Sulphur 410 Jan-Feb 2024

31 January 2024

Market Outlook

Market Outlook

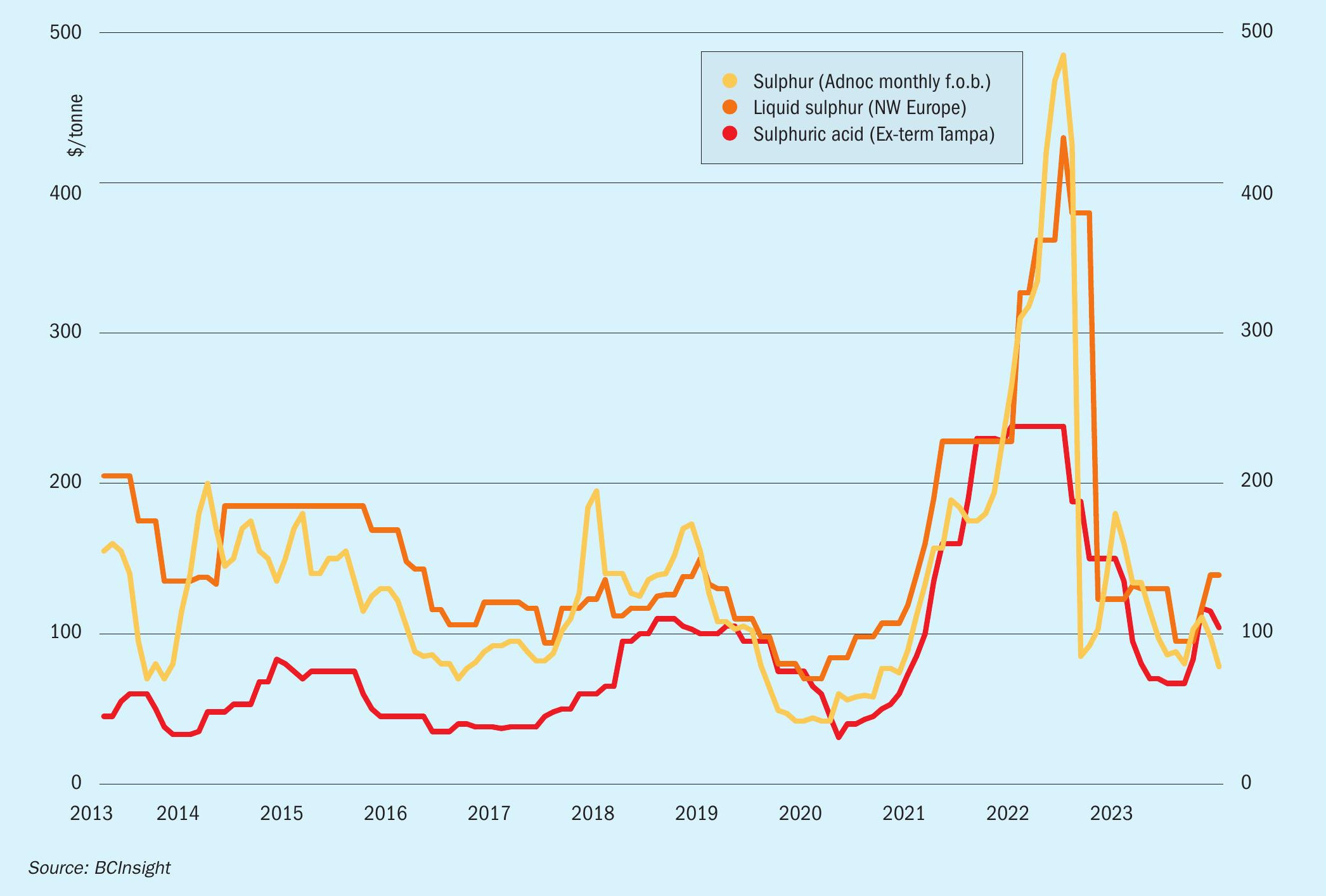

Historical price trends $/tonne

SULPHUR

- Sulphur prices are expected to increase during H1 2024, reversing the trend of recent declines, though good availability will limit the upside to price gains in the short term. However, should fertilizer production prove weaker than expected, prices may remain below expected levels.

- Chinese import demand should increase later in the forecast period if export restrictions are eased, and delivered sulphur prices to China are expected to increase over the coming six months to a high of $136/t CFR by June.

- Morocco’s OCP is also expected to increase its phosphate fertilizer production further over the coming months, as the buyer has ample spare capacity and the potential for good revenues and margins.

- Sulphur demand in Indonesia for nickel is set to increase further over the coming months, limiting the possible downside to global spot prices despite a weaker nickel market.

- Overall, the recent growth in sulphur production, in addition to stock drawdown and high China inventories, is expected to limit upwards potential for prices in the short term, and keep sulphur prices low relative to phosphates. Still, affordability continues to support raw materials purchasing and leaves room for price increases, especially if downstream production picks up as expected.

SULPHURIC ACID

- Morocco remains in the market for sulphuric acid tonnages for early 2024 arrival. The sulphuric acid line up at Jorf Lasfar was estimated at a total of 330,000 tonnes scheduled for arrival during 4Q23.

- Chilean sulphuric acid demand is expected to remain firm next year, with more end users keeping some of the volumes to be supplied by the spot market in anticipation of lower f.o.b. prices in Asia. The rise in northwest European prices and the ongoing logistics issues in vessels crossing the Panama Canal will likely affect vessel arrivals into Chile and result in more acid remaining in nearby destination markets.

- European suppliers are sold out for October-November loading. Some additional European supply could become available for December loading considering the current high export prices, but it remains to be seen if European producers can manage to free up some tonnes for loading towards the end of the year.

- European acid pricing is expected to remain firm next year as heavy maintenance at key smelters – such as Aurubis’ Hamburg smelter – is scheduled in the second quarter of 2024, which will tighten acid availability from Europe.

- Chinese acid pricing is expected to soften as 2024 progresses on the back of new smelter acid capacity coming online, as well as output ramp-ups from already completed projects. However, a risk to the forecast could be a strong domestic market, which may limit acid availability for the export market.