Pyrite-based acid production

While sulphuric acid production is dominated by sulphur burning or metallurgical acid routes, pyrite roasting remains a niche sector, particularly in China.

While sulphuric acid production is dominated by sulphur burning or metallurgical acid routes, pyrite roasting remains a niche sector, particularly in China.

Smelter outages and tight concentrate markets ease an oversupplied market.

While north Africa’s sulphur demand is dominated by its phosphate industry, south of the Sahara it is copper, cobalt and uranium mining, leaching and smelting that hold sway over acid production and demand.

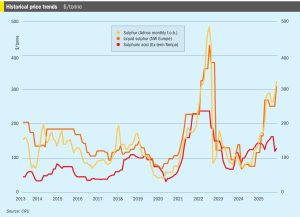

Sulphur prices advanced further in October, more than expected, supported by the supply towards the end of summer becoming restricted, with a number of non-mainstream sources facing logistical constraints.

• Russia is set to impose a temporary ban on sulphur exports, covering liquid, granulated, and lump material, to ensure domestic supply. The measure will be in effect until 31 December 2025. CRU expects Russia to return to the export market in 2026 Q1. On the other hand, exports from Iranian ports are set to come back not only for Iranian production but also for Turkmenistan.

Join us at the 2025 Sulphur + Sulphuric Acid Expoconference in The Woodlands, Texas, 3-5November, for a truly global gathering of the sulphur and sulphuric acid community, where leading market and technology experts and producers will gather to connect, share knowledge, exchange ideas and learn about market trends and the latest developments in operations, technology, processes and equipment.

Almost one third of sulphuric acid production, and a much greater share of globally traded acid, comes from smelting of base metal sulphides and the recovery of SO2 from flue gases. Smelter acid production continues to increase, particularly from copper, creating an imbalance in the sulphuric acid market.

North Africa remains a major centre of global phosphate production, with significant production in Algeria, Tunisia and Egypt as well as Morocco, and sulphur and sulphuric acid consumption continuing to increase.

The global sulphur market registered price increases during August as a result of demand in Asia and North Africa, while supply has tightened due to limited supply from the FSU and Saudi Arabia, as well as logistical constraints in both Iranian ports and railway capacity to Black Sea ports.

Sulphur output in North America continues to decline due to refinery closures and conversions at the same time that acid demand is increasing for metals processing projects.