Market Insight

Price trends and market outlook, 18th December 2025.

Price trends and market outlook, 18th December 2025.

Price trends and market outlook, 23rd October 2025

Smelter outages and tight concentrate markets ease an oversupplied market.

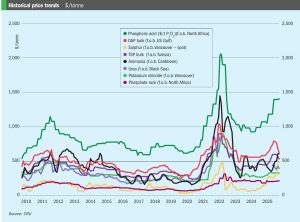

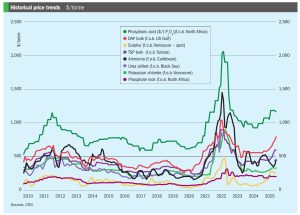

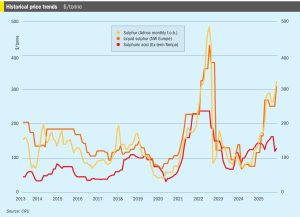

Prices in sulphur markets have been climbing rapidly for several weeks now due to short supply, reaching their highest levels for early two and a half years, since July 2022. A major cause has been widening Ukrainian drone and missile strikes against Russian oil and gas facilities. In particular, drone strikes in September on the Astrakhan and Orenburg natural gas plants led to Russian sulphur exports being cut drastically, first from around 400,000 tonnes per month to only 100,000 tonnes in October, and then to zero from the 1st of November, as Russia implemented a ban on exports of sulphur used in fertilizer production which was projected to last at least until December 31st. “This decision will stabilise shipments of raw materials to the domestic market to maintain current mineral fertilizer production volumes and ensure the country’s food security,” the government’s press service reported. The restriction applies to the export of liquid, granulated, and lump sulphur. It remains to be seen whether exports of Kazakh material from Ust Luga will be affected, but some Kazakh sulphur is now being sold via Iran.

Sulphur prices advanced further in October, more than expected, supported by the supply towards the end of summer becoming restricted, with a number of non-mainstream sources facing logistical constraints.

• Russia is set to impose a temporary ban on sulphur exports, covering liquid, granulated, and lump material, to ensure domestic supply. The measure will be in effect until 31 December 2025. CRU expects Russia to return to the export market in 2026 Q1. On the other hand, exports from Iranian ports are set to come back not only for Iranian production but also for Turkmenistan.

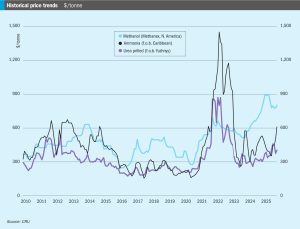

l The market looks very tight through the end of the year, though some expect supply to improve in Q4. Prices are unlikely to ease in the coming weeks. l Woodside’s Beaumont New Ammonia Project is now 97% complete, and the producer expects production from the first train in late 2025. There is no information from Gulf Coast Ammonia on when to expect commercial production. l There was an absence of fresh confirmed business into northwest Europe. Still, producers with ammonia capacity in the region are expected to be maximising output given the favourable economics at current spot natural-gas prices at the Dutch TTF.

By the end of October the ammonia market was facing an acute shortage of spot tonnage, reflected in a $60/t jump in the Tampa price for November. The benchmark Tampa price increased for the sixth straight month to its highest since February 2023 as the global ammonia supply crunch deepened. The surge at Tampa was said to be driven by good demand in the US for direct application combined with a lack of supply. Contributing factors included Nutrien shutting down its nitrogen production in Trinidad, potentially removing around 85,000 tonnes/month from the market. So far, there is no suggestion that other producers in Trinidad will follow suit, and they may even benefit from a boost natural-gas supply given the Nutrien outage, although it is unclear whether the spare gas will be directed to ammonia as opposed to other demand sources.

• The global sulphur market is forecast to enter a downward trend as supply from Saudi Arabia normalises following the summer months, while demand decreases alongside demand for phosphate fertilizers. The price is expected to fall towards the end of the year, with a low of around $220/t by May 2026.

The global sulphur market registered price increases during August as a result of demand in Asia and North Africa, while supply has tightened due to limited supply from the FSU and Saudi Arabia, as well as logistical constraints in both Iranian ports and railway capacity to Black Sea ports.