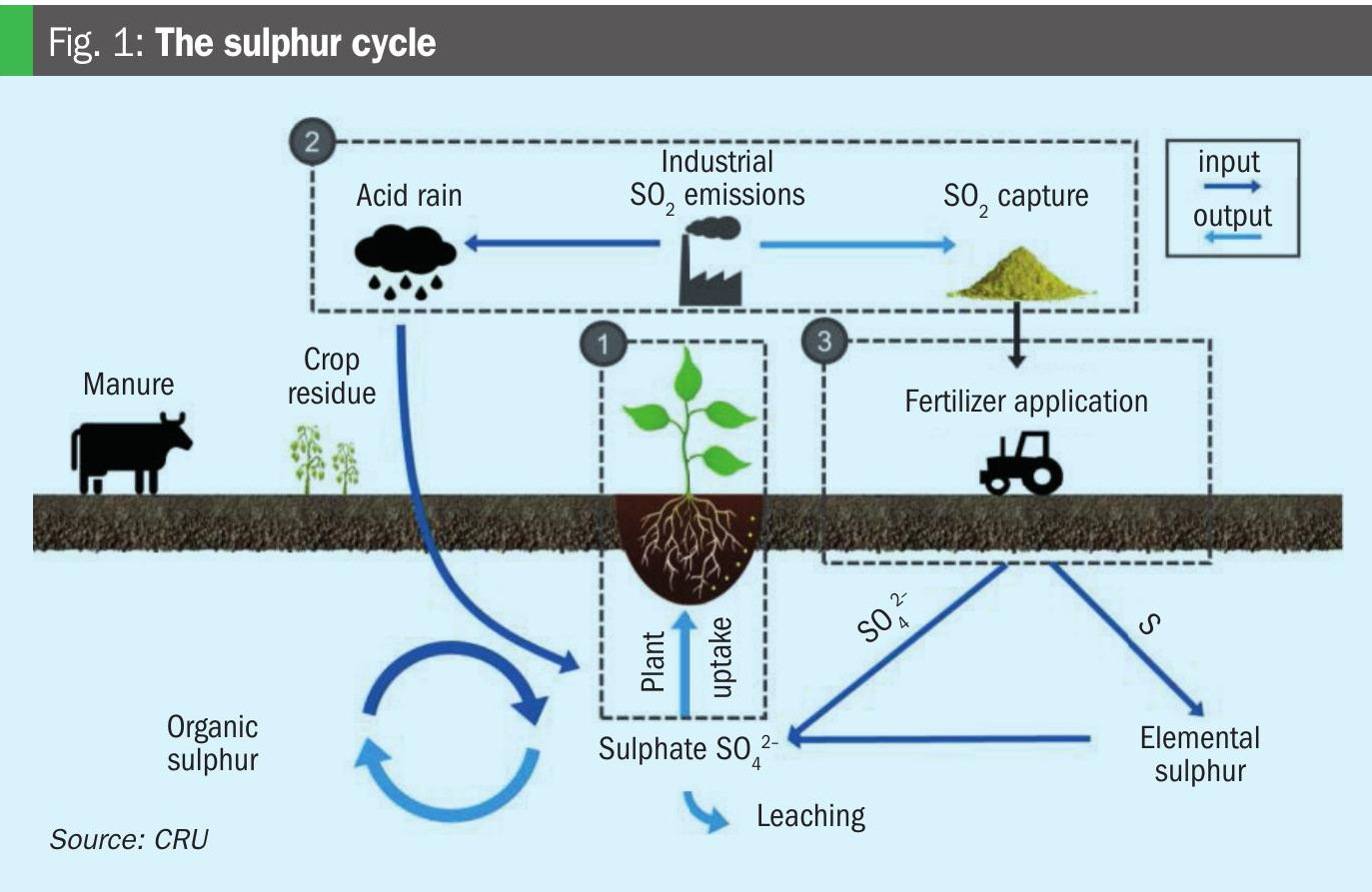

Persistent sulphur deficiency in soils remains a structural demand driver for AS, positioning it as a dual-nutrient solution addressing both nitrogen and sulphur requirements. Areas with pronounced sulphur deficits, South Asia and East Asia, represent long-term addressable markets, particularly as atmospheric sulphur deposition (Figure 1) continues to decline following stricter emissions controls on industrial processes and fuel sulphur content (Fertilizer International 520, p20).

The global sulphur deficit, estimated to exceed 12 million tonnes annually as crop demand outpaces fertilizer application, remains elevated, supporting incremental AS uptake where agronomic and price conditions allow. The shift towards high-analysis fertilizers such as urea, DAP (diammonium phosphate) and MOP (muriate of potash) over the past three decades has also exacerbated soil sulphur depletion, as these products contain little to no sulphur compared with traditional alternatives (Fertilizer International 520, p20).

Modern agricultural practices, including intensive cropping systems, higher-yielding varieties, and expansion onto marginal land, have further intensified sulphur removal rates. Certain crops such as soybeans require 50-60 kg S/ ha compared with 5-10 kg S/ha for low-intensity grazing. In regions where sulphur deficiency has become acute, AS offers an economically viable and agronomically effective solution.

Brazil’s 2025 demand surge

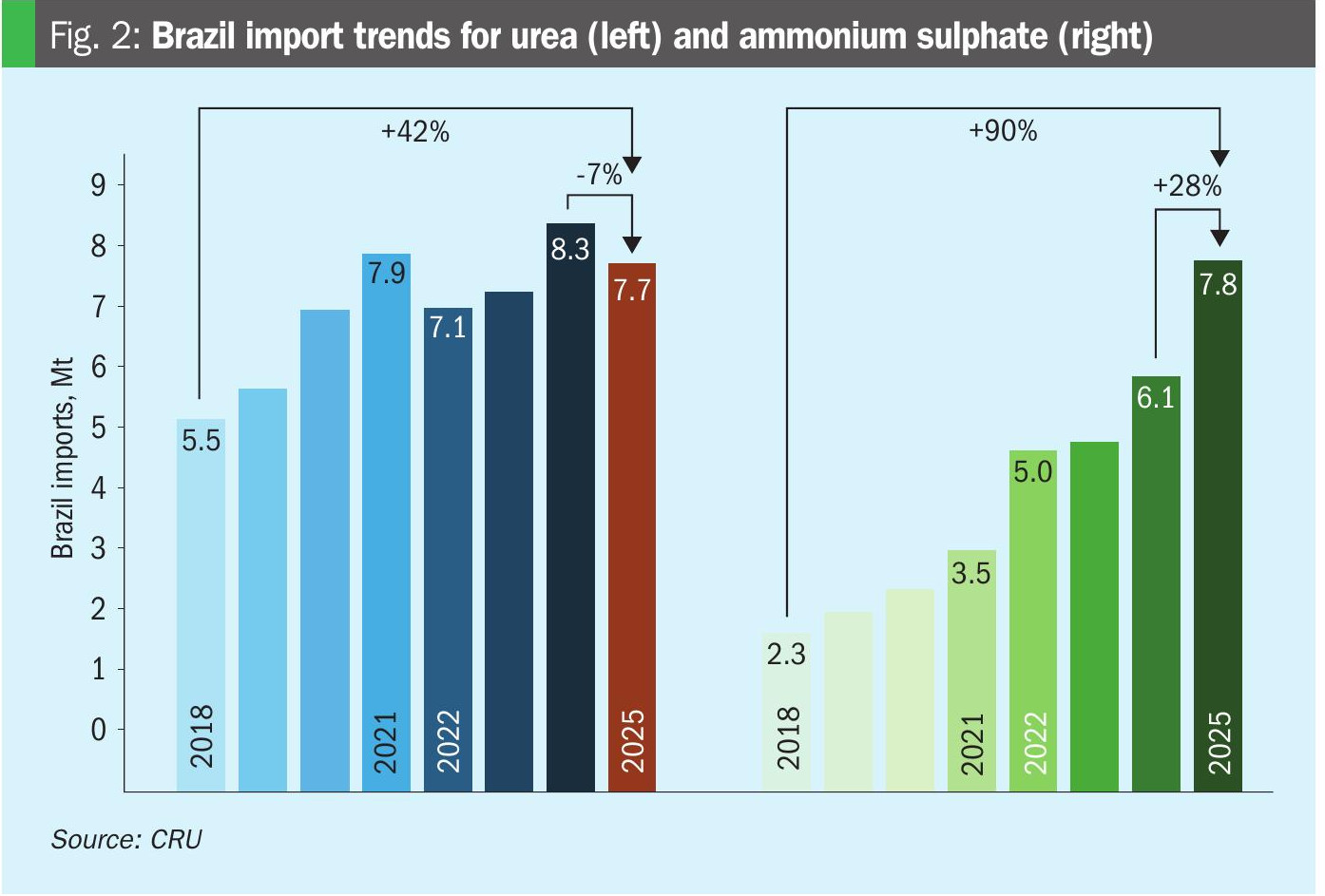

Brazil reinforced its position as the world’s largest AS importer in 2025, accounting for over one-third of global imports. Shipments surged to 7.8 million tones through 2025, driven by robust substitution of urea and ammonium nitrate, expansion of farmed areas, and an AS discount to urea that accelerates substitution. Brazilian AS consumption rose from 1.9 million tonnes in 2017 to 6.0 million tonnes in 2024 (Figure 2), with forecasts pointing towards 9.7 million tonnes by 2029.

Brazil’s preference for granular AS has reshaped Chinese export capacity. Brazilian imports are split 15:85 between standard and granular product, with Chinese compacted granules accounting for the vast majority. China has responded to this preference with a surge in compaction capacity, accounting for more than 99% of Brazil’s total AS imports in 2025, pushing European and US exports to seek alternative destinations.

The surge has been underpinned by favourable agricultural economics. Corn, cotton, soybean, and pasture rotations place high value on sulphur for yield improvement and soil conditioning. In the second and third quarters of 2025, AS also traded at a discount to urea for the first time on record, catalysing substitution. While urea imports declined 15% year-on-year in the first half of 2025, AS volumes grew, reconfiguring Brazil’s nitrogen import basket. So far this decade, ammonium sulphate’s share of its nitrogen demand has doubled, rising from 14% in 2020 to 28% in 2025.

Other markets

Southeast Asia’s AS imports reached 5.14 million tonnes in 2025, although year-on-year growth decelerated sharply to just 0.1%, down from 15.8% in 2024. This slowdown reflects affordability pressures. High AS prices due to freight costs, combined with declining rice prices in Thailand and Vietnam, undermined affordability and slowed buying activity. Demand in Indonesia and Malaysia, in contrast, has shown greater resilience supported by favourable palm oil economics. Combined, Myanmar, Indonesia, and Vietnam accounted for over 60% of regional imports in 2025.

Outside Brazil and Southeast Asia, global demand growth in 2025 was concentrated in India, Turkey, and Egypt, driven by policy changes and favourable pricing.

India’s imports rose from 140,000 tonnes in 2020 to 600,000 tonnes in 2025, with China accounting for 96% of supply. The updated Nutrient-Based Subsidy policy for 2025-26 incorporated domestic and imported AS, signalling long-term governmental support. Yet the market remains at an early stage with strong growth potential, as AS represents just 1.4% of India’s total nitrogen demand in 2025.

Turkey’s imports, meanwhile, rose 102% year-on-year in 2025, supported by low pricing and higher acceptance of AS for NPK production. Egypt also switched from a net AS exporter to a net importer last year as its domestic production faced gas supply disruptions.

Current market situation

The global AS market in 2025 has been defined by three forces:

- Surging Chinese exports

- Structural demand shifts in Brazil and India

- A narrowing premium with urea that is reshaping farmer economics.

China’s exports reached 21.4 million tonnes in 2025 dominated by Fujian and Hubei regions. The exemption of AS from fertilizer export inspections, due to its origins as a by-product and a domestic preference for industrial uses, has allowed volumes to move abroad freely. Chinese AS consumption has also weakened as urea has become more affordable, trading at a discount to AS on a per-unit nitrogen basis for the first time in months.

“Ammonium sulphate has captured an increasing share of global nitrogen consumption, particularly in the Americas and Southeast Asia, where the crop mix and recognition of sulphur’s agronomic value have driven adoption.”

Brazil’s dynamics shifted decisively in late 2025. AS demand weakened considerably as the urea premium over AS compressed, making urea more attractive on a per-unit nitrogen basis. High trucking rates, with transported volumes for AS being double those of urea due to its lower nutrient density, have seen activity in 2026 increasingly concentrated in southern Brazil closer to ports.

Production curtailments in the last quarter of 2025 and into 2026 have also shifted market dynamics. A progressive reduction in operating rates by Chinese CPL producers, from 80% in November to 70% by the end of 2025, has counteracted structural oversupply and prevented a slump in CPL-grade prices. This supply discipline has instead kept AS values elevated, even with slower demand from Brazil.

European AS demand is forecast to jump to 2.7 million tonnes in 2026 as domestic supply remains stagnant and import requirements rise. Southeast Asia imports are likely to decline slightly, as buying activity from major consumers remained subdued in 2025.

The key question for AS in 2026 is whether a host of factors – new urea capacity, China’s export quotas, AS production controls and CBAM in Europe – will undermine its affordability, a key advantage, and the rationale for substitution that has reshaped global nitrogen trade.

About the author

Arina Syrdybayeva is CRU’s Associate Analyst, Fertilizer Value Chain.

Email: arina.syrdybayeva@crugroup.com

Tel: +44 7799 639460